Oncology: the disease, dynamics & challenges of market research

In such a fast-paced and multi-faceted environment, what are the key considerations for those working in oncology today?

In such a fast-paced and multi-faceted environment, what are the key considerations for those working in oncology today?

In an update of our 2018 edition of this paper, we combine new data from Ipsos’ Global Oncology Monitor with our current therapy expertise and market insight to outline the considerations and challenges for professionals who market, or conduct marketing research for, oncology products.

The fundamentals of the disease and the complexity of its treatment are discussed, as well as specific developments such as biomarker testing, the ongoing rise of immunotherapy and biosimilars and, of course, more recent impacts from the global COVID-19 pandemic.

Find more about our Healthcare offer

Introduction

According to the World Health Organization, nearly 10 million people died from cancer in 2020, with deaths most commonly attributed to lung, colorectal and liver cancer. This figure looks set to rise, with one model predicting the number of cancer deaths in 2040 to be around 16 million, and the incidence of new cancer cases rising from about 19 million worldwide in 2020 to about 29 million by 2040. Whether we experience the disease personally or know someone who has, each and every one of us will likely be impacted by cancer in some way during our lifetime.

The earliest documented case of cancer is over 3,000 years old and yet, in some ways, it remains a mystery today. While we have learned a great deal about the causes and effective treatments, those who work in the oncology market are constantly faced with the challenges of this ever-changing disease.

Cancer is complex because it is one term that encompasses many different malignant diseases. There is no one cause of cancer, nor is there a single treatment protocol. The biology of cancer is also very complex, leading to an abundance of treatment approaches. Incidence and prevalence rates differ globally, and treatment of the disease is managed by numerous physician specialties. In addition to these challenges, the continually evolving nature of our understanding of the disease and treatment approaches makes it difficult to remain current. Excluding any biosimilars or generics, there were 121 new approvals of cancer drugs across the US, EU5 and Japan in 2020 (these include label extensions for existing agents).

With this increase in cancer drug development and availability comes an increase in both cost and revenue from these products; the cumulative annual revenue generated from cancer drugs developed by 10 pharma companies with the highest revenue increased from $52 billion in 2010 to £103.5 billion in 2019, highlighting the economic scale and importance of this ever-growing field.

In recent years, we have also seen the advent in cancer treatment of immunotherapy, a revolutionary treatment approach that uses the body’s own immune system to fight disease. A significant proportion of new agents have been approved alongside new companion diagnostics tests, and we now see the rise of elements such as tumour agnostic biomarkers and liquid biopsies. Other novel approaches under development, including therapeutic vaccines and gene editing, hold the promise of potentially revolutionizing treatment in the future, if they prove to be effective.

This paper provides an introduction to the complex market of oncology and highlights some of its distinct challenges. Its aim is to inform and equip professionals who market, or conduct marketing research, for oncology products globally.

Complexity of the Disease Area

Cancer and its Causes

Simply put, cancer is the uncontrolled growth of poorly differentiated (nonfunctioning) cells. These cells’ unchecked proliferation causes them to crowd out normal functioning cells, eventually leading to cell death.

The proximate cause of cancer (i.e. the event which is closest to, or immediately responsible for causing) is mutations of genes that keep normal cellular growth regulated. Mutations in key regulatory genes alter the behaviour of cells and can potentially lead to the unregulated growth seen in cancer. Proto-oncogenes are genes that, when mutated, may lead to unlimited cellular proliferation. It appears that a number of mutations are likely involved in cancer, and tumours rarely rely on one mutation alone; it is the accumulation of such mutations that lead to the occurrence of cancer.

The fact that cancer is caused by mutations has many implications for its treatment. However, mutations do not occur in a vacuum. Many factors can be involved in the mutation of genes, including:

- Lifestyle choices: Smoking and alcohol are chemical teratogens (chemicals that cause mutations), while a diet high in fat and a sedentary lifestyle are thought to increase body fat, which stores teratogenic chemicals.

- Environmental factors: Radiation causes mutation directly by altering DNA; chemicals work to disrupt transcription and translation processes or act as endocrine disrupters that can stimulate cell growth.

