U.S. consumer sentiment remains low despite slight uptick

Washington, DC, July 14, 2022 – Americans’ economic sentiment sees an uptick of 2.5 points from two weeks ago in the Ipsos-Forbes Advisor U.S. Consumer Confidence Tracker. However, sentiment remains below the 50-point mark, a threshold crossed in mid-June for the first time since December 2020.

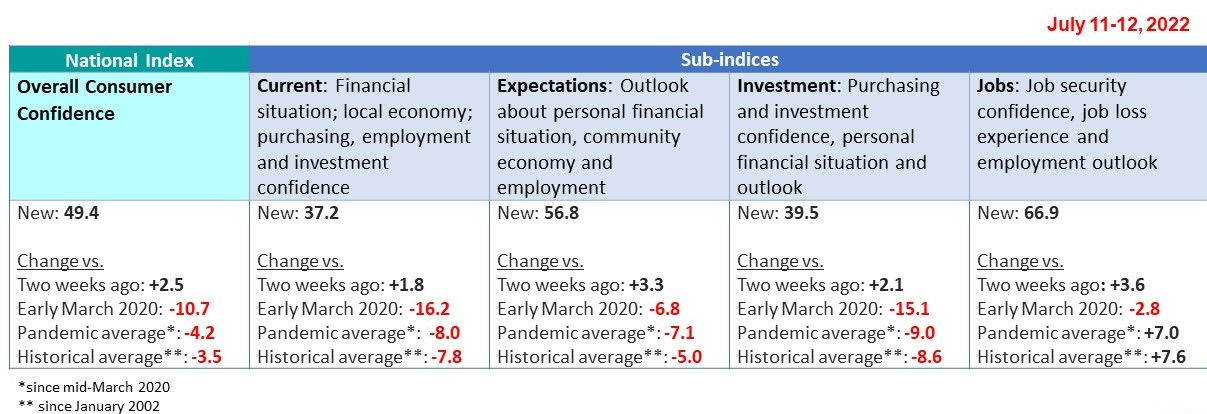

After falling to their lowest points in more than a decade, the Expectations and Investment sub-indices both experience an uptick this week, halting consecutive declines of six and four readings, respectively. Following another month of strong job growth in June, as reported by the Bureau of Labor Statistics, Americans’ job sentiment remains relatively high, as the Jobs sub-index recorded its largest wave-over-wave increase of the year this week.

