Demographic matters

Three and a half years later, in the early hours of 15 April 2023, President Macron pushed through an increase in France’s official pension age from 62 to 64 in controversial circumstances. This was most certainly not a moment of national consensus, as the protests on the streets and the opposition in parliament showed.

But France is not alone in having to face its demographic fate. Almost every country in the European Union is currently implementing an unpopular pension reform.

Compromises are often necessary. The reform approved by referendum in neighbouring Switzerland in 1995 has only just reached its final stage, 27 years after its enactment, since it only affects women born after 1960. The UK government has been increasing its pension eligibility age (currently 68 for young people entering the job market), but in a very incremental way which has not been without its problems.

And this is not just a European issue. Singapore is raising its retirement age to 63, on a path to 65. Quebec is changing its pension plan to encourage people to work past the normal retirement age of 65 (the minimum age is still 60).

The bigger picture here is not just that populations are ageing. They are not being replaced. Governments around the world are only just starting to get to grips with tomorrow’s reality, which is one of population decline.

In 2023 India officially overtook China as the world’s most populous country. But India’s fertility rate – the average number of children a woman gives birth to over the course of her lifetime – now stands at 2.0. As Amit Adarkar writes in the India chapter of the Almanac, the country’s traditional pyramid-shaped population profile is now morphing into a pear-shaped demography. It too will see its population decline in the second half of this century.

Meanwhile, China (whose fertility rate is only 1.19) is one of the 36 countries whose population is already declining.

The politics of demography

We are already starting to see the repercussions of demographic change away from the realm of pension and pension reform.

We are already starting to see the repercussions of demographic change away from the realm of pension and pension reform.

Population decline has led to the closure of 2,600 Italian kindergartens and primary schools in the last 10 years, resulting in almost 1.5 million fewer school places than a decade ago. We see a similar picture in Japan and South Korea, where universities are now exploring "survival strategies" and working out how many people need to be trained in specialisations such as obstetrics and gynaecology in an era of low birth rates.

In Italy, Prime Minister Giorgia Meloni has set out an explicit pathway to “promote parenthood, while the dominant culture has been saying the opposite for years”. A new ministry for Family, Natality and Equal Opportunities has been set up. We can expect to see debates heat up in more countries very soon, as politicians from different sides of the political spectrum grapple with what is becoming an increasingly important issue. Ipsos’ Darrel Bricker explores this topic in more detail elsewhere in this year’s Almanac.

Marketing matters: who to target?

Meanwhile, business decision-makers run the risk of getting stuck in their own particular bubbles. Replacing the Millennials who went before them, the gaze of much marketing activity is now firmly fixed on Generation Z, born between 1996 and 2012.

There are, of course, lots of good reasons for putting young people at the centre of new innovations and communications. They are the adults of tomorrow. They power new trends. And they are attractive – ideal candidates for brand ambassadors.

On the other hand, there are not all that many of them. Around the world, 32% fall into the “Generation Z” category, and in many countries the figure is much lower than that – Germany, Italy and Japan being three examples (all recording just 14% of their populations aged 10-24)

