Support for student loan forgiveness varies widely between the American public and those with loans

Washington, DC, June 17, 2022

A new NPR/Ipsos poll among American adults, with an oversample of those with student loan debt, finds that a narrow majority of Americans support forgiving up to $10,000 in federal student loans. However, support declines at higher amounts of loan forgiveness, and adding a household income ceiling, something the Biden administration is reportedly considering, does not impact support.

The poll also explores the attitudes and behaviors of those with student debt in light of the federal student loan pause, a policy in effect since March 2020 where the federal government has allowed those with federal student loans to stop making their payments without accruing additional interest. Among those with student loan debt, the majority report not paying down their loan during the pause. When asked what they have been able to do instead, the most common actions are those that provide a bit of financial breathing room: having an easier time affording essentials (food, rent, gas, etc.), paying down other debt, and putting money into savings.

Detailed findings:

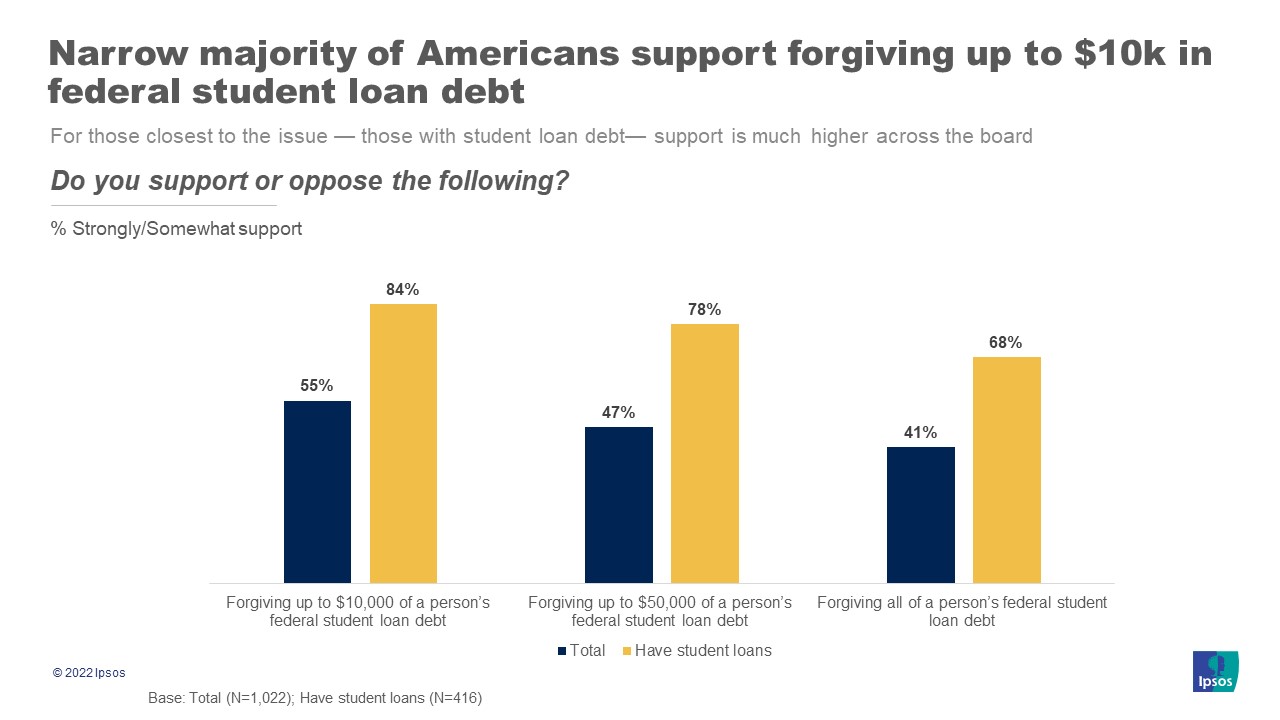

1. A narrow majority of Americans support forgiving up to $10,000 in federal student loans, but support wanes for proposals of a larger amount. A wide majority of those with student loans support forgiveness regardless of the amount.

- A majority (55%) of Americans support forgiving up to $10,000 of a person’s student loan debt.

- Fewer support forgiving up to $50,000 (47%) in student loans and forgiving all student loan debt (41%).

- Roughly four in ten Americans support extending the current federal loan pause without forgiving any loan debt (42%) and ending the loan pause now without forgiving any loan debt (41%).

- A wide majority of those with student loans support each of the three proposals asked about: forgiving $10,000 of student debt (84%), $50,000 of student debt (78%), and all student debt (68%).