- Infectious agents: Some viruses act by inserting their own DNA into the nucleus, which can lead to oncogenic mutations. Furthermore, some bacterial infections may contribute to the proliferation of cancer cells.

Our bodies constantly fight off cancer. If damaged DNA is detected, our DNA repair mechanism typically restores the cell’s genetic material. If this mechanism fails and poorly differentiated cells are detected, our immune system typically destroys the damaged cells before they can multiply and spread. However, increasing age has an impact on these processes.

Some people also inherit genes that predispose them to developing cancer; cancer is not inevitable, but it is much more likely to develop in people with so-called cancer genes than among the general population.

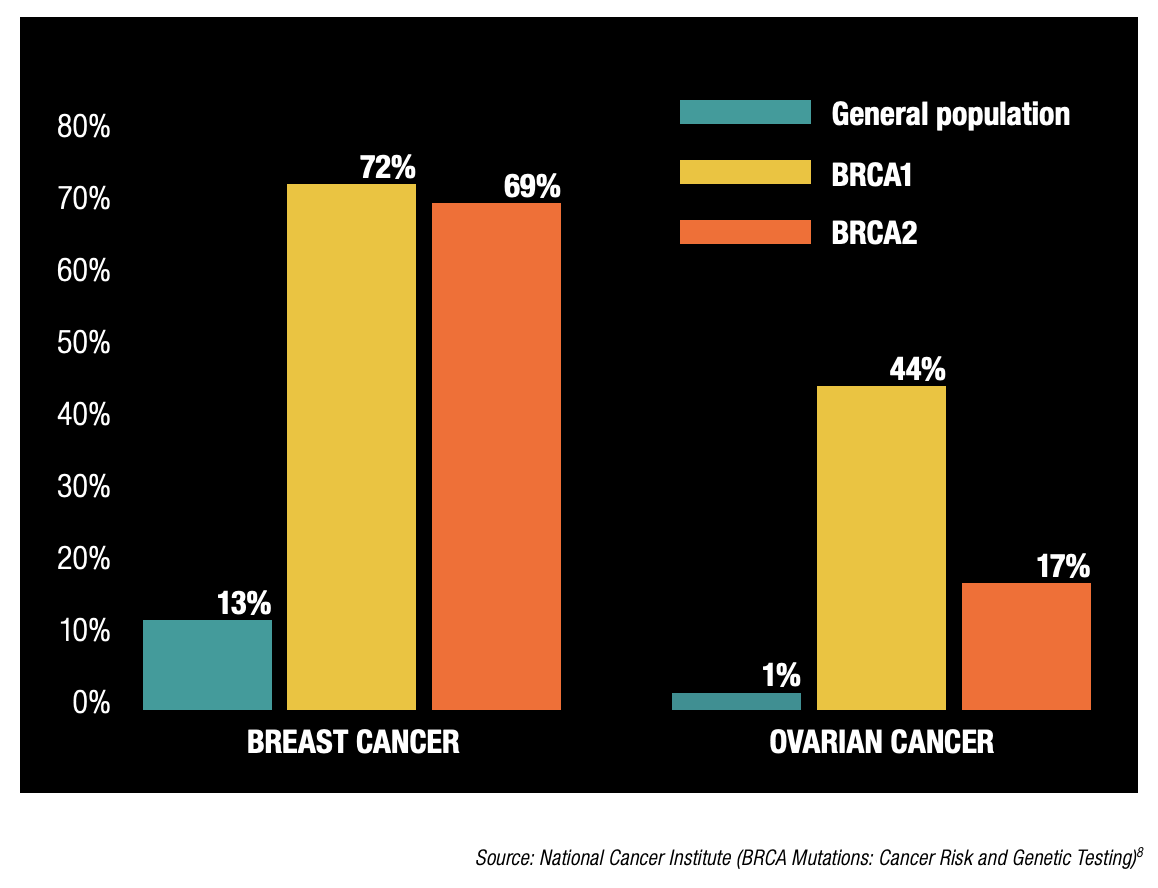

About 5-10% of cancers are thought to be hereditary. Hereditary cancer tends to occur at an earlier age than the sporadic form of the same cancer, so screening is recommended. For example, mutations to tumour suppressor genes BRCA1 and BRCA2 predispose individuals who carry them to breast and ovarian cancers, in addition to a higher risk of other tumours as well.