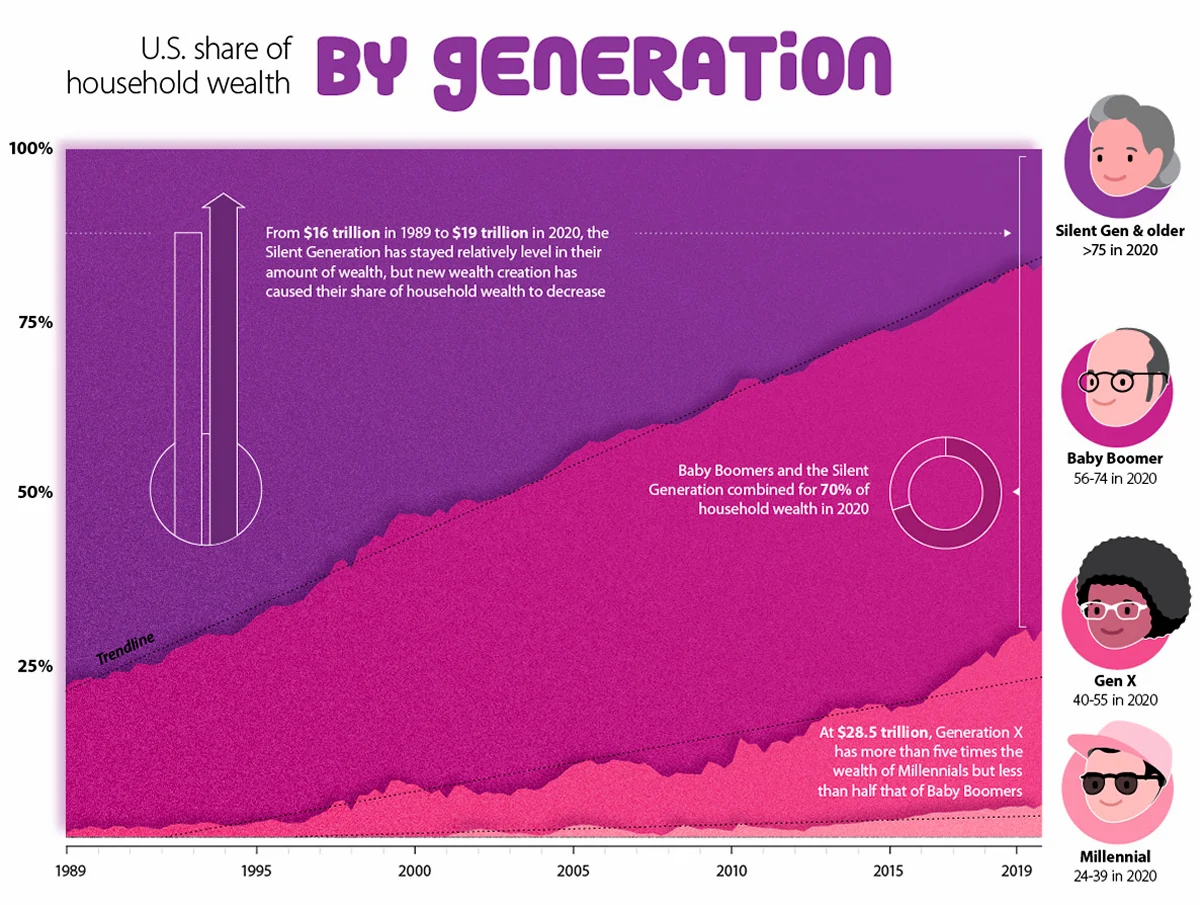

What’s more, Gen Z don’t have that much money. In the US, it’s the “Baby Boomers” who control nearly 70% of the household wealth. Some 77% of them describe themselves as “financially stable”. And they are in good shape: 56% “feel good both physically and mentally”, very much in line with Millennials (57%).

Getting closer to our target markets involves being clear about the nuances, and our latest research finds mature adults to be cautious with their money (more likely than others to save for “no particular reason”) and not particularly flamboyant (just 14% say they “admire people who own expensive homes and cars”).

How to unlock this spending power? Advertising is an obvious route. Our creative research team looked at their database of ads and found that just 8% of commercials feature them in a leading role. Time for a reset?

Three things to think about

-

Whether it’s the labels we use to describe age groups or quantifying the Generational Power Index for our category, are we being too simplistic in how we think about generations?

-

When it comes to different types of mature adults i.e., who are they, what do they buy, and how best to engage with them to unlock their spending power. How much do we really know about them?

-

And, when it comes to research, is it OK to have a cut-off point for respondents at age 65 or 75? Are we asking the right questions of the right people?

This article shares some of the findings from a 2023 Ipsos research programme designed to help us better understand the dynamics of generational analysis and demographic change. For more, please take a look at our report and let us know what you think.