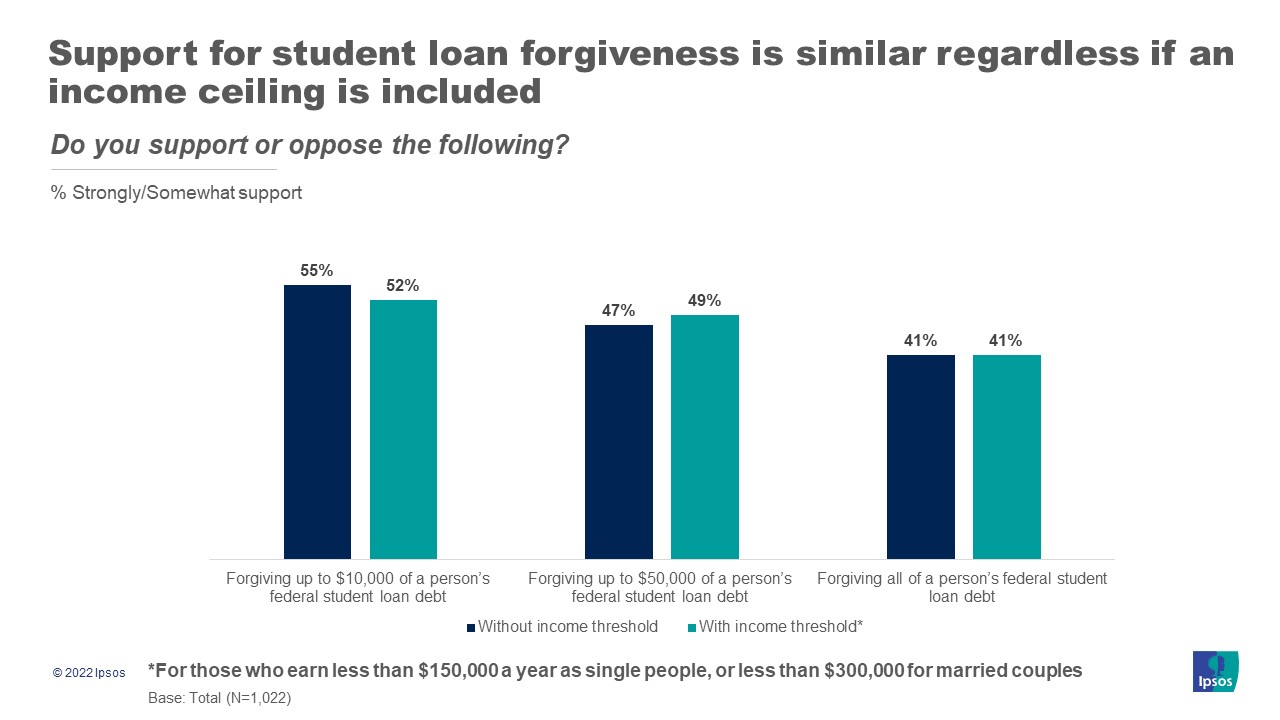

2. Layering in a household income ceiling for loan forgiveness does not change Americans’ support. There is no clear consensus among Americans for the single best path forward.

- Just over half of Americans (52%) support forgiving up to $10,000 in student loans for those who earn less than $150,000 a year as single people, or less than $300,000 for married couples.

- Forty-nine percent support forgiving up to $50,000 in student loans with an income cap, while 41% support forgiving all federal student loans for those who earn less than $150,000 a year as single people, or less than $300,000 for married couples.

- When asked to select the single best path forward, a narrow plurality (25%) say they prefer to end the pause now without any loan forgiveness. Among those with student loan debt, 31% prefer all student loan debt for people that earn less than $150,000 a year, or less than $300,000 a year for married couples be forgiven.

3. Americans and those with student loans alike prefer the government make college cheaper than forgive student loans.

- When asked to choose whether the government should prioritize forgiving some student loan debt, or making college more affordable, 82% of Americans prefer the latter.

- A smaller share, though still a majority (59%), of student loan holders also prefer the government prioritize making college more affordable for future students.

- Nearly two-thirds of Americans (65%) say that if the government does forgive some student loan debt, it should be for graduate and undergraduate debt, as opposed to just undergraduate debt (30%).

4. A majority of Americans with student loan debt say they have not made any payments since the pause began. Instead, most say they have taken this opportunity to catch a financial break.

- Among those with student loans, a majority (57%) say they have not made any payments against their student loans since the pause began.

