Feeling the pressure: Context

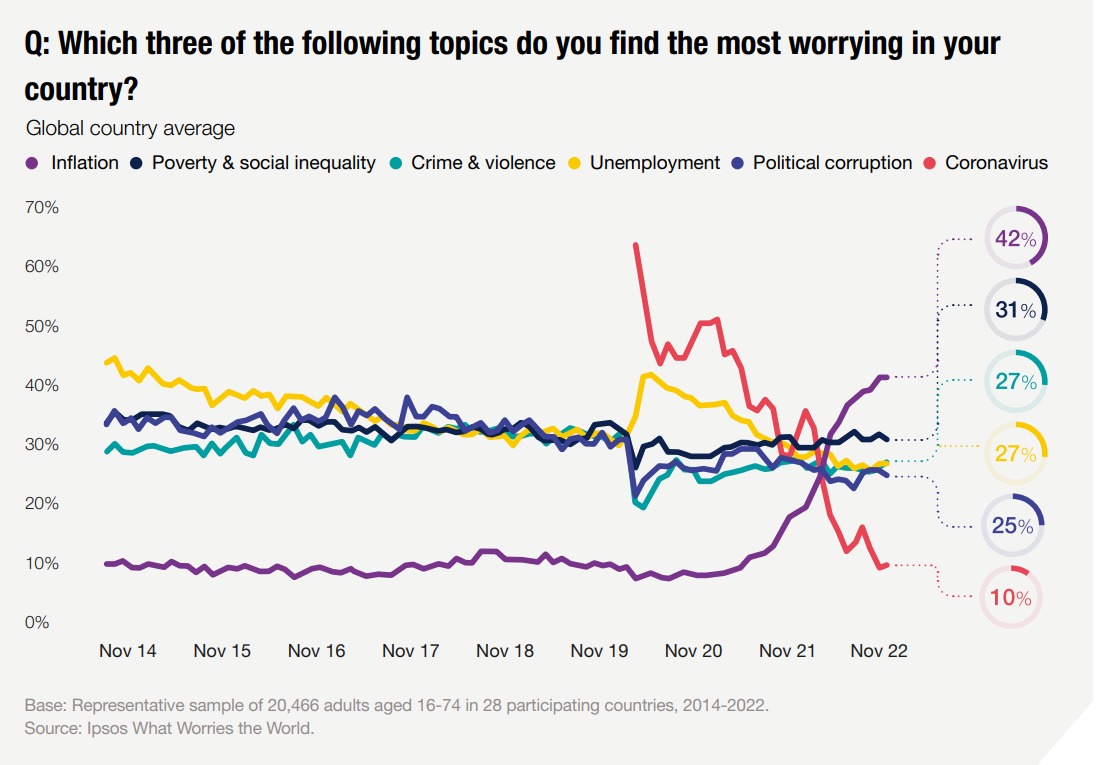

As we began 2022, the pandemic was the number one concern in our What Worries the World survey, with inflation down in seventh spot. Although concern had been ticking up steadily, the proportion saying it was one of the big issues stood at just one in five. Today, inflation has now been the top worry for the last eight months, with 42% saying it is one of the most worrying issues in their country. Meanwhile, coronavirus ranks 12th in our list of 18 worries, above moral decline, with only one in ten choosing it as a concern.

Today in eight countries more than one in two choose rising prices as worry and 13 countries have it as their number one concern (Argentina, Australia, Belgium, Canada, France, Germany, Great Britain, Netherlands, Poland, Saudi Arabia, South Korea, the US and Turkey).

This worry about the cost of goods is reflected in how people how are feeling. One in four (26%) say they are finding it difficult, with people in LATAM countries struggling most (Argentina 56%, Peru 50%, Colombia 46%). In Europe, fewer define themselves as struggling, but many feel they are “just getting by”. While one in three globally feel this way, this rises to over four in ten in Belgium (43%), Spain (44%), and Italy (42%), and more than one in two in Poland (51%). Europe is also more negative about the future, being the region most likely to think their standard of living will decline over the next year (see left). One in two in Turkey (52%), Hungary (50%), and Poland (48%) think their standard of living will fall in the next year, the highest out of 36 countries. To understand how people in Turkey are coping with hyperinflation, our chapter on the country goes into more detail.

There is a significant difference when we turn to the UAE and India and find more than one in two expect their standard of living to go up. In India our research has found consumers are less focused on cutting back on consumption and more focused on growing their income to cover rising prices through second jobs and side hustles.

