Harnessing the Power of Data

The COVID pandemic has elevated the value of high-quality data and analytics. This has been driven by the acceleration of digital transformation and the increasing importance of becoming more human-centric in order to understand the changing dynamics of consumer attitudes and behaviours.

The COVID pandemic has elevated the value of high-quality data and analytics. This has been driven by the acceleration of digital transformation and the increasing importance of becoming more human-centric in order to understand the changing dynamics of consumer attitudes and behaviours.

To understand this shifting landscape, Ipsos conducted more than 70 client interviews during 2021 around the world and across multiple sectors. We synthesized the key learnings from these interviews to capture how organizations are evolving to harness the power of data and technology for better insights.

Acceleration of data and analytics transformation

From our interviews with clients, we identified the following two key dimensions that best reflect a company’s data maturity and transformation journey:

People and Organization

This dimension focuses on aspects that determine the capabilities of the organization as well as the behaviours they promote. Many companies are creating new roles, structures, and ways of organizing themselves to best leverage their data and analytics resources. Some are moving towards an elevated vision for a data-driven company, while others are looking at recruiting new talents, upskilling legacy teams, and integrating newly-acquired skill sets in order to combine data literacy and business understanding.

Tools and Infrastructure

Companies that are at the forefront of data and analytics have placed a strong priority on developing and nurturing their data ecosystems. These include data sources and data aggregators, as well as specialist agencies across the entire continuum of data preparation, analytics, and marketing activation platforms. Almost all clients are building or nurturing partner and data ecosystems, accessing the best resource and expertise where needed, and complementing their own capabilities. They also expect their partners in their ecosystems to be able to collaborate and act as an extension of their own teams and capabilities.

Where are you on the transformation journey?

We have seen much evidence that companies can clearly enhance productivity and human-centricity through data and analytics. Embracing this whole area of data is a way for marketing/insight functions to create significant value for their business. Consumer and Marketing Insights (CMI) can play a unique role in this respect. They bring deep human understanding (more of the why behind the what), they introduce nuances, contextualize the findings, and they clearly articulate how to best activate those findings within their organization.

Leading CMI organizations that have progressed the furthest in their data transformation journey embrace clear best practices – developing a clear data strategy supported by the right capabilities/partners and a strong culture of data.

Overview

The Covid-19 pandemic has elevated the value of high-quality data and analytics. This has been driven by the acceleration of digital transformation and the increasing importance of becoming more human-centric in order to understand rapidly changing consumer attitudes and behaviours.

Seeking to address this shift, Ipsos conducted more than 70 client interviews during the course of 2021 around the world and across multiple sectors. We synthesized the key learnings from these interviews to capture:

- How organisations are evolving to harness the power of data and technology for better insights.

- What challenges they are facing in realizing the promise of data and analytics.

- What level of adoption and progress they are seeing across their business.

In our interviews we found real differences by, and within, sectors in terms of how companies tackle things. These differences include the way they organize their data and analytics functions and prioritize which business questions to address, and the investments they make around infrastructure and tools as well as in acquiring and building capabilities.

We also uncovered clear and common continuous or emerging themes from the companies we interviewed, including:

- In their search for higher productivity and consumer-centricity, many companies have indeed accelerated their experimentation with more and new sources of data and tools.

- Many have created new departments, roles and ways of working to that effect.

- Several of them are moving from transactional engagements to building and nurturing partner ecosystems that connect teams and functions across the business.

- All need to generate and demonstrate the value of data and analytics, case-by-case. The need to create and foster a culture of data within organisations is recognized across the board.

- The insights function has not always been key in data transformation, but some are clearly now taking a strategic lead, positioning themselves as business translators and driving the cultural transformation.

ACCELERATION OF DATA AND ANALYTICS TRANSFORMATION

We identified two key dimensions that best reflected a company’s data maturity and transformation journey:

- People and Organisation

- Tools and Infrastructure

And we have identified a clear acceleration of investments by many clients on these two pillars.