Figure 1: Incidence of Cancer in General Female Population with BRCA Mutation vs. General Population

Figure 1: Incidence of Cancer in General Female Population with BRCA Mutation vs. General Population

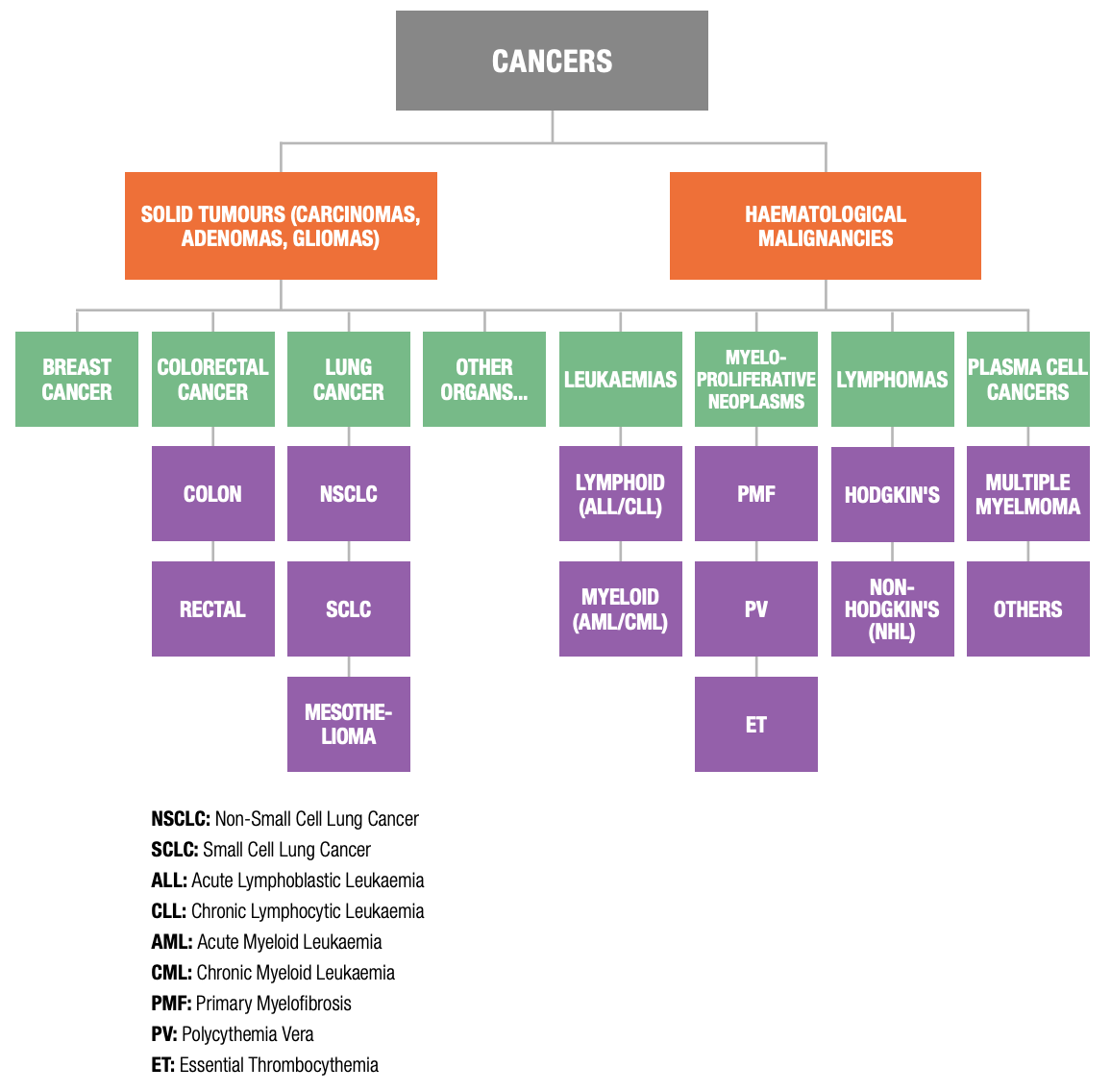

Cancer – One Disease or Many?

