Retail

As the World looks to find its feet again following a two-year global pandemic which saw several major retail companies forced into closure, a spiralling cost of living crisis conspires to take away more of the retail sector’s customer base as digital disruptors continue to undercut the high street. Increasingly, retail brands need to differentiate in order to stay competitive, and commitment to fulfilling a societal purpose and doing the right thing on ESG could be the way to do just that. Being seen as trustworthy to ‘do the right thing’ can reap its own rewards, as increasingly ethical consumers become more picky with their brand loyalties. The Ipsos Global Trustworthiness Monitor assesses how the retail sector stacks up against other sectors, what the challenges are to its reputation, and what ultimately makes the sector trustworthy.

Generally, the sector is seen as more trustworthy than not, behind only the food & drink, technology and pharmaceutical sectors. Out of all the sectors asked about, retail, along with food & drink, is the sector least likely to actively be seen as untrustworthy. The Global Trustworthiness Monitor tells us that being reliable, transparent and responsible are key drivers of trust, and as the sector continues to navigate challenging circumstances, it has been judged well on these. Retail sits only behind pharma and food & drink on behaving responsibly and leads all sectors in the study on being seen as reliable and transparent. Indeed, compared to other sectors, the fundamental underpinnings of trust are strongest in the retail sector.

However, like many sub-sectors which make up the Consumer sector, cost of living and inflation – which top the list of people’s worries both globally and in the UK according to Ipsos WWtW data – are set to pose some challenging questions for the retail sector in 2023. As the fallout of external shocks such as Brexit, Liz Truss’ ill-fated economic tinkering and the war in Ukraine continue to drive inflation and costs are passed onto consumers who are increasingly struggling, consumer spending is likely to decrease.

With the financial pain continuing into 2023, a third of Britons reported they were ‘just about getting by’, and a fifth said they were finding things ‘difficult’ last Spring. Moreover, 87% of Britons said 2022 was a ‘bad year’ for their country, and 86% of Britons said it was more likely than unlikely that prices to rise faster than income in 2023. The Ipsos’ Consumer Confidence Index at the end of 2022 further underlined this sense of gloom in the UK as its confidence index score dropped 10 percentage points to 41.8 between February and November - the largest out of all nations surveyed. Hungary saw the next biggest drop, down 9.9pp to 30.4, followed by Germany (down 9.6pp to 44.3) and Belgium (down 9.6pp to 38.0).

To make matters worse, a general sense that the economy is rigged to advantage the rich and powerful (71%) permeates in the UK, according Ipsos Broken-System Sentiment Index. As cost of living concerns continue to mount, having held the top spot since last March and almost doubling since the start of 2022, affordability, and moreover a sense of fairness, could be some of the most important battlegrounds moving forward. Pricing, the fourth most important driver of trust will be something retailers will be judged on over the coming year, particularly as many tighten their belts. The challenge for high street retailers may be particularly acute as they try to strike a balance between remaining affordable and fair, as online disruptors continue to undercut traditional brick and mortar establishments with lower prices. However, it’s not the only thing retailers will be judged on.

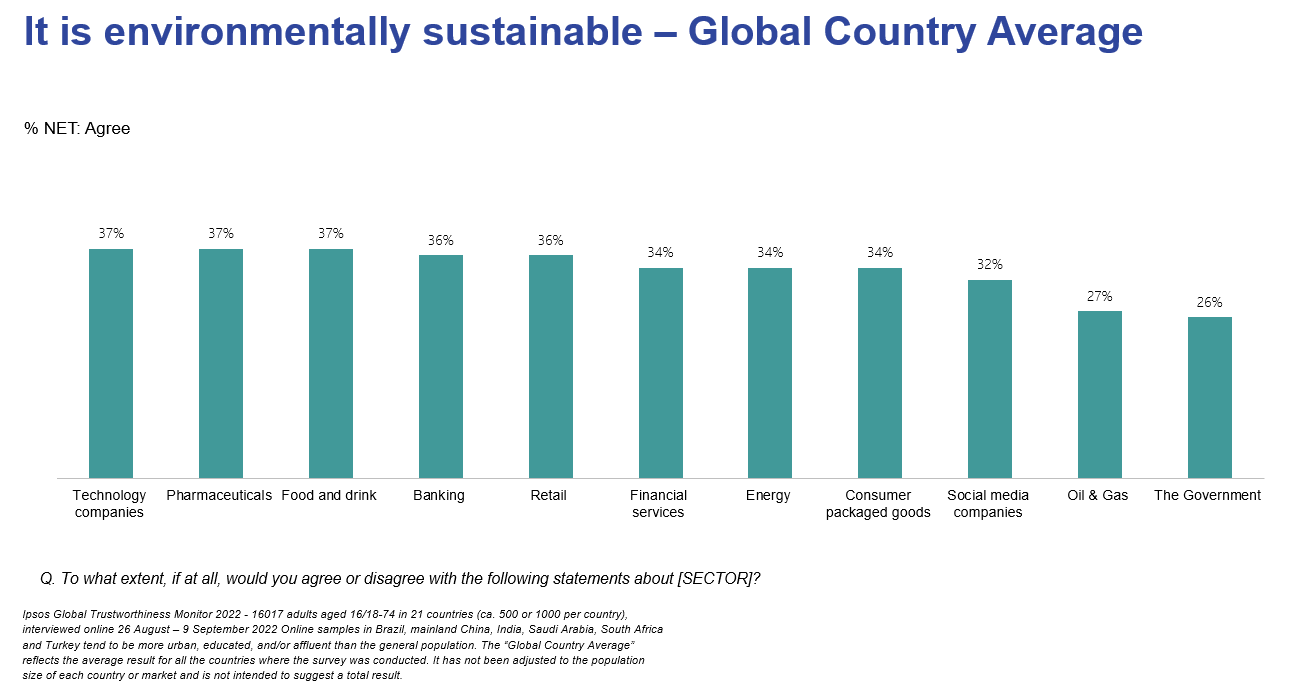

As the climate also continues to worry many, companies that share a social responsibility and are shown to be environmentally sustainable are increasingly preferred where retailers which can leverage this USP may well be able to curate a loyal customer base. Encouragingly, the sector as a whole is seen to be environmentally stable compared to other sectors, but individual brands ought to bear in mind the ESG behaviours of companies are becoming increasingly scrutinised.

That said, there is some scepticism as to whether people trust business leaders to care for the environment. Globally, 32% trust them compared to 34% who do not. In Western countries however, Great Britain for example, only 18% would trust business leaders compared to 47% who do not. Thus, any products or actions that retailers may consider when attempting to leverage the popularity of environmentally conscientiousness must be backed with tangible actions and evidence. Indeed, over half globally say businesses use the language of changes to the environment or to promote greater equality without committing to real change. Increasingly, businesses are expected to take a stance on these issues and show real commitments, where those who do not may face damaging reputational backlash.

According to half those polled in the Global Trustworthiness Monitor, the most successful brands in the future will be those that make the most positive contribution to society beyond just providing good services and products. Often, we find that is the companies which are striving (or ignoring) this that are most often in the news. And as a sector which is under great external economic pressures, while also featuring in the social fabrics by their presence on our high streets, those operating in retail are constantly in the limelight. Showing a social utility may not be a business’ first instinct, but it does mark them apart from others and has the power to convert consumers into a loyal customer base. In a time where people are struggling and want companies to take a stand on societal issues, developing such USPs – and reputations – around such things may prove the to be a key driver of growth in real terms and reputation.