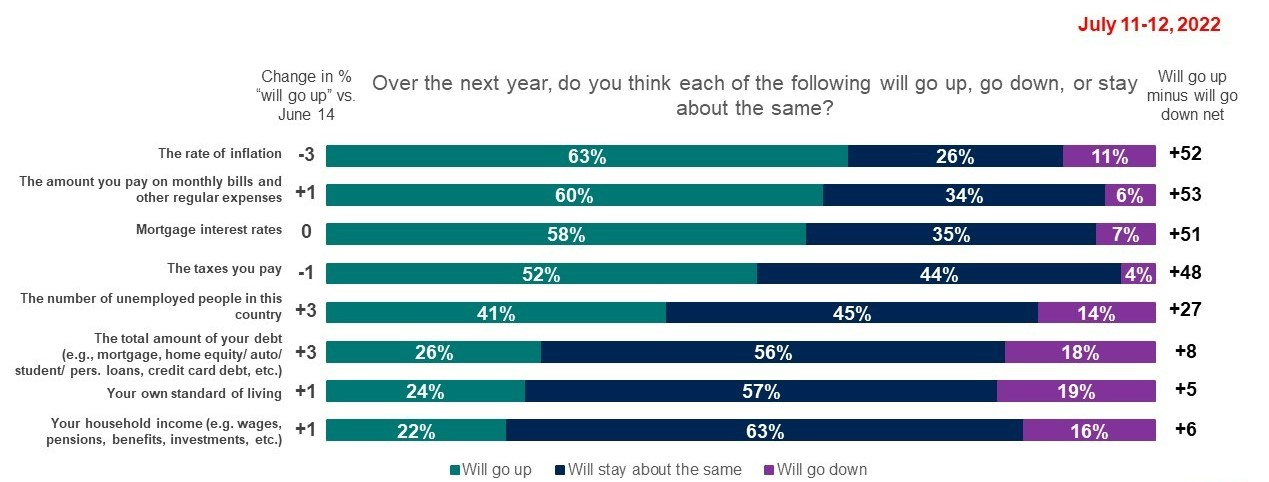

This week’s survey finds that while purchasing confidence saw a small uptick, two in three Americans still feel less comfortable purchasing both big-ticket items and other household goods than they were several months ago. Lastly, majorities of Americans continue to expect inflation, monthly bills, mortgage rates, and taxes to rise, and four in ten now expect the number of unemployed people to continue to go up.

Read the full story from Forbes Advisor here.

Learn more about the Ipsos Global Consumer Confidence Index and sub-indices via the interactive portal, Ipsos Consolidated Economic Indicators (IpsosGlobalIndicators.com) including graphic comparisons, trended data and all the questions on which they are based.

Detailed Findings

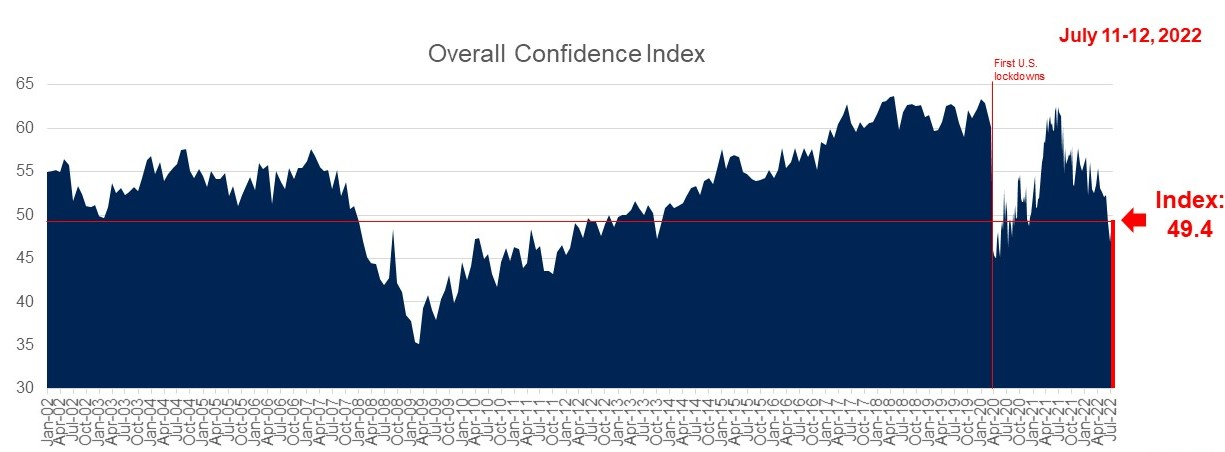

1. Scoring at 49.4, the latest Overall Consumer Confidence index has increased by 2.5 points from two weeks ago.

- The Overall Confidence Index is currently 4.2 points below the pandemic average and 10.7 points below where it stood in early March 2020 prior to the first lockdowns (60.1). The index now sits just 3.5 points lower than its 20-year historical average.

2. The Expectations Index is up 3.3 points from two weeks ago. This week’s gain stops a three-month freefall that resulted in the index hitting its lowest point since July 2009.

3. The Current and Investment sub-indices both show increases from two weeks ago (+1.8 and +2.1, respectively). For the Investment Index, this week’s increase halts a two month decline that left the index at its lowest since October 2011.

- The Current Index and Investment Index scores are now lower than they were pre-pandemic by 16.2 points and 15.1 points, respectively. The Current index sits around 8 points lower than both its pandemic and 20-year historical averages, while the Investment index is around 9 points lower than these respective averages.

4. The Jobs sub-index had the biggest increase of the sub-indices, up 3.6 points from two weeks ago. It continues to remain relatively strong, exceeding both its pandemic and historical averages by 7.0 and 7.6 points, respectively. The index now sits just 2.8 points below its pre-pandemic reading.

