Turkey: Re-designing adaptation in the shadow of hyperinflation

Under the pressure of hyperinflation

Inflation is not a new term in Turkey. Looking at the history of inflation; the annual rate for the last 50 years is around 40%. However, in recent years, we were getting used to living without inflation. For the first time in Turkey’s economic history, inflation remain below 10% for most of the years between 2004 and 2017.

However, it has now returned and returned in a big way. Since 2018 inflation has been growing and reached a new record of 83.5% in September 2022. There are different reasons for this, both local and global, but most importantly, Turkey society must quickly adapt to our new reality to survive.

How daily life is changing

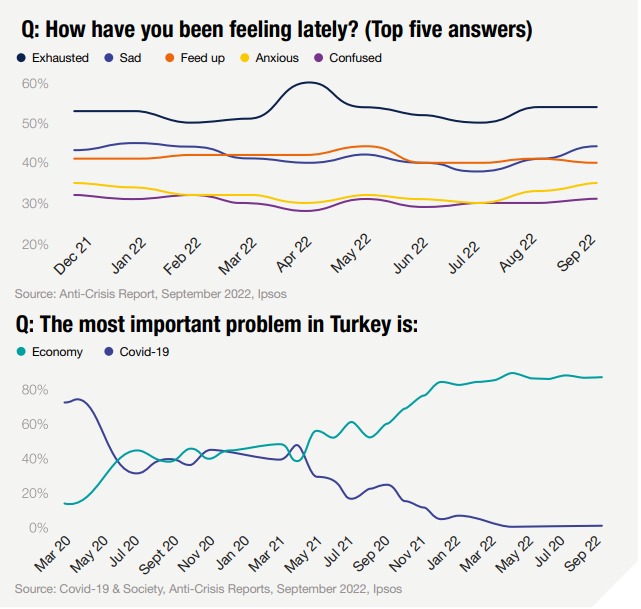

In the last year, the most dominant emotion in Turkey has been exhaustion (see previous page). This is reflected in our 2022 Global Happiness Report, where only 42% in Turkey said they were very/relatively happy, the lowest out of 30 countries. This figure is down 17percentage points on the previous year and is long way from 2011 when 89% in Turkey described themselves as very/relatively happy.

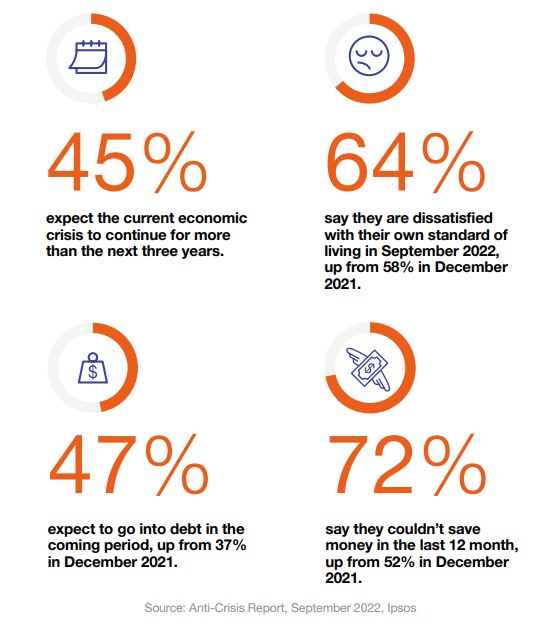

Despite all the negativity, life is a stage and the show must go on. Almost half (47%) think the current period of economic disruption will continue for the next three years. This expectation shows that changes in daily life do not involve just giving up as a solution; we are trying to shape our daily habits within these unstable conditions. This section looks at the changes we’re seeing.

|

|

Changes to shopping habits

- Price increases in items such as food and transport - which have a big impact on our daily lives - are higher than the overall inflation rate. The effect of this on daily life is therefore much deeper and negative.

- The rise in minimum wage to protect a significant part of those in work took place after the spike in inflation began, so there is a lag between price increases and wage adjustment.

- Because of all this, there is competition not only between the brands on the same shelf, but also across sectors.

- The fashion industry has been one of the most negatively affected industries, with the choice to minimize spending on clothing becoming a top action consumers are taking against rising prices.

- Second-hand shopping is rising as a means to manage household budgets. According to our Anti-Crisis Report, more than one in three (35%) computer purchases in July were of second-hand products.

- The attractiveness of second-hand products is not just limited to durables. Demand is becoming a trend in different sectors, from clothing to baby products.

- Discounters are getting stronger and are the fastest growing channel, with value growth up 80% on last year.

I used to order coffee from a chain on the way to the office but now it’s too expensive. Now I make my filter coffee at home, I put it in this chain brand thermos. It feels good to me as if my habit hasn’t changed.