Each type of cancer is unique – a disease within itself, with its own causes, symptoms, and methods of treatment. Leukaemias, lymphomas and myelomas are considered haematologic malignancies, while tumours affecting a specific organ are considered solid tumours. As with all groups of disease, some types of cancer are more common than others.

Figure 2: Tumour Types and Sub-Types

Figure 2: Tumour Types and Sub-Types

Classifying cancer becomes more comprehensive when linking it to the specific organ or system in the human body affected. The following table shows this classification.

Figure 3: Cancer Classifications

Figure 3: Cancer Classifications

Once the cancer type is identified, there is still a need to understand the histology or cell type of the disease. This process allows pathologists and physicians to understand which cells are being primarily impacted within the cancer.

For example, in NSCLC alone, there are different histological categories, the most common ones being:

- Squamous cell

- Adenocarcinoma

- Large Cell

Adenocarcinoma and Large Cell are often grouped together and referred to as “nonsquamous” NSCLC. There are also several other rarer subtypes of NSCLC, such as pleomorphic, carcinoid tumour, adenosquamous, and salivary gland-type carcinoma.

NSCLC subtypes are further segmented by predictive biomarkers (which are discussed in a later section). All of this will ultimately inform the oncologist’s treatment approach and selection for the individual NSCLC patient.