- The proportion of Americans who say they are more confident in their job security now compared to six months ago is at 44%, up 2 points and reversing losses from two weeks ago.

- The proportion of Americans reporting they, a family member, or a personal acquaintance lost their job in the past six months due to economic conditions is at 20%, down 4 points from two weeks ago.

- In addition, 35% say it’s at least somewhat likely that they, a family member, or a personal acquaintance will lose their job in the next six months due to economic conditions, down 6 points from two weeks ago.

5. A majority of Americans continue to expect inflation to rise over the next year, along with mortgage interest rates, their monthly expenses, and their taxes. In addition, four in ten now believe the number of unemployed people in the country will go up, marking the highest this measure has been since tracking started in December 2021.

- Wave-over-wave changes were not as significant this week.

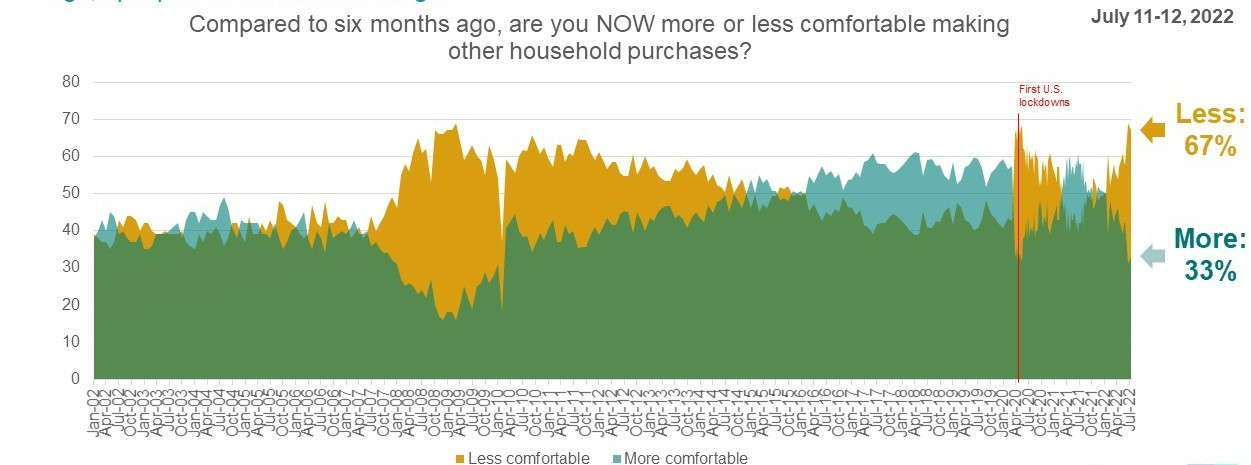

6. Comfort with making major purchases relative to six months ago sees a slight uptick, but just one in three are currently comfortable making both major and other household purchases.

- 33% say they are more comfortable making major household purchases compared to six months up 3 points from two weeks ago.

- 33% say they are more comfortable making other household purchases compared to six months ago, up 2 points from two weeks ago.

Questions

The data used for the Consumer Confidence index and sub-indices is based on the following questions:

1. Now, thinking about our economic situation, how would you describe the current economic situation in the US? Is it… very good, somewhat good, somewhat bad or very bad?

2. Rate the current state of the economy in your local area using a scale from 1 to 7, where 7 means a very strong economy today and 1 means a very weak economy.

3. Looking ahead six months from now, do you expect the economy in your local area to be much stronger, somewhat stronger, about the same, somewhat weaker, or much weaker than it is now?

4. Rate your current financial situation, using a scale from 1 to 7, where 7 means your personal financial situation is very strong today and 1 means it is very weak

5. Looking ahead six months from now, do you expect your personal financial situation to be much stronger, somewhat stronger, about the same, somewhat weaker, or much weaker than it is now?

6. Compared to 6 months ago, are you NOW more or less comfortable making a major purchase, like a home or car?

7. Compared to 6 months ago, are you NOW more or less comfortable making other household purchases?

8. Compared to 6 months ago, are you NOW more or less confident about job security for yourself, your family and other people you know personally?

