Are the 2022 midterms a done deal?

Mid-term season is upon us. All signs point to it going well for the GOP; in fact, our preliminary forecast gives Democrats just a one in ten chance of retaining control of both the Senate and the House. The big question is less “Will the Republicans win,” but, “How much will they win by”?

There is historical precedent for this. Far more often than not, voters tend to reject the party holding the White House in the mid-terms. But other factors – like presidential approval ratings and economic sentiment – influence how meaningful that loss will be.

The current context also sets up significant headwinds for Biden and the Democrats. The pandemic is still with us, inflation is historically high, and Russia just initiated a land war with Ukraine. Fairly or not, voters will hold them to account for these and other issues.

Of course, there are many months to go between now and the day votes are cast. The situation could theoretically change in a way that favors Democrats more, although the chances of this happening are slim.

This is where public opinion lies today.

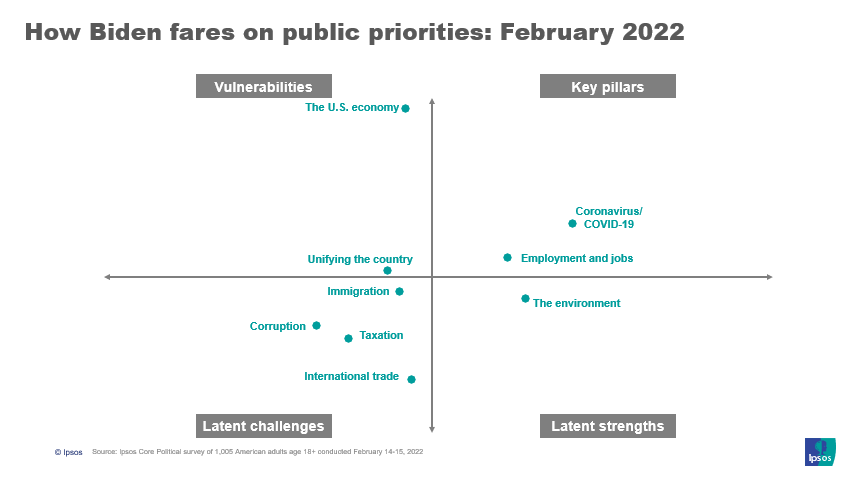

- Strengths and vulnerabilities. Biden’s strengths and weaknesses still look a lot like they did at the outset of his term. COVID management is his bailiwick while he is seen as less effective on the economy. But today, the economy reigns supreme, rendering his advantage on COVID somewhat moot. There is nowhere to pivot. Economic instability on the horizon.

