Post-COVID interregnum

For much of the past two years, our outlook on the world was largely conditioned by one looming, all-consuming factor – the coronavirus pandemic. Economic confidence in particular swung according to the vicissitudes of the virus. But our COVID regime appears to be drawing to a close and a new one beginning. In the current context, we are looking at a bumpy road ahead.

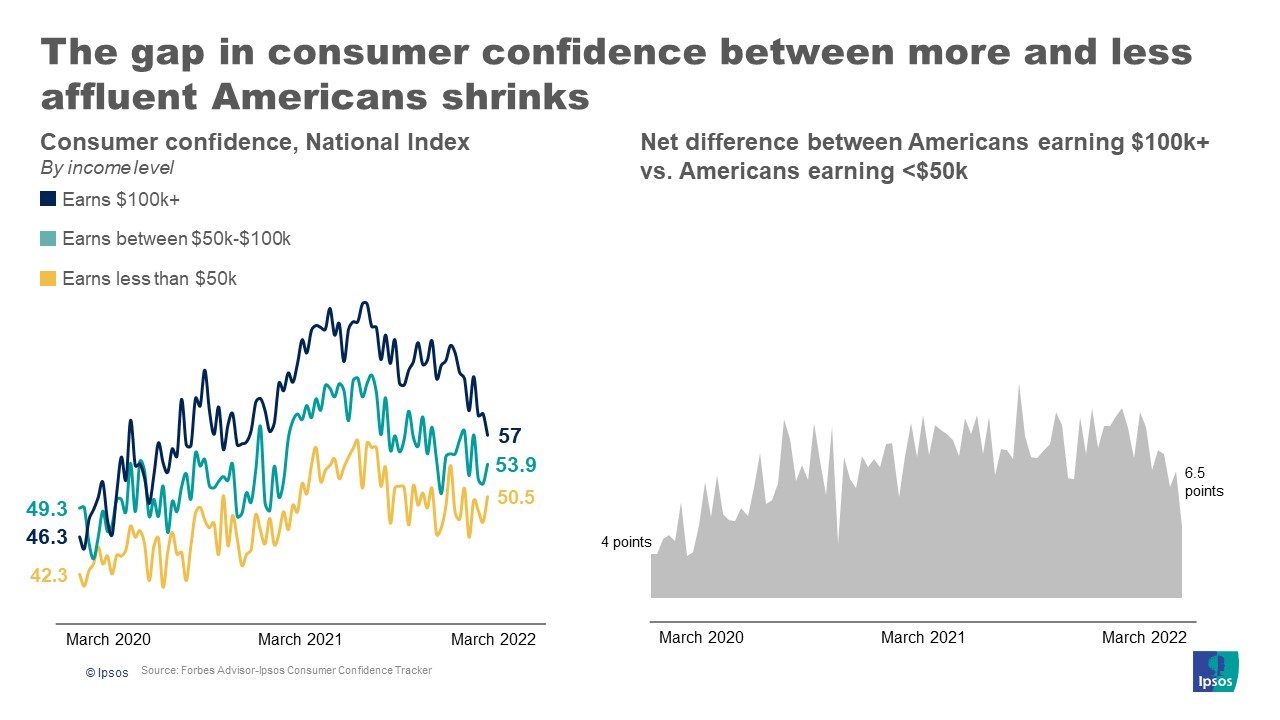

One of the other most salient details from our recent Forbes Advisor Ipsos consumer confidence tracking data is the sudden drop off in optimism among the wealthiest Americans. Throughout the pandemic recovery, they consistently held a sunnier outlook across all four sub-indices we track – views on the current and future state of the economy, investment and jobs. Yet with inflation and other destabilizing forces at play, suddenly even they are feeling warier.

