The Endurance Economy at Mid-Year 2026

At the start of 2026, many organizations were still planning against a familiar assumption: that easing inflation and stabilizing interest rates would lead to a gradual return to normal economic conditions. Six months in, that assumption looks increasingly misaligned with reality.

Canada is not moving through a typical recovery cycle. It is operating in a period of sustained constraint. The question for business leaders is no longer when conditions will normalize. It is how prolonged adaptation is reshaping the market and whether current strategies are aligned to that reality.

Taking Stock of the Endurance Economy

One of the advantages of publishing annual outlooks is that they create a record. Assumptions can be revisited, interpretations tested, and emerging patterns evaluated against subsequent events. As we reach the midpoint of 2026, we think it’s a good time to take stock of the Endurance Economy.

Many of the ideas that would eventually form Ipsos’ Endurance Economy framework first appeared in our 2024 and 2025 end of year outlooks for Canada. At the time, the prevailing expectation (or maybe it was hope) was that as inflation eased and interest rates moderated, Canadians would gradually return to a more familiar economic and psychological equilibrium. Our interpretation was different.

We argued that Canadians were not simply moving through a temporary period of disruption but entering a longer phase of adaptation. In late 2024, we noted that the feeling of falling behind financially appeared increasingly entrenched in the Canadian psyche. That observation mattered not because it was dramatic, but because it suggested duration. Affordability pressures were becoming embedded in how Canadians interpreted their everyday economic reality.

In our 2025 Review and 2026 Outlook, we extended that view. We described 2025 as a period of transition rather than resolution and argued that Canadians were increasingly making decisions through the lens of financial constraint and resilience rather than expectation of improvement. We also suggested that many of the pressures shaping Canada including housing affordability, productivity, healthcare capacity, demographics, and competitiveness were structural in nature and unlikely to resolve quickly.

Together, those observations formed the foundation of the Endurance Economy Framework, which Ipsos formally released in January 2026 at our annual Canada Now Canada Next event. The core proposition of the framework remains straightforward: Canada is not moving through a typical economic cycle. It is moving through a prolonged period of adjustment in which households, businesses, and institutions are adapting to conditions increasingly experienced as structural rather than temporary. Six months into 2026, that interpretation appears increasingly relevant.

The Bank of Canada Can Stabilize the Economy. It Can't Restore Confidence.

The Bank of Canada's latest decision to hold interest rates and its lowering of 2026 expected growth seems to confirm that the Bank is comfortable that monetary policy is now appropriately positioned. Inflation is moving toward target, interest rates have fallen considerably from their peak, and economic growth is expected to improve modestly over the coming year.

Yet the Bank's report also carries a more cautious message. Growth expectations remain modest, global trade tensions continue to cloud the outlook, productivity remains weak, and uncertainty features prominently throughout the Bank's assessment of the economy. Rather than describing an economy preparing to accelerate, the report describes one searching for stability.

Viewed through the lens of Ipsos' Endurance Economy framework, the July announcement does not signal the end of Canada's adjustment period. Instead, it reinforces our central thesis: while inflation may be normalizing, Canadians continue to navigate a prolonged period of financial caution, constrained optimism and structural uncertainty.

Three Signals That Define the Framework

Three ideas consistently appeared in our earlier work and continue to shape the current environment.

First, affordability has remained the dominant lens through which Canadians interpret economic conditions. Inflation has moderated, yet affordability continues to shape political debate, consumer behaviour, and perceptions of economic progress. The issue has proven more durable than the post-pandemic inflation cycle that helped elevate it.

Second, adaptation has become more important than recovery. Rather than waiting for conditions to return to previous norms, Canadians have increasingly adjusted their behaviours under new constraints. Delayed milestones, heightened value-seeking, provider switching, and sensitivity to price increasingly appear less like temporary responses and more like emerging behavioural norms.

Third, Canada has become more visibly bifurcated. National averages continue to suggest relative stability, but lived experiences are diverging. Asset-owning households experience the economy differently than income-dependent households. Younger Canadians face different realities than older Canadians. In addition to higher levels of unemployment younger Canadians are delaying life milestones such as marriage, having children and home purchases.

Regional experiences also vary considerably. According to Statistics Canada provincial economic accounts, GDP per capita in 2024 was approximately 40% higher in Alberta than the national average and roughly 40% lower in Prince Edward Island, highlighting the uneven economic realities facing Canadians across the country. These overlapping forms of divergence are becoming defining features of Canada’s economic landscape.

The Language of Structural Change

One of the more notable development in 2026 is a growing convergence in how Canada’s challenges are being described.

Across housing, productivity, healthcare, fiscal sustainability, labour markets, and competitiveness, the language of structural constraint has become increasingly common. Housing affordability is routinely discussed in terms of supply limitations and long-term demand imbalances. Productivity is framed as a structural challenge linked to investment and innovation. Healthcare pressures are increasingly attributed to demographic realities and capacity constraints. Fiscal debates increasingly focus on long-term drivers such as aging populations and debt-servicing costs.