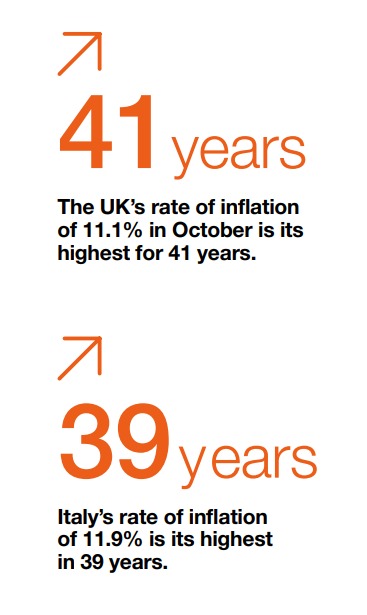

The differences in outlook between Europe and other regions could in part be down to the low level of inflation Europe has experienced in recent decades. For example, the UK’s rate of inflation of 11.1% in October is its highest for 41 years, while in Italy it is the highest in 39 years at 11.9%. In India, the current rate of around 7% is nothing new for consumers, who dealt with double-digit inflation in the last decade. Learn more about how Indians are dealing with inflation in our chapter on India later in this report.

Emergence of the polycrisis

At the beginning of this year, government policy-makers, business and individuals had, broadly speaking, one main problem to deal with: coronavirus. Now, while inflation is the number one concern globally, there are a number of additional crises facing us. Instability has reigned supreme in 2022, with the Russian invasion of Ukraine, the hottest ever temperatures in Europe and destructive flooding in Pakistan making the effects of climate change more visible.

At the beginning of this year, government policy-makers, business and individuals had, broadly speaking, one main problem to deal with: coronavirus. Now, while inflation is the number one concern globally, there are a number of additional crises facing us. Instability has reigned supreme in 2022, with the Russian invasion of Ukraine, the hottest ever temperatures in Europe and destructive flooding in Pakistan making the effects of climate change more visible.

In the US the overturning of Roe vs Wade highlights that the freedoms we take for granted cannot always be relied upon. What’s more all of this comes on the back of two years of precariousness, disruption and “unprecedented times”. To describe this phenomenon some have defined this as the polycrisis, interacting crises that result in harms greater than the sum that the crises would produce in isolation. Two articles in this report highlight this time of instability: the first looks at human psychology within the polycrisis we’re now faced with, and the second focusing on disruption.

The inflation crisis is itself perceived as the fault of many factors. Consumers accept that this is a worldwide problem, with three in four (74%) blaming the state of the global economy and seven in ten (70%) the Russian invasion of Ukraine for rising prices.

While global forces are playing a role, consumers feel that policies within their country are contributing. Seven in ten choose interest rates and the policies of my national government as contributing to inflation (both 69%). Blaming government is highest in Great Britain (84%), South Korea (82%), and Thailand (81%). In Britain this figure is up from 74% in July and is, according to Brits, the biggest contributor to inflation.

Brands are also facing higher costs, with many passing on these to consumers. Businesses making excessive profits is also seen a big contributor to the rising cost of living, with the same number of people blaming brands (62%) as blame the pandemic (61%). This is particularly high in Thailand (78%) and Brazil (75%). In this report, one of Ipsos’ pricing experts in Brazil, Luis Fernando Freixedas Abimerhy, explores how brands can navigate rising costs and sets out the options open to businesses. Our research has highlighted that empathy and transparency are key for brands while people are dealing with this multitude of crises. One of our community members in the US summed this up: “(I want) more compassion and showing care for their customers and employees, rather than pushing a product.”

Where next?

As we look to what lies ahead, few expect prices to stop increasing. Almost three in four (73%) expect to be paying more for their utilities in the next six months. Seven in ten expect their food shopping (72%) and other household shopping (70%) to rise.

Many are already changing the way they shop, whether that’s going to different stores, buying more private labels, or shopping around.

For those that are already doing this, if prices continue to rise, buying less may be only option.

Looking at the US, there are big differences in how people are coping. 31% say they are doing alright and 17% say they’re living comfortably. However, more than one in five (22%) are finding it difficult with half of these already finding it very difficult. Our ethnographic tracker America in Flux highlights how Americans are changing their shopping behaviour and, one participant (Terri) showing the anxiety and difficult decisions many are facing to put food on the table (see quotes overleaf).