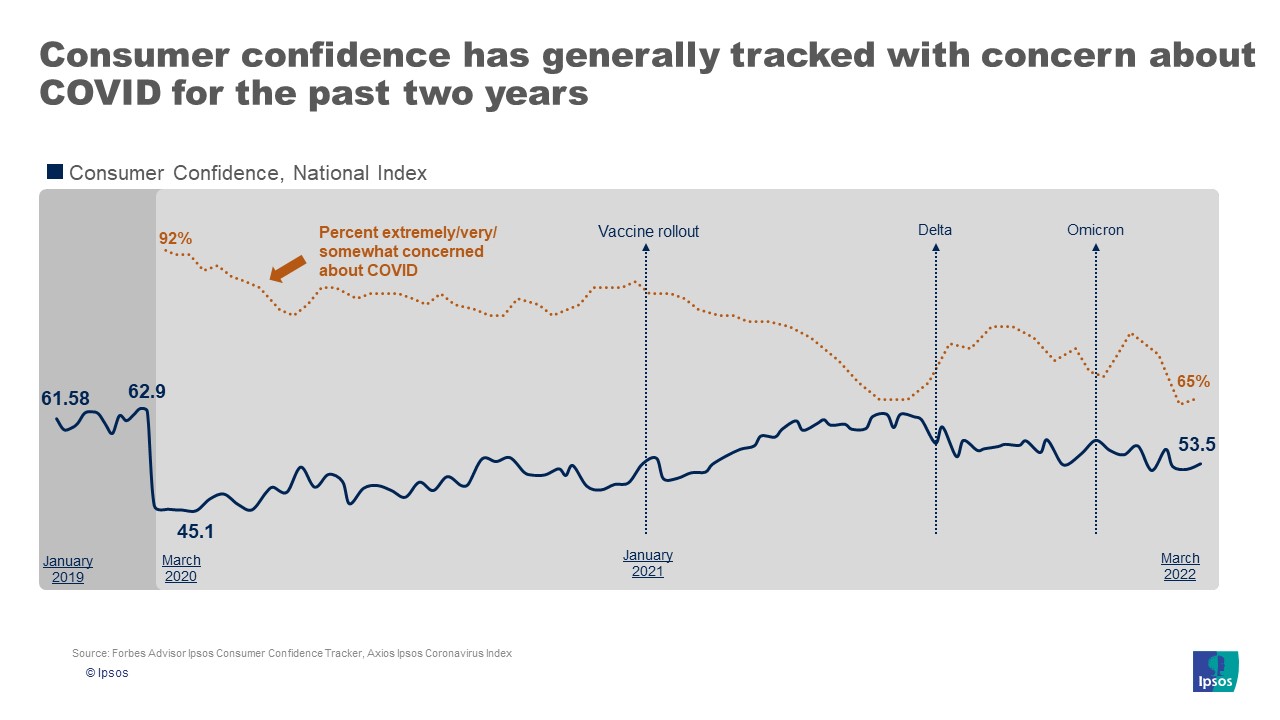

- The COVID Effect. Consumer confidence and concern about COVID had an inverse relationship for much of 2020-2021. The picture is more muddled in 2022. Hopes rose with the advent of vaccines, only to stall out against Delta and Omicron. As concern about COVID dissipates, inflation and the situation in Ukraine are now the most critical concerns, leaving consumer sentiment in something of a holding pattern.

