Trust in 2022

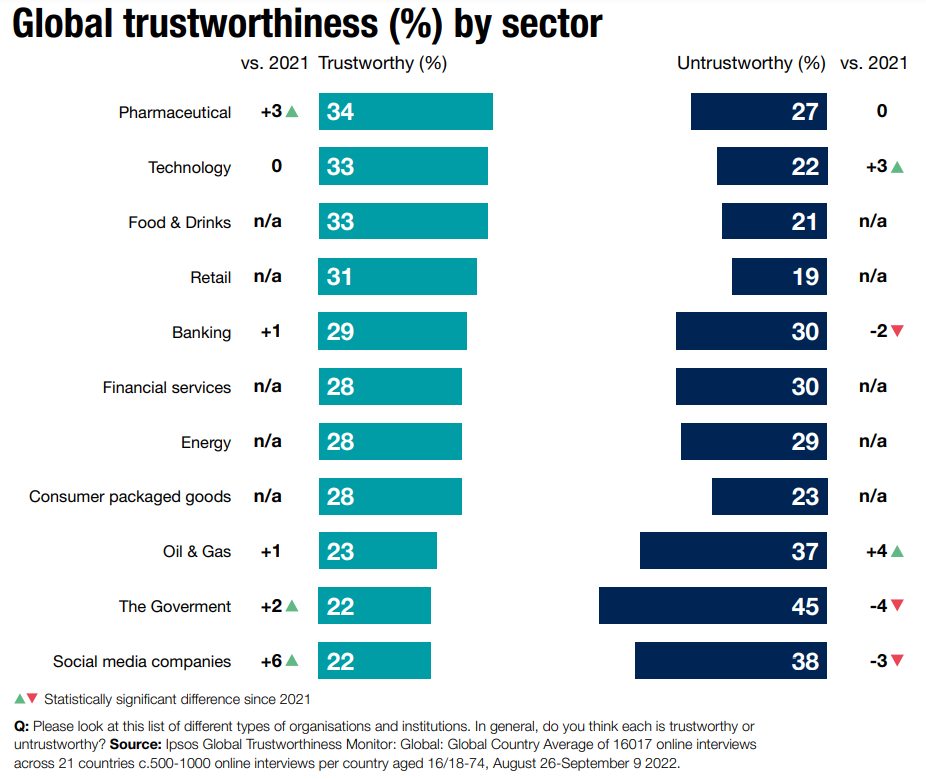

Which sectors do people think are most trustworthy?

It would be an understatement to say that 2022 was an interesting year. In our last ipsos Global Trustworthiness Monitor report, the COVID-19 pandemic was the top concern globally for the public of the most important social and political issues in our What Worries the World survey. But, at the time of writing this report, only one in ten (10%) choose it as an issue affecting their country. So as the pandemic has faded from the forefront of our minds, we have discovered many new things to alarm and worry us; a burgeoning global financial and cost of living crisis, a slumping economy, the war in Ukraine, political upheavals in leadership changes in several large and geo-politically influential countries, all of which have added to a sense of worldwide instability and uncertainty. Collins dictionary has chosen ‘permacrisis’ as its word of the year, defined as “an extended period of instability and insecurity”.