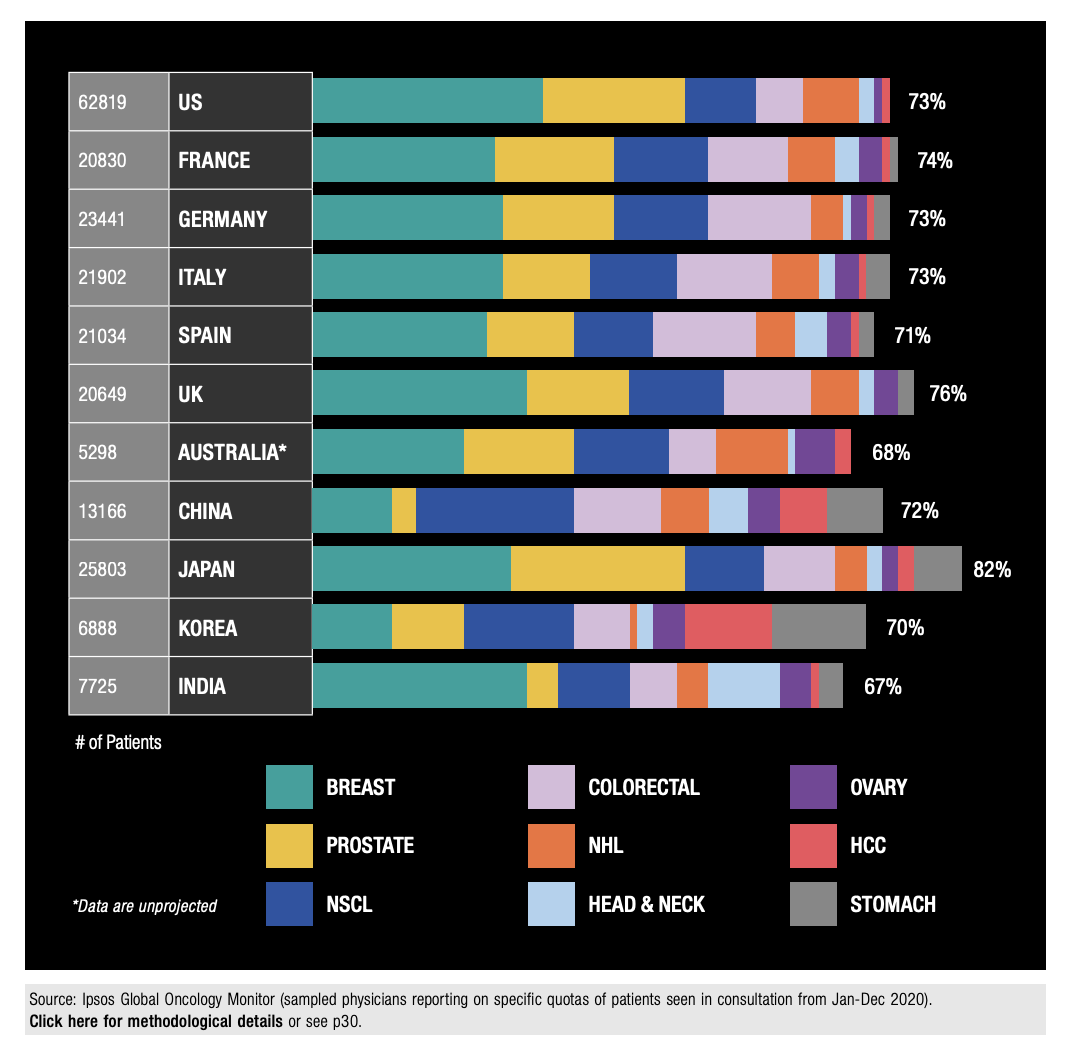

Cancer Around the Globe

As cancer and treatment approaches vary significantly from country to country, it is important to understand not only the biology of each of the diseases but also the global differences.

It is well documented that cancer incidence varies globally. For example, the incidence of prostate cancer is lower in certain Asian countries compared to the US and Europe, while stomach cancer is more prevalent in Asia, particularly East Asia. These differences stem from a multitude of factors including lifestyle, average age of the population and overall economic status of the region.

The Western diet, high in fat and refined sugar but lower in fibre, has been linked to the increased risk of several cancers, including prostate, colorectal and breast, three of the top drug-treated cancers in the US and Western Europe according to Ipsos Global Oncology Monitor data. Meanwhile, NSCLC shows the highest drug-treated prevalence in China, likely attributable to pollution and higher smoking incidence, as smoking has the strongest cancer-lifestyle relationship and is responsible for nearly 90% of all lung cancers worldwide. Additional evidence of lifestyle factors is seen in the higher proportion of head and neck cancer in India, driven by use of smokeless tobacco products and the practice of chewing betel quid.

However, it is important to remember that actual drug-treatment rates will not correlate directly with incidence as additional variables come into play, including more prevalent screening, accessibility to medical care, and ability to afford treatment. Such socioeconomic factors often drive greater treatment of cancer in more developed countries.

When viewing cancer globally, it is vital to understand these local and regional considerations that impact incidence, prevalence and ultimately treatment of cancer.

Figure 4: Distribution of Drug-Treated Patients by Select Tumour Types (2020)

Figure 4: Distribution of Drug-Treated Patients by Select Tumour Types (2020)