This shift in language is significant because it reflects and reinforces a broader shift in expectations. Cyclical challenges imply that conditions improve with time and conventional policy adjustments. Structural challenges imply that adaptation and institutional change are required. For organizations, this changes planning horizons, investment assumptions, and risk assessments.

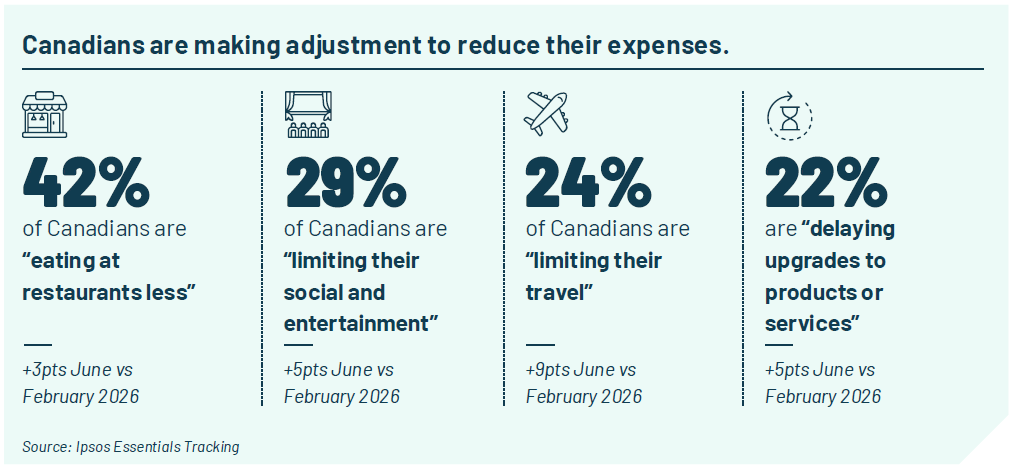

Consumers Have Adapted and the Evidence Continues to Accumulate

Consumers have not stopped spending but have changed how they spend. They consider anticipated future affordability pressures as well as responding to current financial circumstance. They are more deliberate in their purchasing decisions, more sensitive to price changes, more willing to switch providers, and more likely to defer discretionary purchases. The horizon has also shifted. Consumers are asking not only whether they can afford something now, but whether they can continue to afford it six months or two years from now. As a result, transparency, predictability, and perceived fairness have become increasingly important components of value.

The changing consumer behaviour does not necessarily mean the economy is in decline. Inflation has moderated and labour markets remain relatively resilient. Economic growth has been flat, but a modest recovery is expected. What has changed is the relationship between improving macroeconomic indicators and lived experience. Stability at the aggregate level is no longer translating into a comparable sense of relief at the household level.

Canadian household net worth reached record levels in 2025. For households with accumulated wealth, those assets are helping to sustain spending despite ongoing affordability pressures. For income-dependent households, that buffer does not exist. The result is a more fragmented picture of household financial health than aggregate measures suggest. Sustained consumption does not necessarily signal broad-based financial comfort. In some cases, resilience reflects accumulated assets rather than improving cash flow. What emerges is not a single Canadian experience but multiple Canadian experiences unfolding simultaneously with some households able to absorb volatility, others highly exposed to shifts in employment or increases in everyday expenses.

Ipsos Essentials Tracking shows that while all households, regardless of income level are exposed to the high cost of living it is the households at the lower income level who are most likely to say that they take a price first attitude into each purchase decision at 65%. Households at the higher income level are also impacted but to a lesser extent with 42% saying that their purchase decisions are driven by a price first mentality.

Politics Is Beginning to Reflect the Same Reality

Canadians are being held, not healed. What keeps the Endurance Economy from tipping into recession may be political management. Federal and provincial governments have increasingly deployed targeted transfers, rebates, and benefit enhancements not as stimulus but as floor maintenance: keeping household distress below the threshold of political crisis. These interventions may alleviate immediate pressure without materially altering the structural drivers of affordability stress. The result is a structurally prolonged plateau: chronic constraint managed carefully enough to remain politically tolerable.

The External Variable

The Endurance Economy was never built on the assumption of domestic stability alone, and 2026 has reinforced why.

Two external developments are particularly relevant. The renegotiation of CUSMA, now operating under conditions of considerable political uncertainty, has introduced sustained ambiguity into business planning and long-term trade confidence. For an economy as trade exposed as Canada’s, prolonged uncertainty about the terms of access to its largest market is a structural drag on business confidence with direct household implications.

The escalating and on again/off again tensions involving Iran represent a second and distinct category of external risk. Energy price volatility and potential disruption to global shipping lanes carry implications for inflation, interest rates and the global economic backdrop against which Canada’s domestic pressures are playing out.