- When asked what those with student loans have been able to do during the pause that they otherwise would not have, the most frequent behaviors include having an easier time affording essentials like food, rent, and gas (51%), paying down other debt (45%), and putting money into savings (44%).

- Nearly half (47%) of Americans with student loan debt say that the federal student loan pause has improved their mental health.

These are the findings of an Ipsos poll conducted between June 3-5, 2022 on behalf of NPR. For this survey, a sample of 1,022 Americans age 18+ from the continental U.S., Alaska, and Hawaii was interviewed online in English. The poll includes an oversample of student loan holders, for a total of 416 Americans with student loan debt. The poll has a margin of error of plus or minus 3.3 percentage points at the 95% confidence level for all respondents and a margin of error of plus or minus 4.8 percentage points at the 95% confidence level for those with student loan debt.

About the Study

This NPR/Ipsos poll was conducted June 3-5, 2022, by Ipsos using the probability-based KnowledgePanel®. This poll is based on a nationally representative probability sample of 1,022 general population adults age 18 or older. The sample includes 416 people who have student loans.

The margin of sampling error is plus or minus 3.3 percentage points at the 95% confidence level, for results based on the entire sample of adults. The margin of sampling error takes into account the design effect, which was 1.14. For those with student loans, the margin of sampling error is plus or minus 4.8 percentage points at the 95% confidence level. This margin of sampling error takes into account the design effect, which was 1.12 for those with student loans.The margin of sampling error is higher and varies for results based on other sub-samples. In our reporting of the findings, percentage points are rounded off to the nearest whole number. As a result, percentages in a given table column may total slightly higher or lower than 100%. In questions that permit multiple responses, columns may total substantially more than 100%, depending on the number of different responses offered by each respondent.

The survey was conducted using KnowledgePanel, the largest and most well-established online probability-based panel that is representative of the adult US population. Our recruitment process employs a scientifically developed addressed-based sampling methodology using the latest Delivery Sequence File of the USPS – a database with full coverage of all delivery points in the US. Households invited to join the panel are randomly selected from all available households in the U.S. Persons in the sampled households are invited to join and participate in the panel. Those selected who do not already have internet access are provided a tablet and internet connection at no cost to the panel member. Those who join the panel and who are selected to participate in a survey are sent a unique password-protected log-in used to complete surveys online. As a result of our recruitment and sampling methodologies, samples from KnowledgePanel cover all households regardless of their phone or internet status and findings can be reported with a margin of sampling error and projected to the general population.

The data for the total sample were weighted to adjust for gender by age, race/ethnicity, education, Census region, metropolitan status, and household income. The demographic benchmarks came from the 2021 March Supplement of the Current Population Survey (CPS).

- Gender (Male, Female) by Age (18–29, 30–44, 45-59 and 60+)

- Race/Hispanic Ethnicity (White Non-Hispanic, Black Non-Hispanic, Other, Non-Hispanic, Hispanic, 2+ Races, Non-Hispanic)

- Education (Less than High School, High School, Some College, Bachelor or higher)

- Census Region (Northeast, Midwest, South, West)

- Metropolitan status (Metro, non-Metro)

- Household Income (Under $25,000, $25,000-$49,999, $50,000-$74,999, $75,000-$99,999, $100,000-$149,999, $150,000+)

The data for those with student loans were weighted to adjust for gender by age, race/ethnicity, education, Census region, and household income. Benchmarks for respondents with a student loan were developed based on their distribution within the KnowledgePanel general population survey, as national benchmarks for this target population is not available from the US Census.

- Gender (Male, Female) by Age (18–29, 30–44, and 45-60+)

- Race/Hispanic Ethnicity (White/Other Non-Hispanic, Black Non-Hispanic, and Hispanic)

- Education (Less than High School / High School, Some College, Bachelor or higher)

- Census Region (Northeast, Midwest, South, West)

- Household Income (Under $49,999, $50,000-$99,999, $100,000+)

About Ipsos

Ipsos is the world’s third largest Insights and Analytics company, present in 90 markets and employing more than 18,000 people.

Our passionately curious research professionals, analysts and scientists have built unique multi-specialist capabilities that provide true understanding and powerful insights into the actions, opinions and motivations of citizens, consumers, patients, customers or employees. We serve more than 5000 clients across the world with 75 business solutions.

Founded in France in 1975, Ipsos is listed on the Euronext Paris since July 1st, 1999. The company is part of the SBF 120 and the Mid-60 index and is eligible for the Deferred Settlement Service (SRD).

ISIN code FR0000073298, Reuters ISOS.PA, Bloomberg IPS:FP www.ipsos.com