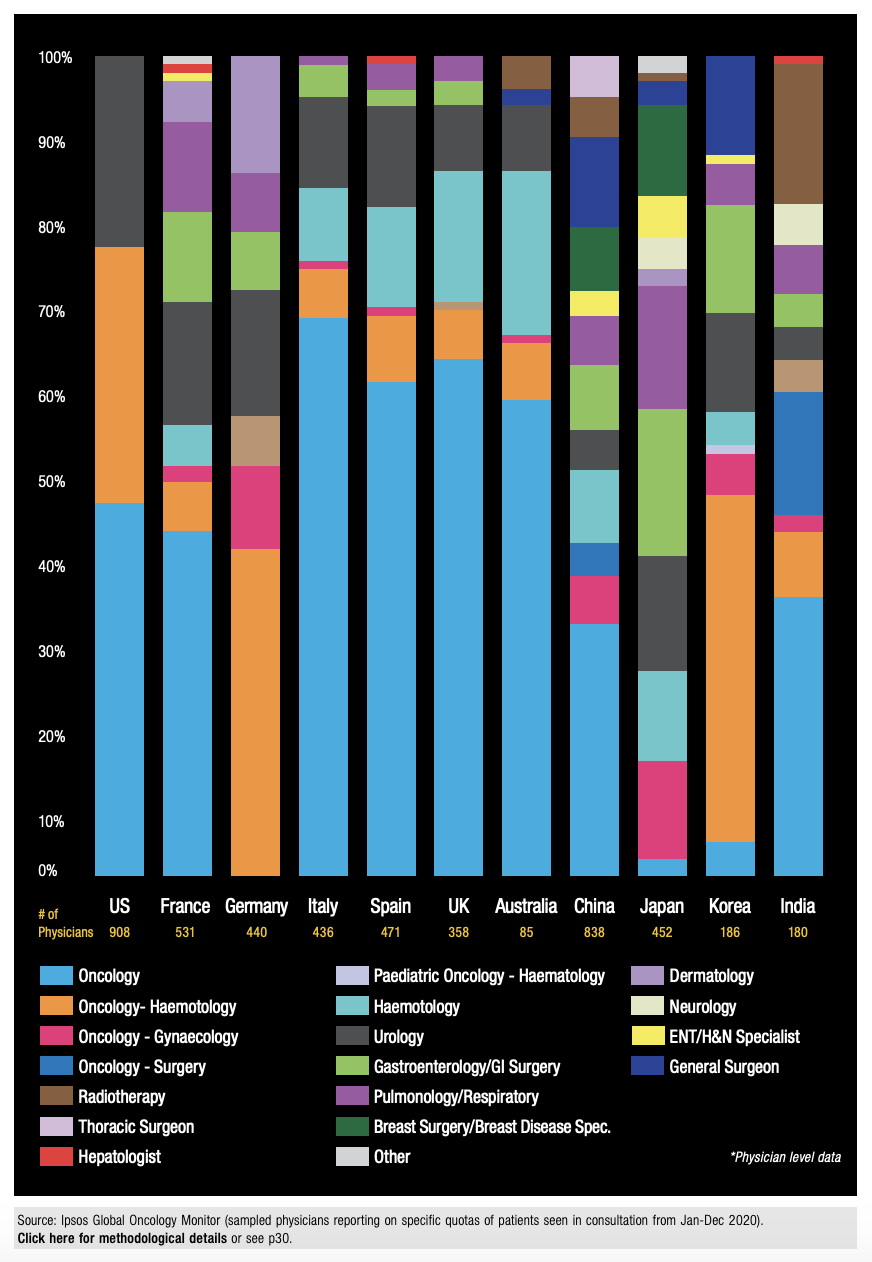

Cancer – One Treater or Many?

When undertaking market research, great care needs to be taken when deciding what audience to survey – we need to think about the sample.

When conducting global research with cancer treaters, many researchers may believe it would be safe to focus only on Medical Oncologists and/or Haematologist/ Oncologists. The reality is, there are multiple physician specialties treating cancer with drug therapy, with variability seen by cancer type as well as by region.

The vast majority of cancer treaters in the US are Oncologists, of which there is a relatively equal distribution between Medical Oncologists and Haematologist/ Oncologists. As of 2020, there were 12,940 practicing oncologists recorded, with 16% of this workforce deemed ‘early career’ oncologists, i.e. 40 years of age and under.

When comparing the US to a market such as Japan, however, there is a stark difference in the physician specialties that treat cancer with systemic therapy. Up until 2007, there was no “oncology” specialty in Japan. Although increasing, the latest figure given by the Japanese Board of Medical Oncology (JSMO) for the number of Oncologists in all of Japan is just 1,461 – lower per capita than the US. As such, the main cancer systemic treaters in Japan are either surgeons or physician specialties that treat a specific area of the body.

According to Ipsos Global Oncology Monitor data, Europe is somewhat of a hybrid of these markets. Medical Oncologists comprise over half of cancer treaters in Italy, Spain and the UK, but in Germany the ‘Oncology-Haematology’ specialty dominates. This difference can be attributed to the fact that in Europe, Medical Oncology is recognized as a distinct specialty in France, Italy, Spain and the UK, but as a mixed specialty with Haematology in Germany. Furthermore, in France and Germany, tumour-specific specialists, such as Gastro-Oncologists (stomach cancer), Pulmo-Oncologists (lung cancer), and Dermato-Oncologists (melanoma), treat with systemic drug therapy, aligning more with the Japanese approach.

Understanding the correct specialties of physician/treater to target and talk to globally can be as much of a challenge as understanding the nuances of cancer treatment. Ipsos conducts a market sizing study that enables us to identify the physician specialties treating cancer in each country.