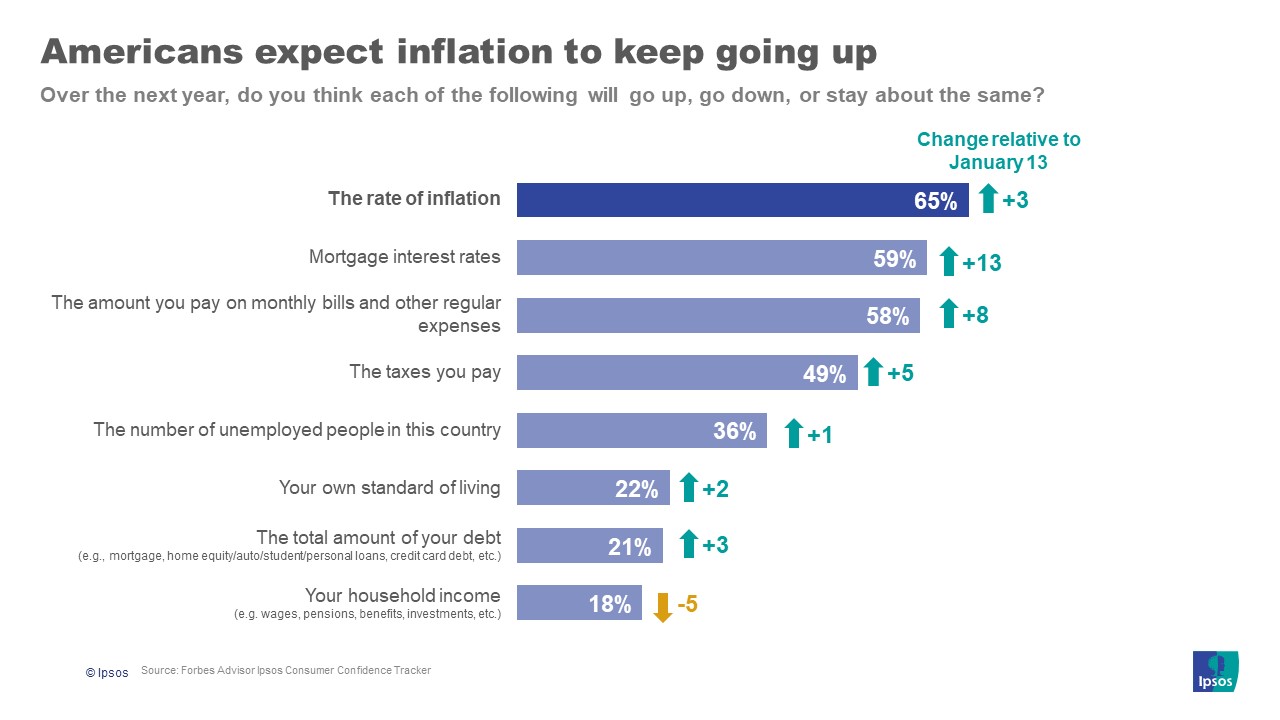

- Buckling down. Most Americans expect inflation to continue to rise into 2022. Bottom line, few expect it to get any easier to pay for daily life, rich or poor. Are we leaving the COVID regime only to enter an inflationary one? Seems so.

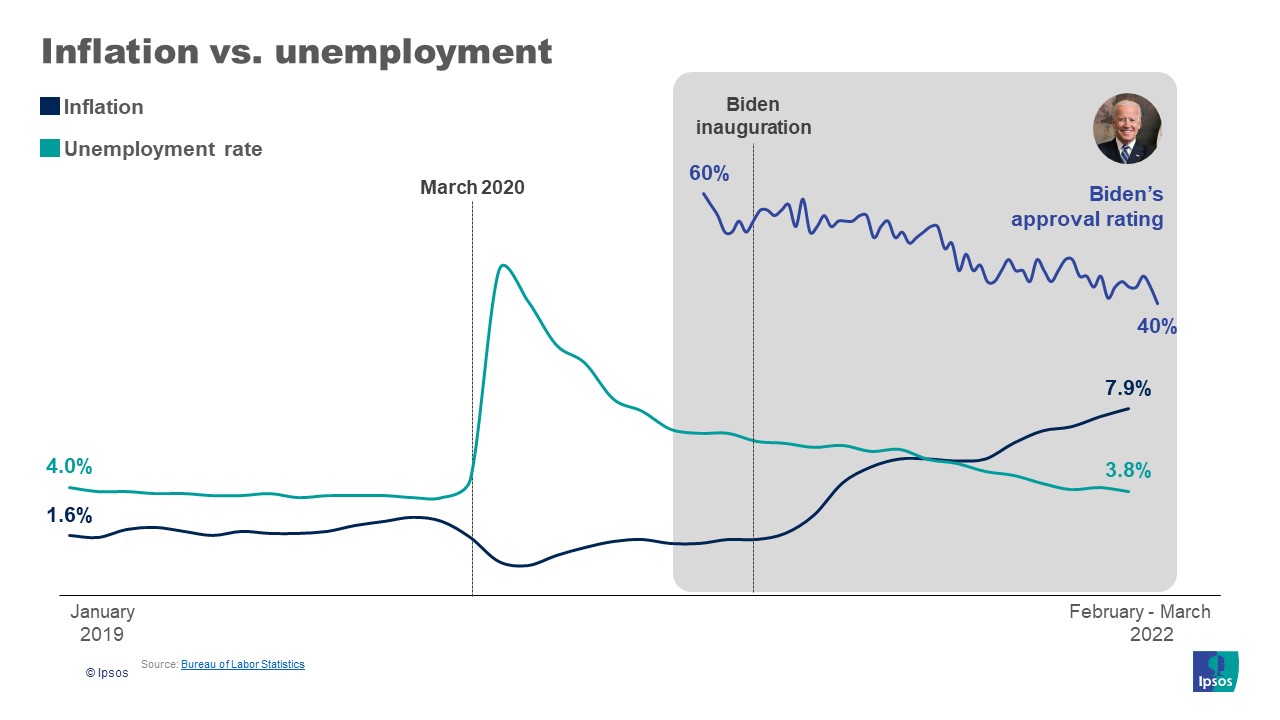

- Inflation rules. Historically, inflation and unemployment have held an inverse relationship. We’ve been seeing this pattern play out over the past couple months. As a sidenote, the implications for Biden have been less than ideal. His approval rating hit its lowest point yet in this week’s core political tracking data. The perennial tension between unemployment and inflation are a challenging mix for policy makers.

