Australians support shift away from fossil fuels with almost half expecting a spike in energy prices to reduce their purchasing power

A new global survey conducted by Ipsos for the World Economic Forum finds that, even though most consumers across the world expect their purchasing power to be impacted by rising energy prices, few blame climate change policies for it. The survey finds a consensus in all 30 countries surveyed around the importance of moving away from fossil fuels.

The survey was conducted among 22,534 adults under the age of 75 conducted between February 18 and March 4 on Ipsos’s Global Advisor online survey platform.

Detailed Findings

Impact of energy price hikes on consumers’ spending power

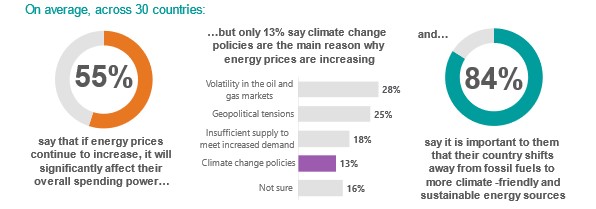

Survey respondents were asked to think of all the energy they use daily for transportation, heating or cooling their home, cooking, powering their appliances, etc., and how much they pay for it, and to assess how much energy price increases will affect their overall spending power. While on average, globally, 55% say price hikes will have a fair amount or a great deal of impact on their purchasing power, expectations vary widely across countries. More than two-thirds in South Africa, Japan, and Turkey say so vs. just over one-third in Switzerland and the Netherlands.

Australians appear more optimistic than many of the other countries surveyed, 46% anticipating price hikes will have a fair amount or a great deal of impact on their purchasing power.

Ipsos Public Affairs Director, Jennifer Brook, said: “Australians’ slightly more optimistic outlook on the impact of price rises may be due to our domestic supply of oil and gas. However, formal sanctions many countries are placing on Russia due to the invasion of Ukraine are being felt by consumers across the world. Most notably, Australians have been feeling the pressure at the bowser with petrol station fuel prices soaring in recent weeks.

“Our March edition of the Ipsos Issues Monitor saw petrol prices rise to the fifth top issue facing the country, with 24% identifying it as one of the top issues, – the first time petrol prices have featured as a top-five issue since we started monitoring this in 2010. And it’s not just petrol prices, energy bills are predicted to increase locally. Higher energy prices may well accelerate our transition to renewable energy sources away from coal and gas with lasting implications for our economy and environment.”

Globally, the survey finds few differences across demographic groups when it comes to the expectation that one’s overall spending power will be significantly impacted by continued energy price increases. Concern is slightly higher among those with a lower income and those in the 35-49 age group.

No unified views on the cause of energy price increases

In Australia, energy price increases are most likely to be attributed to volatility in the oil and gas markets (32%), followed by geopolitical tensions (19%), and climate change policies (17%).

Across the world, consumers show a diversity of views on the main reason for energy price hikes. On average globally, about one-quarter (28%) cite volatility in the oil and gas markets and another quarter (25%) cite geopolitical tensions; 18% cite insufficient supply to meet increased demand while only 13% cite climate change policies. With only one exception, no single reason is cited by a majority in any country.

- Like for Australia, market volatility is most widely seen as the cause of price hikes in Mexico (40%), South Korea (38%), Peru (36%), and Saudi Arabia (36%)

- Geopolitical tensions are most blamed in the Netherlands (the only country where any single reason is cited by a majority – 54%), Belgium (46%), and Italy (42%).

- Insufficient supply is most cited in South Africa (37%), Malaysia (28%), and Argentina (28%).

- Climate change policies are most commonly blamed in India (24%), Germany (20%), and Poland (19%); and among all demographic groups, by business decision-makers (19%). However, it is not the #1 reason in any country or among any demographic group.

Consensus on the importance of shifting away from fossil fuels

Four-in-five (80%) Australians say it is important that Australia shifts away from fossil fuels to more climate-friendly and sustainable energy sources in the next five years.

Australian opinion is consistent with global opinion, on average, 84% say it’s important to shift away from fossil fuels. Vast majorities say so in every country: from 72% in Russia and 75% in the United States, to 93% in South Africa and Peru. Citizens of emerging countries are especially adamant about it.

Globally, the level of importance granted to shifting away from fossil fuels is very high across all demographic groups. The only difference of note is along gender lines as the percentage viewing the shift from fossil fuels as important is six points higher among women (87%) than among men (81%).

About the Study

These are the findings of a 30-country Ipsos survey conducted February 18 – March 4, 2022, among 22,534 adults aged 18-74 in the United States, Canada, Ireland (Republic), Malaysia, South Africa, and Turkey, and 16-74 in 24 other countries, via Ipsos’s Global Advisor online survey platform.

Each country’s sample consists of ca. 2000 individuals in Japan and the United States, ca. 1000 individuals in Australia, Brazil, Canada, China (mainland), France, Germany, Great Britain, Italy, and Spain, and ca. 500 individuals in Argentina, Belgium, Chile, Colombia, Hungary, India, Ireland, Malaysia, Mexico, the Netherlands, Peru, Poland, Russia, Saudi Arabia, South Africa, South Korea, Sweden, Switzerland, and Turkey.

The samples in Argentina, Australia, Belgium, Canada, France, Germany, Great Britain, Hungary, Ireland, Italy, Japan, the Netherlands, Poland, South Korea, Spain, Sweden, Switzerland, and the United States can be taken as representative of these countries’ general adult population under the age of 75.

The samples in Brazil, Chile, China (mainland), Colombia, India, Malaysia, Mexico, Peru, Russia, Saudi Arabia, South Africa, and Turkey are more urban, more educated, and/or more affluent than the general population. The survey results for these markets should be viewed as reflecting the views of the more “connected” segment of their population. The data is weighted so that each country’s sample composition best reflects the demographic profile of the adult population according to the most recent census data.

“The Global Country Average” reflects the average result for all the countries and markets where the survey was conducted. It has not been adjusted to the population size of each country or market and is not intended to suggest a total result.

Where results do not sum to 100 or the ‘difference’ appears to be +/-1 more/less than the actual, this may be due to rounding, multiple responses, or the exclusion of “don't know” or not stated responses.

The precision of Ipsos online polls is calculated using a credibility interval with a poll of 1,000 accurate to +/- 3.5 percentage points and of 500 accurate to +/- 5.0 percentage points.