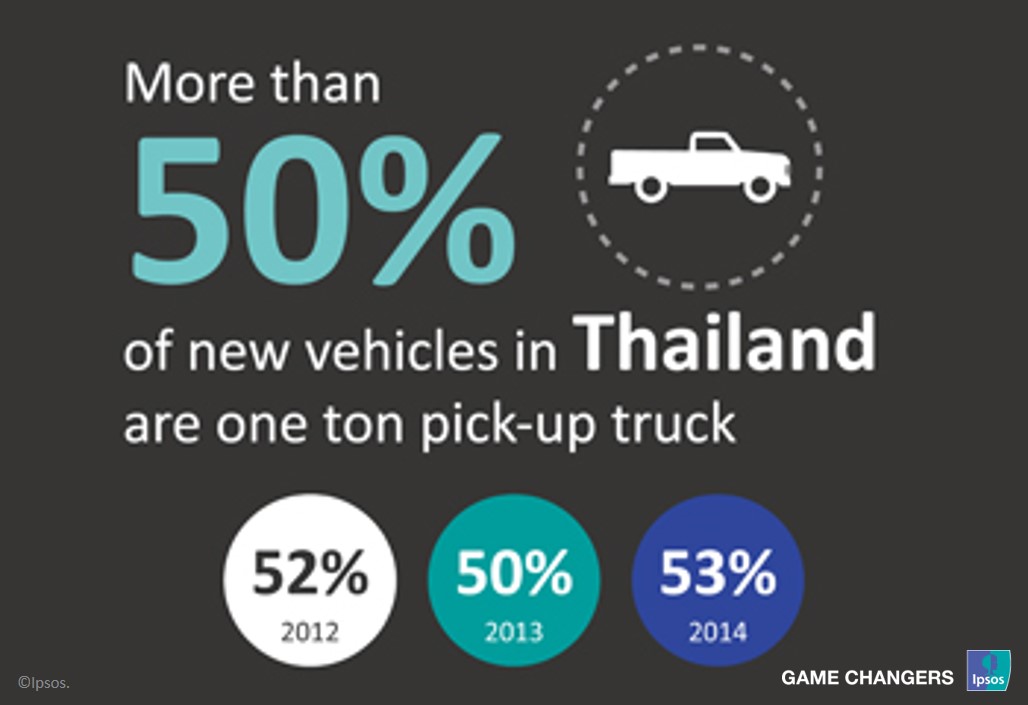

Trends And Opportunities in Thailand's Emerging Automotive Market

Thailand has witnessed a sharp decline in new car sales in recent years. In common with other automotive markets, the OEMs and dealerships have also seen a steady decline in the profit margins within the new vehicle sales business, along with an extension of car life. All of this makes the after-sales business increasingly important in the efforts to maximise revenues and profit across the industry. At the same time, the country is experiencing significant change within the after-sales market, putting the OEMs’ market share at risk. This Industry report looks at the opportunities and trends within the Thai automotive after-sales market, including how the changes in customer behaviour are giving rise to a need for existing and new players to re-examine their after-sales business model.

Many OEMs and automotive component manufacturers are seeking to develop stronger revenue streams and this is bringing the aftersales market into greater focus. This market offers significant potential to the industry as a strong revenue stream.

Our latest publication on the Thailand Automotive Aftersales market highlights that there will be more than 18 million passenger vehicles in Thailand by 2020, thereby offering an attractive opportunity in the automotive aftermarket arena.

Our latest publication on the Thailand Automotive Aftersales market highlights that there will be more than 18 million passenger vehicles in Thailand by 2020, thereby offering an attractive opportunity in the automotive aftermarket arena.

Even though parts quality is the most important criterion for selecting the aftermarket channel, the non-OEM parts has a significant share in the market.

The number of out-of-warranty passenger vehicles in Thailand is expected to exceed 14 million units by 2020, with more than five million units between the age of three and eight years.

The number of used car sales is expected to grow with a CAGR of 5.5% during 2015-2020, due to an expected decrease in used car prices and an increasingly affluent middle-class population.

Bangkok will remain the key driver of the independent aftermarket, while the North and the Northeast will also be key markets contributing to aftermarket growth in the coming five years. The growth in passenger vehicle ownership, specifically in the Northeast, is expected to be driven by growing cross-border trade between Thailand and Lao PDR.

The uncertified independent workshop is still the channel with the most outlets, however, branded service providers and certified independent workshops are well-positioned to benefit from the development of increased demand from out-of-warranty car owners.

While consumers still have a clear preference for OEM branded parts, over 50% of consumers are willing to use non-OEM parts if the OEM parts are perceived as too expensive.