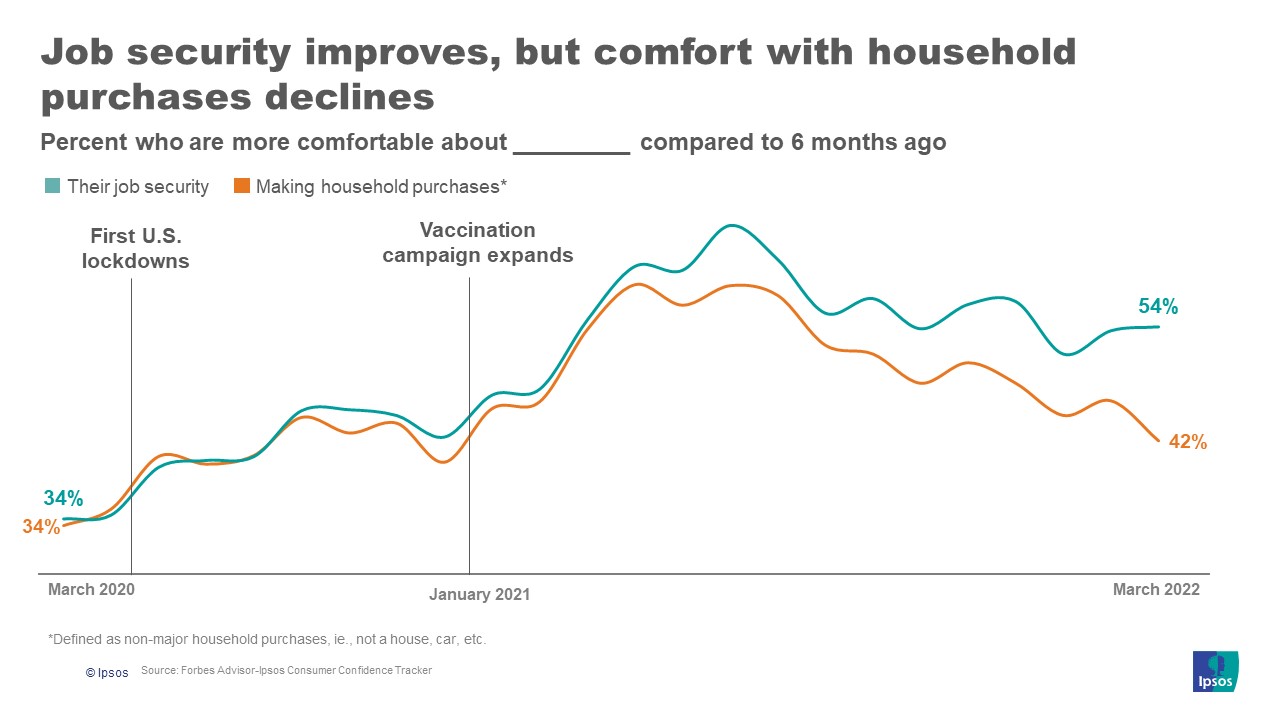

- Inflationary decoupling. Related to this, our economic tracking data shows a distinct decline in comfort with household spending – another proxy for inflation. But at the same time, most Americans still feel their jobs are secure. This decoupling only portends uncertainty.

- The confidence gap. Inflation, the stock market, Ukraine all have Americans worried to varying degrees. Against this, we see the consumer confidence gap between more and less affluent Americans become less extreme. This comes as Americans earning $100k or more show less confidence in their investment prospects and a gloomier outlook on the future. Yet the effects of inflation will likely have more of an impact on those with less to spare.

At this time last year, there was more hope for a clear-cut return to normal once we were no longer living by COVID’s rules. Delta and Omicron changed that calculus. Today, the addition of inflation to the mix makes for an even more volatile situation. Looking ahead, expect sentiment during this transient, not-quite-post-COVID period to be marked by inflation.