PEOPLE AND ORGANISATION

The first dimension focuses on aspects that determine the capabilities of the organisation as well as the behaviours they promote. Many companies are creating new roles, structures, and ways of organizing themselves to best leverage their data and analytics resources. For example, L’Oréal recently appointed a global Chief Data Officer, The Coca-Cola Company launched a Platform Services Division as part of their new global structure, and Reckitt launched their interactive Marketing Excellence Virtual Village last year as part of their drive for a step-change in brand building capability and consumer-centricity. Here the ‘Hive’ becomes a dedicated home for their enhanced data and analytics function.

Some are clearly moving to an elevated vision for a data-driven company, like Sanofi for example. Many others are looking at recruiting new talents, upskilling legacy teams and integrating newly-acquired skill sets in order to combine data literacy and business understanding. One of the most important capabilities businesses are seeking to develop is around “storytelling” and communicating the implications from their data and models to their stakeholders.

TOOLS AND INFRASTRUCTURE

Companies that are at the forefront of data and analytics have placed a strong priority on developing and nurturing their data ecosystems. These data ecosystems include data sources and data aggregators, as well as specialist agencies across the entire continuum of data preparation, analytics, and marketing activation platforms.

Almost all clients are building or nurturing partner and data ecosystems, accessing the best resource and expertise where needed, and complementing their own capabilities. They also expect their partners in their ecosystems to be able to collaborate and act as an extension of their own teams and capabilities. In many cases, they are trying to leverage these other sources to substitute for first party data/context data (geopolitics and society) and understand the why behind human behaviours.

Several companies are investing in artificial intelligence (AI)/machine learning (ML) and other data science capabilities. For example, some have explicitly said that they have invested in AI to exploit their own data, identify growth opportunities and better assess gaps in consumer needs.

DIFFERENT PERSPECTIVES AROUND HOW TO ORGANIZE THE DATA AND ANALYTICS FUNCTION

We observed many differences in how companies structure their data and analytics teams across their organisations, with a wide spectrum of approaches. These range from completely internalizing this function, to a hybrid model of internalizing specific functions, to fully outsourcing all analytics to external partners allowing their teams to focus on activating the insights.

INSOURCING VS. OUTSOURCING

A debate exists in the industry as well as within individual companies about whether to build internal data science capabilities or to outsource this function to external partners. The key reasons given for insourcing were the perceived competitive advantages of building this capability and being closer to the business, as well as concerns and challenges about working with external partners for first party data due to privacy and security, and company policies limiting external access to highly confidential customer data. However, the lack of data science talent or willingness to contain costs has resulted in many companies looking to outsource their analytics, either partially or in full.

This is especially true for CPG companies. For example, Unilever has spoken about “insourcing thinking and outsourcing process”.

Another reason behind this debate is the challenge that marketing or insights departments have in recruiting data and analytics talent. Although tech companies have hundreds of Data Scientists throughout their organisation, their insights teams face increasing challenges in accessing Ph.D. level Data Scientists and often partner with external agencies who can provide access to their pool of experts, especially if the analytics involves the integration of survey data.

CENTRALISATION VS. DECENTRALISATION OF DATA SCIENCE

When data activities/ownership are centralised within the enterprise, Consumer and Market Insights (CMI) and marketing teams generally face challenges in accessing the best Data Scientists. In addition, with a centralised model, Data Scientists are seen as being less connected to the business. The ideal scenario for each business function is to have dedicated experts who truly understand their needs and are partnering with them on a daily basis.

When companies adopt a more decentralised structure, with Data Scientists embedded within each business unit, there are different trade-offs such as limited access to the best experts. For example, working with CMI or marketing teams might not always be perceived as the “glory role” for Data Scientists as many prefer to be working on the company’s flagship products or solutions.

There appears to be a growing trend of hybrid structures emerging, with Business Partners or Analysts being based with the end clients and connecting with Data Scientists throughout the organisation.

DIFFERENT PATHS TO CREATE VALUE AND DRIVE HUMAN-CENTRICITY

In terms of focus areas to create more value through data and analytics, most companies recognize the need to be more human-centric, to foster productivity, and enhance their forecasting – all while aiming to find new growth opportunities for their business.