These forces do not alter the fundamental logic of the Endurance Economy. Canada’s structural challenges remain primarily domestic in origin. But external developments act as amplifiers, prolonging caution, delaying investment decisions, and reinforcing the adaptive behaviours already visible among consumers and businesses. The result is not a deviation from the framework but a complication of its timeline.

What Would Signal a Shift?

As with any framework, the Endurance Economy should remain open to evidence. Ipsos has identified a specific set of conditions that would indicate Canada is meaningfully transitioning out of the current phase of adaptation and toward a Confident Economy.

Those conditions are not simply macroeconomic. They are perceptual and behavioural. Sustained net personal financial optimism at or above +25 points, with no major demographic or regional cohort falling below +10, would represent a meaningful threshold. So would evidence that younger Canadians and lower-income households are participating in any recovery, not just asset-owning households. Wage growth that outpaces essential costs, a measurable easing of housing affordability for first-time buyers, and a demonstrated decline in consumer sensitivity to price would all contribute to that case.

To date, evidence for such a transition remains limited. The markers of endurance deferred milestones, heightened value-seeking, and reduced discretionary spending remain broadly intact.

Endurance as the New Baseline

The most important lesson from the first half of 2026 is not that Canadians are struggling or that the economy is flat. It is that Canadians are adapting. Households continue to recalibrate expectations. Businesses continue to adjust strategies. Policymakers continue to confront challenges increasingly understood as structural rather than temporary.

The question is no longer whether Canadians can endure. The evidence suggests they already are. The more important question is what prolonged endurance changes.

Two years ago, we suggested Canada was entering a period defined less by recovery and more by adaptation. Midway through 2026, the evidence has not reversed that view.

The Endurance Economy is not a forecast of decline. It is a framework for understanding how people, institutions, and markets adapt under sustained pressure. As the second half of 2026 unfolds, the direction of travel remains broadly consistent. Yet the forces shaping that journey are becoming more complex. Domestic pressures remain structural. Political expectations are adjusting. External uncertainties continue to evolve.

If the first phase of the Endurance Economy was about recognizing adaptation, the next phase may be about understanding how prolonged adaptation ultimately reshapes the definition of normal itself.

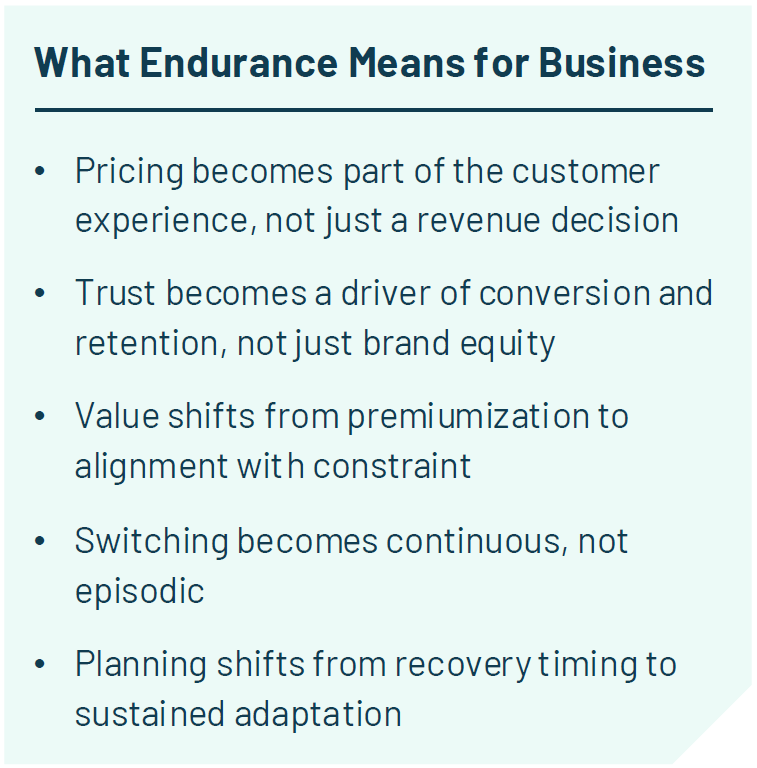

For business leaders, the Endurance Economy has a practical implication: your customers are not waiting to feel better before they decide. They have recalibrated what they expect, what they will pay, what they will tolerate, and who they will trust. The organizations that recognize this and build their value propositions, pricing strategies, and customer relationships around sustained constraint rather than anticipated recovery will be better positioned than those still waiting for conditions to normalize.

![[WEBINAR] 2025 KEYS: The Year in Review](/sites/default/files/styles/list_item_image/public/ct/event/2025-11/Slide8_0.PNG?itok=vI55-tRN)