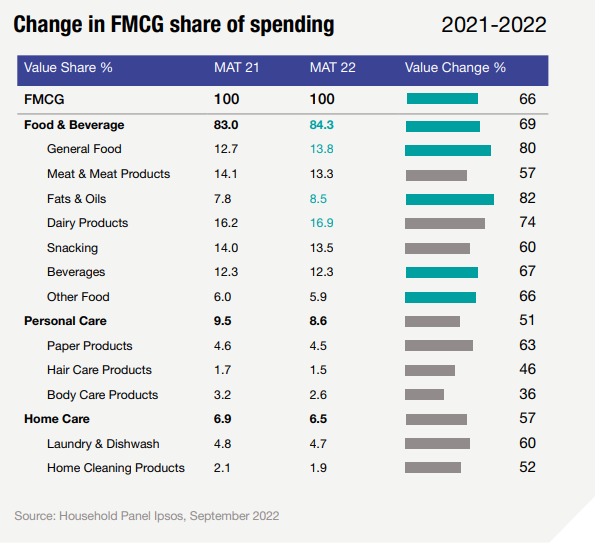

The increase in Household FMCG spending compared to the previous year is below the rate of inflation. This is because:

- AB consumer spending is growing less than other groups. (AB up 57%, others 68%).

- Consumers are visiting more market stores to find the cheapest option, while shopping frequency has decreased.

For managing a limited budget against price increases, the second biggest action taken by consumers is “wandering around different markets to find the cheapest option”, with 51% saying they are doing this.

As a result of this action, according to our household panel findings, the number of different stores visited for FMCG shopping has increased by around 10 percentage points this year. However, the frequency of shopping is decreasing even compared to the pandemic.

Purchases are falling in some non-essential categories

The value increase of each category is at a different level and there are different stories in the background.

- General food increases is closer to the rate of inflation and its ratio as a proportion of FMCG spending is getting higher.

- Meat and meat products are consumed less frequently and by fewer households as a result of high price increases, and therefore their growth is more limited.

- When it comes to snacking, more expensive products such as solid chocolate have been adversely affected, but it’s important to note that products with hunger management benefits such as crackers, cereals, cakes continue to grow in volume.

- The most negatively affected category is body care products, which are seen as more dispensable by consumers. Growth in this category is well below inflation.

How life at home is changing

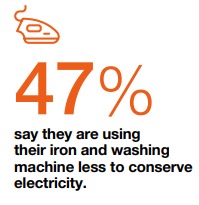

Cleaning is very important to Turkish people, but it has now become an area to cut back on. 47% say they are using their iron and washing machine less in order to conserve electricity.

During the pandemic there was a surge in people getting food takeaways and deliveries, but now 44% say they don’t order food in order to be able to balance their budget. For many it is just not affordable to order food or go out to dinner on a regular basis and this is leading to new simple home-cooked solutions. The common feature of these recipes are fewer ingredients, reasonable price points and fewer dirty dishes.

However, one thing Turkey can’t give up is Netflix. The viewing rate is at the same level as last year: 22%.

|

|

|

|

|

|

Where next?

2023 will be an interesting year for the world as a whole, but with an election coming in Turkey, understanding how people are feeling will be more important than ever. Here are four points to consider in the new year:

- Spot the signals

Society adapts rapidly to changing conditions with new routines. Spotting the signals from early adopters and adapting to business action plans will be more important than ever. At this point, curating social media data and leveraging insights will be key for companies - The Era of Foresight

We should strengthen to design different but realistic predictions about the future and should be prepared for different scenarios. Understanding today is critical for creating learnings but foresight will shape the future - Don’t put up barriers

During this period, we have focused on the barriers to success in every sector and the ways that could be a solution.- Competition is getting more rigid, consider interactions across sectors.

- Channel management and visibility is more essential than ever

- Focus on single, clear and relevant messages via all communication tools (Pack, ATL, BTL, PR…)

- Test and learn across every stage during the innovation process.

- Invest in the future generation

The younger generations are feeling the pressure most coming out of a pandemic and into a hyperinflation crisis at a significant time in their life. When more stable conditions arrive, brands will want to accompany them as they return to “normal” levels of spending. For this reason, they need to invest in this relationship now

Table of content

- Introduction

- Feeling the pressure: Context

- Understanding human psychology during the polycrisis

- Has disruption become the new normal?

- The Indian consumer's response to inflation

- Turkey: Re-designing adaptation in the shadow of hyperinflation

- Brazil: Downsizing VS price rises- making the right choice

- Malaysia: Between money well spent and life well lived

- Understanding Argentina

- France: The end of recklessness

| Previous | Next |

![[WEBINAR] KEYS: Dialling Up the S In Sustainability](/sites/default/files/styles/list_item_image/public/ct/event/2026-06/keys-webinar-sustainability.webp?itok=xPunvoGu)

![[Webinar] Real-World Evidence: Empowering the Patient](/sites/default/files/styles/list_item_image/public/ct/event/2026-05/healthcare-real-world-evidence-webinar.jpg?itok=kT0PwLPQ)