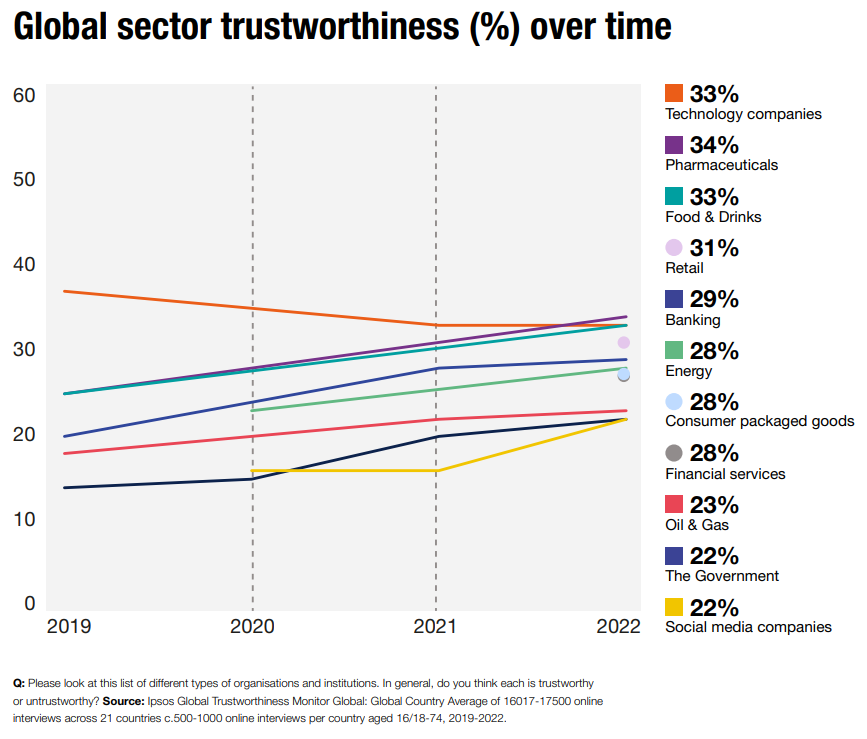

Global sector trustworthiness over time

Given the way trust in institutions and brands has traditionally been seen over the years, we might expect this to be the point where we reveal that global trust has taken another turn for the worse and, if the trend continues, then the foundations of society will start to crumble. The sort of decline and fall of faith in civic structures that Edward Gibbon attributed to the end of the Roman Empire. This has been the narrative that the Ipsos Global Trustworthiness Monitor has been warning against since it was first envisioned in 2018 and when we launched our first report in 2019; Trust: The Truth. To reiterate our review of the available evidence; there is no evidence that there has been a widespread decline in the level of trust that the public around the world has in the core institutions or industry sectors that shape everyday life. This has been what the evidence says, both over the last few years and looking further back, and we hope that our contribution to the wider debate has begun to change the way in which the trust debate is discussed.

Certainly, the data from this year is reason to be optimistic – trust across the world appears to be on a slow but steady rise for nearly all the sectors and institutions we measure. Given that levels of trust in most sectors is poor, as has always been the case, and some are seen as more untrustworthy than trustworthy, this may give some sectors hope that things might change in their favour over the long term. In the short term however, the headline finding is that the pharmaceutical sector, still riding high in public opinion for its work during the pandemic, has taken the top spot from the technology sector, but the more fascinating changes are at the other end of the spectrum.

As the pandemic has faded from the forefront of our minds, we have discovered many new things to alarm and worry us.

Government and social media, while still being far “in the red” when it comes to net trustworthiness globally, have made significant improvements over the last twelve months. In the case of the Government, this is the fourth year of incremental gain. This is likely down to the pandemic – to varying levels of success, it was national governments that tried to safeguard the public from the worst effects of the disease and parts of the public are grateful as a result. While the social media sector can lay claim to playing a role in keeping us entertained during the lockdown, the lack of change between 2020 and 2021 would seem to indicate that had little effect on sector trustworthiness. From wider, client-facing work ipsos has done, a contributory factor here may well be that it was during the pandemic that the sector took firm and decisive action on misinformation and fake news, albeit covid-19 specific, for the first time. Action that was widely seen in a positive light. Certainly, the social media sector’s performance across the drivers of trustworthiness has improved as well, perhaps indicating a softening of the public’s deeply held distrust of the sector.

The one exception to the positive story is the technology sector. As recently as 2019 the tech sector was seen, by a distance as the most trustworthy sector in our research, but since then the sector has been on a gradual decline and this year slipped to second place in the rankings, behind the pharmaceutical sector.

The bedrock trust that the world’s population has in Government and the major industry sectors of the world is still improving slowly

This decline in overall trustworthiness does not appear to have a specific cause – in fact, the sector still performs very strongly and has even improved on the key drivers of trust – but seems to represent more the “reining in” of tech back towards a sector norm as the gloss and mystique has begun to tarnish in recent years.

Overall, our key finding this time is that, despite a year of negative news, political uncertainty, and economic woe, the bedrock trust that the world’s population has in Government and the major industry sectors of the world is still improving slowly, in most cases. There has been no seismic change – some sectors are seen as trustworthy, many are not. But so far, the public’s judgment either way is yet to be affected by the momentous events of the year.

Methodology

These are the findings of an Ipsos online survey conducted between 26 August – 9 September 2022.

The survey was conducted in 21 markets around the world, via the Ipsos Online Panel system in Argentina, Australia, Belgium, Brazil, Canada, China, France, Germany, Great Britain, Hungary, India, Italy, Japan, Poland, Saudi Arabia, South Africa, South Korea, Spain, Sweden, Turkey, and the United States. The results comprise an international sample of 16,017 adults aged 16-74 in most countries and aged 18-74 in Canada, South Africa, Turkey and the United States. Approximately 1,000 individuals participated on a country by country basis via the Ipsos Online Panel, with the exception of Argentina, Hungary, India, Poland, Saudi Arabia, South Africa, South Korea, Sweden and Turkey, where each have a sample of approximately 500.

The samples in Argentina, Australia, Belgium, Canada, France, Germany, Great Britain, Hungary, Italy, Japan, Poland, South Korea, Spain, Sweden, and United States can be taken as representative of their general adult population under the age of 75. The samples in other countries (Brazil, China, India, Saudi Arabia, South Africa and Turkey) produce a national sample that is more urban and educated, and with higher incomes than their fellow citizens. The survey results for these countries should be viewed as reflecting the views of the more “connected” segment of their population.

Weighting was then employed to balance demographics and ensure that the sample’s composition reflects that of the adult population according to the most recent country Census data. The “Global Country Average” reflects the average results for all 21 countries where the survey was conducted.