Ahead of COP27, Canadian public support for policies encouraging sustainable technology adoptions trails behind most other countries surveyed

Toronto, ON, November 6, 2022 – Ahead of COP27, Canada is gearing up to showcase its ambitious plans to cut carbon emissions in its efforts to demonstrate strong local action and global leadership on climate change. A new global Ipsos poll paints a complex picture of Canadian citizen support on the subject.

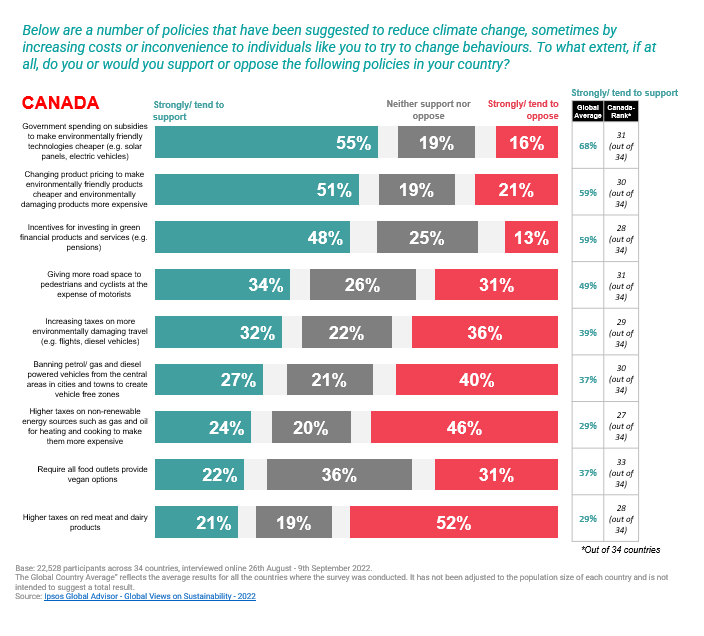

The latest Ipsos Global advisor research studies citizen support across 34 countries on a range of policies to help tackle climate change. The results highlight that while support varies by topic and region, for almost all the suggested policies to help combat climate change, Canadians feature at the bottom of the list of 34 countries in extending their support.

At an overall level, the most popular policy, with an average of almost 7 in 10 (68%) citizens across the 34 countries surveyed saying they would support it, was for government spending on subsidies to make environmentally friendly technologies cheaper (e.g., solar panels, electric vehicles), followed by more than half (a global average of 59%) who would also support changing product pricing to make environmentally friendly products cheaper (conversely environmentally damaging products more expensive) and providing incentives for investing in green financial products and services (e.g., pensions) (59%).

In contrast, Canadians express much lower support and feature among the countries with the lowest approval (among the 34 countries surveyed). While a slim majority of Canadians would approve of subsidizing green technologies by the government (55%) and modifying product pricing to make environmentally friendly products cheaper (51%), most other policy suggestions would only be supported by less than one-third of Canadians. In fact, for all of the policy initiatives listed, Canada ranks among the least likely to support, i.e. between rank 27 to 31 (out of 34 countries).

Although there is a general alignment across the various demographic sub-groups, women and younger Canadians tend to express higher agreement in support of the proposed changes. The chart below breaks down support among these key demographic groups - gender and age.

Although there is a general alignment across the various demographic sub-groups, women and younger Canadians tend to express higher agreement in support of the proposed changes. The chart below breaks down support among these key demographic groups - gender and age.

Support for Suggested Policies: By Gender and Age

|

|

Men |

Women |

18-34 |

35-54 |

55+ |

|

Government spending on subsidies to make environmentally friendly technologies cheaper (e.g. solar panels, electric vehicles) |

51% |

60% |

59% |

55% |

53% |

|

Changing product pricing to make environmentally friendly products cheaper and environmentally damaging products more expensive |

46% |

55% |

53% |

53% |

47% |

|

Incentives for investing in green financial products and services (e.g. pensions) |

43% |

53% |

56% |

46% |

44% |

|

Giving more road space to pedestrians and cyclists at the expense of motorists |

33% |

35% |

41% |

33% |

28% |

|

Increasing taxes on more environmentally damaging travel (e.g. flights, diesel vehicles) |

32% |

31% |

39% |

27% |

28% |

|

Banning petrol/ gas and diesel-powered vehicles from the central areas in cities and towns to create vehicle-free zones |

27% |

27% |

32% |

26% |

24% |

|

Higher taxes on non-renewable energy sources such as gas and oil for heating and cooking make them more expensive |