However, the starting point differs by sector first:

Digitally-native tech companies, financial institutions and retailers are rich in data, but they need external partners to help in understanding their competition, reducing churn, enhancing their existing models, and adding human understanding to their data.

FMCG companies often lack and therefore need data (first and third party). They tend to be more consumer aware; however, they want to further leverage the data they have and combine it with other sources to get richer and more accurate answers to their business questions.

The way to get endorsement for data and analytics within companies is usually through creating use cases: identifying business questions, creating cross-functional teams, engaging with Data Scientists and demonstrating value to the business. These use cases can then be scaled up to create maximum impact and adoption across the enterprise.

In several companies, we have observed that the space around productivity and commercial optimisation has been initially covered by IT or Finance. Digital spending optimisation is being handled by the digital/e-business teams and CRM is often covered by a separate entity.

However, some CMI teams are playing a proactive role in shaping the data strategy and extending their role and influence within their organisation.

Some insights leaders are choosing to focus on the forward-looking element of the data agenda (trend forecasts, innovation opportunities, and foresights). However, some marketing/insights teams are taking ownership of the broader data topics, including productivity, and creating true partnerships with other departments like R&D, CRM and Digital, offering a true transversal leadership for their business.

Unlike pure Data Scientists who are sometimes too far removed from the practicality of the business, insights teams are seen as best placed to add value in asking the right questions, contextualizing issues, translating outputs into action, and storytelling for impact.

A key to success for insights teams is to be able to demonstrate value and ROI. We have seen successful examples of advertisers who made a point in quantifying savings/added value to the company and communicated clearly through their organisations.

COMMON NEEDS FOR COMPANIES WE INTERVIEWED:

- Predictive models and solutions.

- Trend forecasts and scenario planning (accentuated due to Covid-19).

- Micro-targeting/precision marketing/ personalisation (make the bridge between marketing strategy and digital activation).

- Enhanced demand forecasts based on deep consumer understanding (and realtime optimisation – pricing, media, etc.).

- Identification of growth and innovation opportunities.