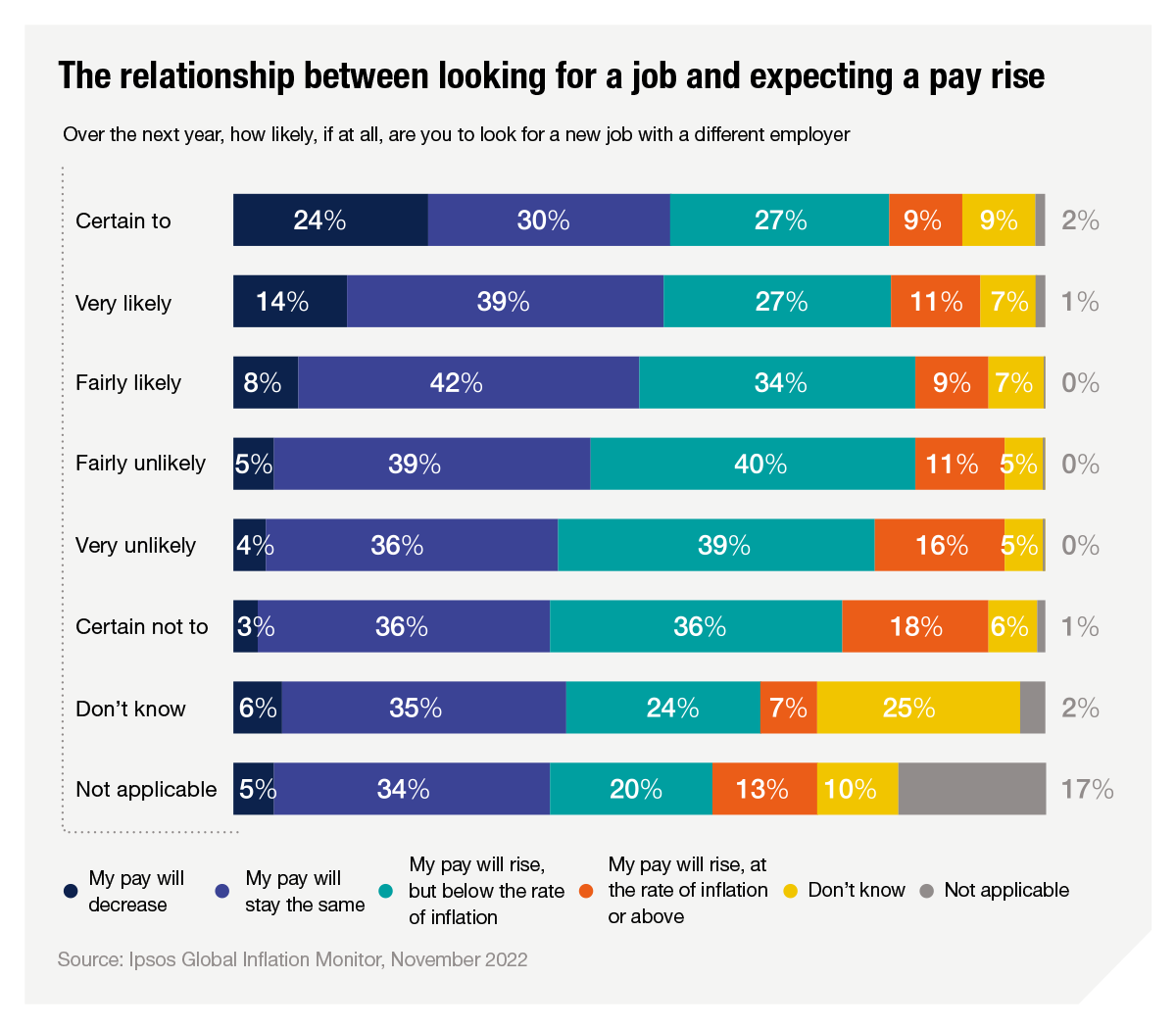

In 2023, one word which we will likely be discussing more is recession. Central bankers around the world are worried about wage-price spirals, lengthening this period of inflation. While 45% are expecting a pay rise in the next 12 months, very few expect (12%) feel it will be at or above the rate of inflation. 37% expecting their disposable income to decline in 2023. Fears of a wage-price spiral in Europe were allayed somewhat in November with Germany’s biggest union IG Metall, accepting a pay rise for its members well below the country’s current rate of inflation.

There is a belief that unemployment will be a bigger issue next year than it was in 2022. Six in ten (61%) say that unemployment in their country is going to rise, this is up from 56% back in July.

Over four in ten (43%) workers globally say they are certain/likely to look for a job with a new employer in the next 12 months. Likelihood to look for new work was lowest in Europe with Romania (42%) the highest figure in the region. Moving back to a global picture, more than one in two of those certain/very likely/fairly likely they will look for a new job are expecting a reduction in their pay or their salary to stay the same. Of those fairly or very unlikely to look for a new employer, four in ten say in 2023 they will get a pay rise but below the rate of rising prices.

What is clear is in 2023 the problems we’ve faced recently are not going away, including the increasing difficulty of retaining employees, but the dynamic of the next 12 months is going to be different.

Table of content

- Introduction

- Feeling the pressure: Context

- Understanding human psychology during the polycrisis

- Has disruption become the new normal?

- The Indian consumer's response to inflation

- Turkey: Re-designing adaptation in the shadow of hyperinflation

- Brazil: Downsizing VS price rises- making the right choice

- Malaysia: Between money well spent and life well lived

- Understanding Argentina

- France: The end of recklessness

| Previous | Next |

The author(s)

-

Jamie StinsonIpsos Knowledge Centre

Jamie StinsonIpsos Knowledge Centre

![[WEBINAR] KEYS: Dialling Up the S In Sustainability](/sites/default/files/styles/list_item_image/public/ct/event/2026-06/keys-webinar-sustainability.webp?itok=xPunvoGu)

![[Webinar] Real-World Evidence: Empowering the Patient](/sites/default/files/styles/list_item_image/public/ct/event/2026-05/healthcare-real-world-evidence-webinar.jpg?itok=kT0PwLPQ)