25% |

23% |

29% |

24% |

20% |

|

Require all food outlets to provide vegan options |

16% |

28% |

33% |

19% |

16% |

|

Higher taxes on red meat and dairy products |

18% |

24% |

31% |

19% |

14% |

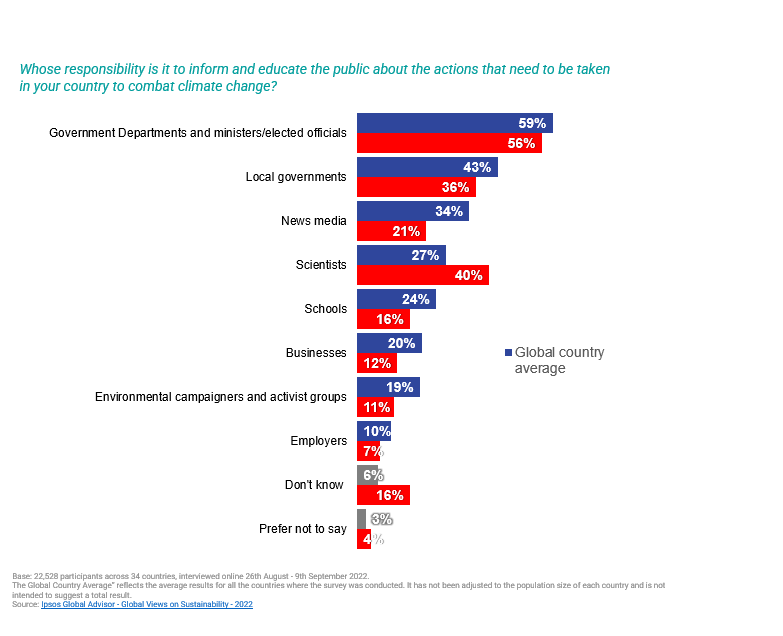

Whose responsibility is it to educate the public?

There is notable consensus at a global level that the responsibility for educating the public on climate change lies with government departments and ministers/elected officials (59%). Just over 4 in 10 think it is the responsibility of local governments and just over a third (34%) would consider news media to be responsible. Then scientists (27%), schools (24%), business (20%) and environmental campaigners/activist groups (19%).

While Canadian opinions are largely in line with the trends observed at the global level, when it comes to Canada, higher importance is placed on the role of scientists in the matter. Scientists come fourth in terms of responsibility for climate education based on the global average (27%) but are second in Canada (40%), France (35%) and Great Britain (35%).

While the government and scientists might be seen as the leading players in climate education, there is a role to be played by the private sector as well. Interestingly, expectations placed by younger Canadians on the role of businesses and their employers are much higher than their older counterparts [Businesses: 17% among those 18-34 yrs of age Vs. 8% among 50+; Employers: 10% among 18-34 Vs. 6% among 50+]. The same trend holds for the average of 34 countries surveyed, highlighting the growing expectations from younger and more socially active citizens and therefore, the increasingly important role of CSR initiatives and ESG functions in the private sector.

About the Study

These are the results of a 34-country survey conducted by Ipsos on its Global Advisor online platform. Ipsos interviewed an international sample of 22,528 adults aged 18-74 in the US, Canada, Republic of Ireland, Israel, Malaysia, South Africa, and Turkey, 20-74 in Thailand, 21-74 in Indonesia and Singapore and 16-74 in all other countries between 26th August and 9th September 2022.

The sample consists of approximately 1,000 individuals in each of Australia, Brazil, Canada, mainland China, France, Germany, Great Britain, Italy, Japan, Spain, and the U.S., and 500 individuals in each of Argentina, Belgium, Chile, Columbia, Hungary, India, Indonesia, Ireland, Israel, Malaysia, the Netherlands, Peru, Poland, Romania, Saudi Arabia, South Africa, Sweden, Thailand, Turkey and the United Arab Emirates.

17 of the 34 countries surveyed online generate nationally representative samples in their countries (Argentina, Australia, Belgium, Canada, France, Germany, Great Britain, Hungary, Italy, Japan, the Netherlands, Poland, Romania, South Korea, Spain, Sweden and United States).

The samples in Brazil, Chile, mainland China, Colombia, India, Indonesia, Ireland, Malaysia, Mexico, Peru, Saudi Arabia, Singapore, South Africa, Thailand, Turkey and United Arab Emirates are more urban, educated, and/or more affluent than the general population. They are not nationally representative of their country. The survey results for these countries should be viewed as reflecting the views of the more “connected” segment of their population.

“The Global Country Average” reflects the average results for all the countries where the survey was conducted. It has not been adjusted to the population size of each country and is not intended to suggest a total result.

Where results do not sum to 100 or the “difference” appears to be +/-1 more/less than the actual, this may be due to rounding, multiple responses, or the exclusion of “don’t know” or not stated responses.

The precision of Ipsos online polls are calculated using a credibility interval with a poll of 1,000 accurate to +/- 3.5 percentage points and of 500 accurate to +/- 5.0 percentage points. For more information on Ipsos’ use of credibility intervals, please visit the Ipsos website.

The publication of these findings abides by local rules and regulations.

For more information on this news release, please contact:

Sanyam Sethi

Vice President, Ipsos Public Affairs

[email protected]

About Ipsos

Ipsos is the world’s third largest market research company, present in 90 markets and employing more than 18,000 people.

Our passionately curious research professionals, analysts and scientists have built unique multi-specialist capabilities that provide true understanding and powerful insights into the actions, opinions and motivations of citizens, consumers, patients, customers or employees. We serve more than 5000 clients across the world with 75 business solutions.

Founded in France in 1975, Ipsos is listed on the Euronext Paris since July 1st, 1999. The company is part of the SBF 120 and the Mid-60 index and is eligible for the Deferred Settlement Service (SRD).

ISIN code FR0000073298, Reuters ISOS.PA, Bloomberg IPS:FP