9. Compared to 6 months ago, are you NOW more or less confident of your ability to invest in the future, including your ability to save money for your retirement or your children’s education?

10. Thinking of the last 6 months, have you, someone in your family or someone else you know personally lost their job as a result of economic conditions?

11. Now look ahead at the next six months. How likely is it that you, someone in your family or someone else you know personally will lose their job in the next six months as a result of economic conditions?

Additional question:

1. Over the next year, do you think each of the following will go up, go down, or stay about the same?

- The rate of inflation

- Mortgage interest rates

- The amount you pay on monthly bills and other regular expenses

- The taxes you pay

- The number of unemployed people in this country

- Your household income (e.g. wages, pensions, benefits, investment, etc.)

- The total amount of your debt (e.g., mortgage, home equity/ auto/ student/ pers. loans, credit card debt, etc.)

- Your own standard of living

About the Study

These findings are based on data from an Ipsos survey conducted July 11 – 12, 2022 with a sample of 929 adults aged 18-74 from the continental U.S., Alaska, and Hawaii who were interviewed online in English.

The sample was randomly drawn from Ipsos’ online panel, partner online panel sources, and “river” sampling and does not rely on a population frame in the traditional sense. Ipsos uses fixed sample targets, unique to each study, in drawing a sample. After a sample has been obtained from the Ipsos panel, Ipsos calibrates respondent characteristics to be representative of the U.S. Population using standard procedures such as raking-ratio adjustments. The source of these population targets is U.S. Census 2016 American Community Survey data. The sample drawn for this study reflects fixed sample targets on demographics. Post-hoc weights were made to the population characteristics on gender, age, race/ethnicity, region, and education.

Statistical margins of error are not applicable to online non-probability polls. All sample surveys and polls may be subject to other sources of error, including, but not limited to coverage error and measurement error. Where figures do not sum to 100, this is due to the effects of rounding. The precision of Ipsos online polls is measured using a credibility interval. In this case, the poll has a credibility interval of plus or minus 3.9 percentage points for all respondents. Ipsos calculates a design effect (DEFF) for each study based on the variation of the weights, following the formula of Kish (1965). This study had a credibility interval adjusted for design effect. For n=929, DEFF=1.5 and adjusted Confidence Interval=+/-5.4 percentage points.

Findings from March 2010 to early March 2020 are based on data from Refinitiv /Ipsos’ Primary Consumer Sentiment Index (PCSI) collected in a monthly survey on Ipsos’ Global Advisor online survey platform with the same questions. For the PCSI survey, Ipsos interviews a total of 1,000+ U.S. adults aged 18-74. The Refinitiv/Ipsos Primary Consumer Sentiment Index (PCSI), ongoing since 2010, is a monthly survey of consumer attitudes on the current and future state of local economies, personal finance situations, savings, and confidence to make large investments. The PCSI metrics reported each month consist of a “Primary Index” based on 10 questions available upon request and of several “sub-indices” each based on a subset of these 10 questions. Those sub-indices include a Current Index, an Expectations Index, an Investment Index, and a Jobs Index.

Findings for January 2002- February 2011 are based on data from the RBC CASH Index, a monthly telephone survey of 1,000 U.S. adults aged 18 and older conducted by Ipsos with a margin of error of +/- 3.1 percentage points.

For more information on this news release, please contact:

Chris Jackson

Senior Vice President, US

Public Affairs

+1 202 420 2025

About Ipsos

Ipsos is the world’s third largest Insights and Analytics company, present in 90 markets and employing more than 18,000 people.

Our passionately curious research professionals, analysts and scientists have built unique multi-specialist capabilities that provide true understanding and powerful insights into the actions, opinions and motivations of citizens, consumers, patients, customers or employees. We serve more than 5000 clients across the world with 75 business solutions.

Founded in France in 1975, Ipsos is listed on the Euronext Paris since July 1st, 1999. The company is part of the SBF 120 and the Mid-60 index and is eligible for the Deferred Settlement Service (SRD).

ISIN code FR0000073298, Reuters ISOS.PA, Bloomberg IPS:FP www.ipsos.com