Figure 5: Systemic Cancer Treating Specialties by Country (2020)

Figure 5: Systemic Cancer Treating Specialties by Country (2020)

Treatment Challenges

Cancer staging – One system or many?

In order to determine the proper treatment for cancer, it is critical to assess the extent of the disease. Several staging systems have been developed to do this.

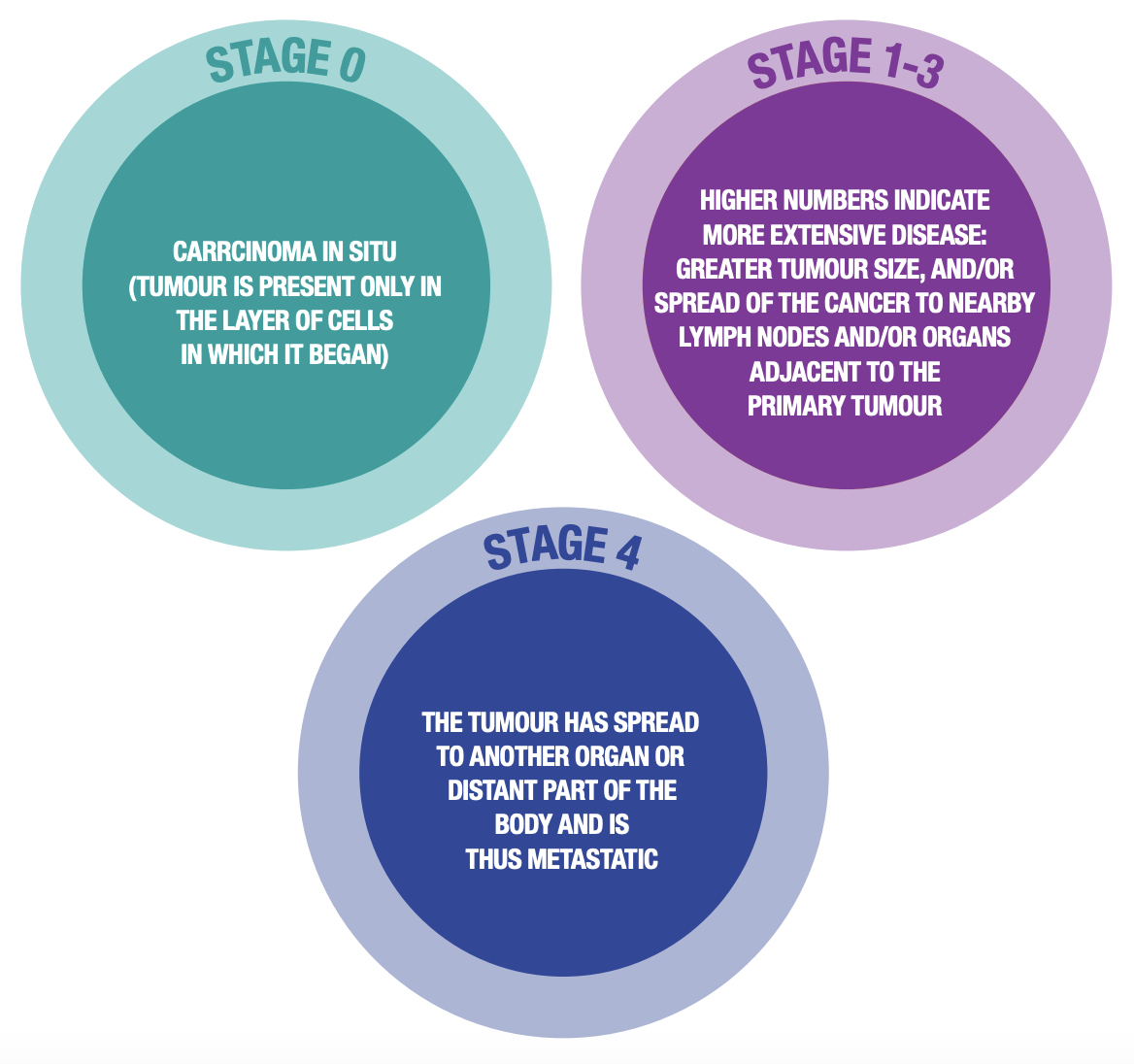

Solid tumours are commonly staged by a Roman numeric system that is related to the extent of disease, with 0 being the least extensive and IV being the most extensive (metastatic) disease. However, gliomas and other CNS diseases are solid tumours that are exceptions to this system.