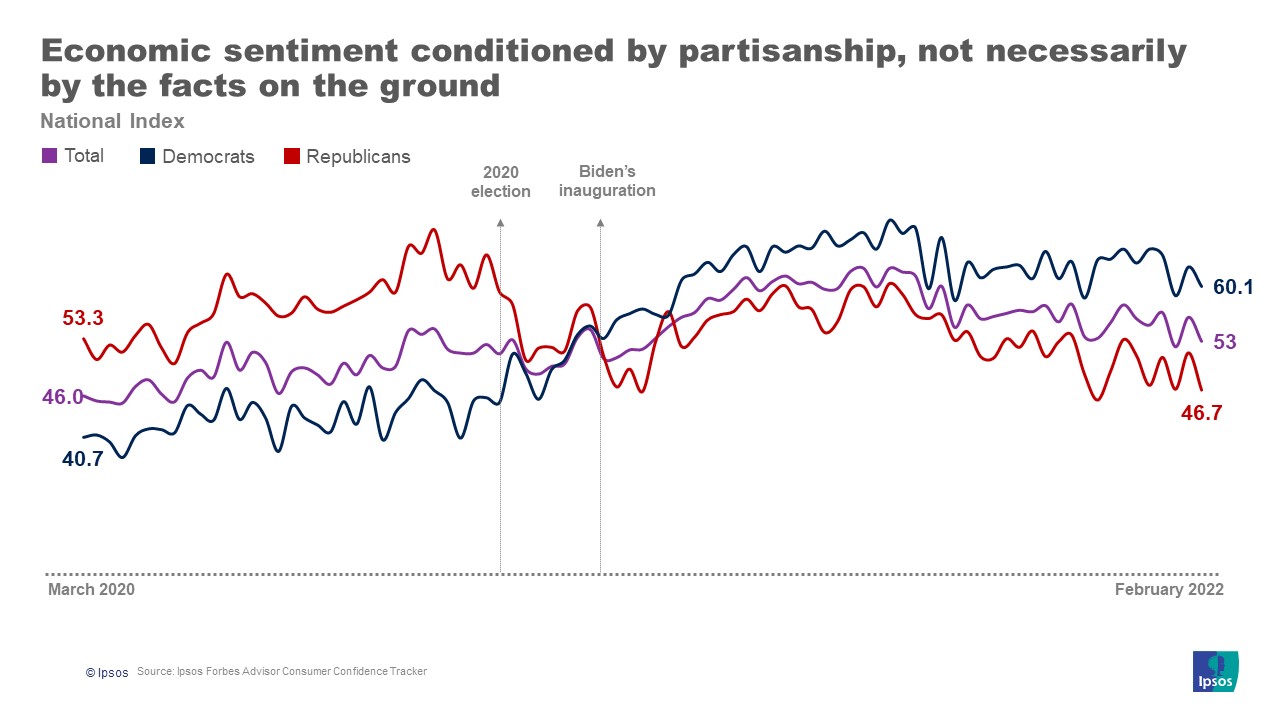

- Partisan economics. The public has good cause to be concerned about the economy – the pandemic remains a drag on businesses, inflation is the highest it has been in 40 years, and the Federal Reserve has signaled an eventual end to low interest rates and easy money. Despite these very real factors, our Forbes Advisor-Ipsos tracking data underlines that economic sentiment is also closely linked to partisanship, not just to material realities. Once again, a tale of two Americas—one red; the other blue.

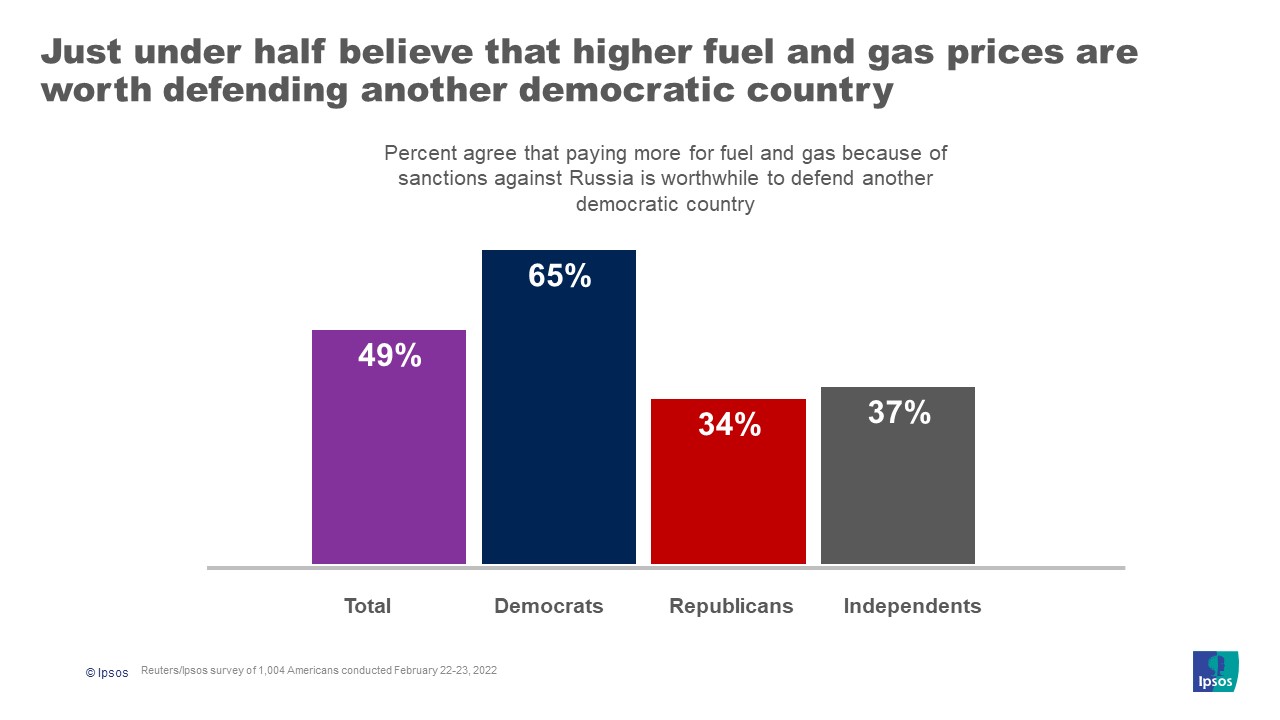

- Ukrainian angst. The conflict in Ukraine adds a new dimension to Americans’ concerns. Uncertainty is never good for business. The price of fuel and gas, already high due to inflation, shot up even higher after sanctions were imposed. There is only marginal consensus on absorbing higher gas prices for Ukraine. Again, red and blue Americans do not see eye-to-eye. For Biden and the Dems, this foreign conflict will likely have negative domestic consequences – no rally around the flag effect here.