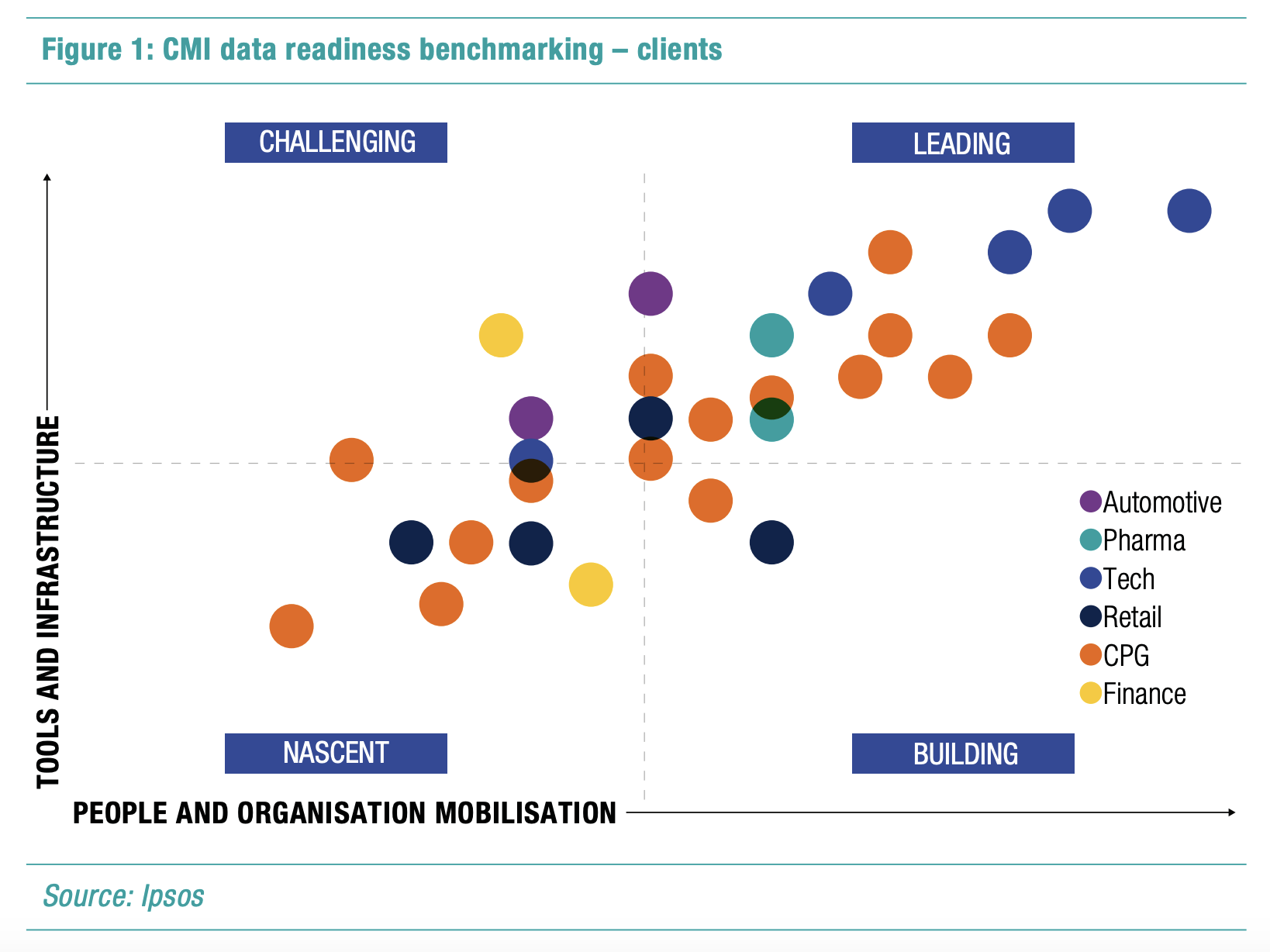

CMI DATA MATURITY MODEL AND IMPORTANCE OF CULTURE

In order to get a sense for what drives CMI data readiness and how companies benchmark against each other, we examined seven dimensions categorized into two broad overall categories for People and Organisation, and Tools and Infrastructure:

- People and Organisation: data sophistication, CMI data impact, data culture, organisation

- Tools and Infrastructure: data ecosystem, data availability, tools and systems

We evaluated each of the companies against the seven dimensions and mapped them based on the two axes of People and Organisation, and Tools and Infrastructure (see Figure 1).

Tech and retail sectors have a natural advantage due to access to tremendous amounts of first party data. However, owning proprietary data did not necessarily place companies into the ‘leader’ section of the quadrant as some lacked capabilities in other dimensions such as business impact and data sophistication.

Interestingly, there appears to be a paradox revolving around big data and advanced analytics for many of these tech companies. Generally, once datasets reach a certain size, such as petabytes, complex modelling approaches become time and cost-prohibitive and many of the useful analytics conducted tend to be simple. This is because speed is often more critical than perfection when dealing with daily petabytes of data. This data obesity is a real challenge for many organisations and few feel that they have uncovered the full value from their existing data.

Tech has another advantage due to its digitally native culture and core competence in data, whereas retailers do not have the same level of access to new technologies and talent that tech companies can acquire. For example, Microsoft’s Data and Analytics Platform team has created an advanced data integration and curation system utilizing its Azure cloud and Power BI solutions for integrating and validating thousands of third party market research studies to support its product development and marketing end users. This central analytics platform allows the end users to analyze these data sets using dashboards and query tools as well as explore the relationships between the perceptual data and behavioural data that Microsoft collects from its users. Meanwhile, retailers have become very proficient in maximizing their operational efficiency through their analysis of their customer data.

Finance and healthcare companies also have access to vast amounts of first party data, but they are operating in highly regulated industries and often have a very risk-averse culture when it comes to accessing and analyzing sensitive customer data for market research and marketing purposes.