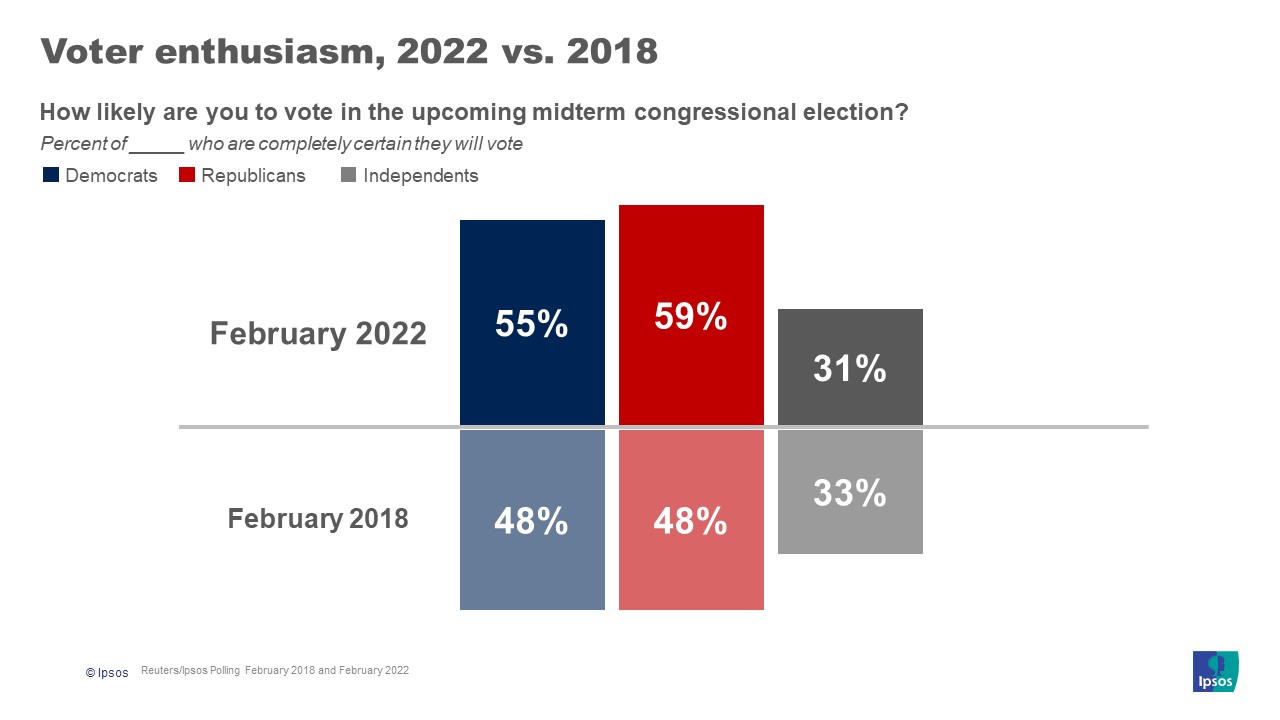

- Year of the GOP. Who actually shows up to vote is an important piece of the midterm puzzle. Remember that midterm turnout is generally low. But there are no prizes for not showing up. Our polling data – and early primary turnout numbers – suggest that Republicans are more fired up to vote than Democrats. Again, 2022 will be a red year.

- Average losses. Since 1946, the party in power has lost an average of 4 seats in the Senate and 26 seats in the House of Representatives. Redistricting may recalibrate the traditional electoral map, but all Republicans need is 5 seats in the House and 1 in the Senate for majority control of Congress. The law of historical averages would suggest that the outcome is a done deal. The consequences? No chance for the Dems to advance their legislative agenda.

Polling is a snapshot of public sentiment at a specific moment in time, so it’s important to remember that these points are always retroactive and not a guaranteed predictor of what’s to come. Yet unless the situation changes drastically, all signs point to Republicans gaining a meaningful advantage in Congress.

That’s because nothing is certain at the moment – COVID, the economy, or the foreign stage. Such fuzziness is a bad thing for the Democrats and the president. Like all parties in power, they arrive at the midterms at a disadvantage. But the broader environment makes that reality even more challenging.