Many automotive companies have strong aspirations to become more like tech companies, but they are also held back by legacy culture, skill sets, and access to data. While there are some automotive companies that are investing heavily in acquiring new tech talent, most do not have the luxury of making investments during the pandemic as this was one of the key industries negatively impacted during the initial stages of Covid-19.

The FMCG sector is very much polarized with some companies aggressively investing in data and analytics and actively promoting their advancements in this space. However, other FMCG companies have been slower and more conservative with their investments in data science. In addition, the CMI functions for these lagging companies often struggle to secure a seat at the table when it comes to their company’s overall data and analytics agenda.

The biggest barrier to progress is in acquiring and developing talent who are confident and fluent in the world of data and analytics. Many companies are expressing the need to have more data translators; people who understand data and analytics and can clearly articulate the business implications from data and confidently provide actionable recommendations for the business. This is a broadly new skill set required to achieve more impact by CMI teams and recognized by most CMI leaders as a core competency for their teams.

Among all factors we analyzed, culture has the strongest correlation with overall data maturity. A large proportion of companies recognize the need for their organisation to upskill in the data space and advance in cultural transformation.

WHERE ARE YOU ON THE TRANSFORMATION JOURNEY?

We have seen much evidence that companies can clearly enhance productivity and human-centricity through data and analytics. Embracing this whole area of data is a way for marketing/insight functions to create significant value for their business. CMI has the opportunity to play a unique role in this respect. Those insights or insight and analytics teams who are further advanced are best at combining what some of our clients call the “math and the poetry” and they act as business translators. They start by helping stakeholders best define their business needs; they understand what various data sources and data science can bring to address a specific business question while also capturing potential limitations and gaps. They bring deep human understanding (more of the why behind the what), they introduce nuances, contextualize the findings, and they clearly articulate how to best activate those findings within their organisation.

Leading CMI organisations that have progressed the furthest in their data transformation journey embrace two key best practices – developing a clear data strategy supported by the right capabilities/partners and a strong culture of data.

The most important aspect of a data strategy is in its clarity, as each company has its own unique set of circumstances and capabilities and can be successful if they can execute their strategy well. The most important factor that impacts execution is the culture of the company, especially with regards to data.

CULTURE OF DATA

When we evaluated a company’s culture regarding data and analytics, there were several key themes and characteristics that we identified among the leading companies in this space. Most of the leading companies encouraged experimentation and collaboration, and embraced taking calculated risks by conducting several pilot projects. Essentially, they were not afraid to fail and focused on building knowledge and capabilities through their data initiatives.

In addition, these leading companies were very clear about the types of skill sets they needed to improve their capabilities and utilized a combination of acquiring and developing the talent necessary for creating a leading analytics organisation. For CMI, these skills include data literacy, storytelling and business acumen.

And finally, leading companies are developing a strong and diverse ecosystem of data and analytics partners with a clear understanding of their own core competencies while outsourcing the non-core activities to their partners. A good example of an ecosystem that any company can tap into is in China, where Alibaba has created an AI-powered Uni-Marketing platform. This platform enables brands to integrate their own research and CRM data with Alibaba’s unified database of 600M+ users that tracks their lifestyle, shopping, media consumption, and payment data for precision targeting as well as marketing attribution.

A CHECKLIST FOR YOUR TRANSFORMATION JOURNEY

Each company is at a different stage of maturity with regards to data and analytics and will need to determine the best path based on its unique set of circumstances and capabilities.

Below are some questions to consider for accelerating your transformation journey:

- What is your data and analytics strategy? Have you identified and prioritized business areas you want to explore and are you considering building use cases for them?

- Have you assessed the level of data readiness and capability of your insights function?

- What are the core competencies that you want to develop for the CMI function, and which of these would your stakeholders be better served by outsourcing?

- And, most importantly, have you developed a culture of data that facilitates the execution of your strategy?

![[WEBINAR] 2025 KEYS: The Year in Review](/sites/default/files/styles/list_item_image/public/ct/event/2025-11/Slide8_0.PNG?itok=vI55-tRN)