Figure 6: Roman Numeric Staging System for Solid Tumours

Figure 6: Roman Numeric Staging System for Solid Tumours

For most solid tumours, the TNM staging system is typically used to arrive at the Roman numeral stages. For each cancer type, the exact criteria for assigning these T, N and M values are different, as are the conversions from TNM into their respective Roman numeral stages.

These staging systems continue to evolve over time for any given cancer as our understanding grows. For example, the Cancer Staging System from the American Joint Committee on Cancer (AJCC) is now in its 8th edition.

Figure 7: TNM Staging System for Solid Tumours

Figure 7: TNM Staging System for Solid Tumours

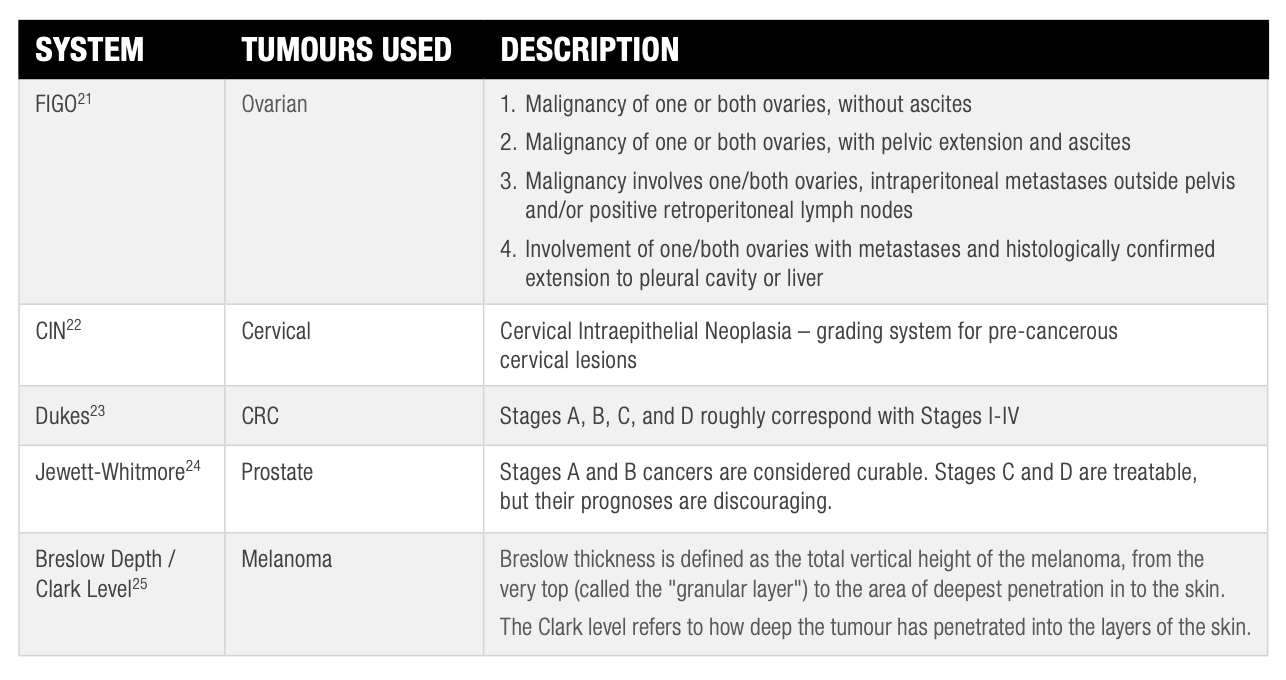

Alternative staging systems to TNM also exist for certain solid cancers, though their usage is generally on the decrease in favour of TNM.

Figure 8: Other Staging Systems for Solid Tumours

Figure 8: Other Staging Systems for Solid Tumours

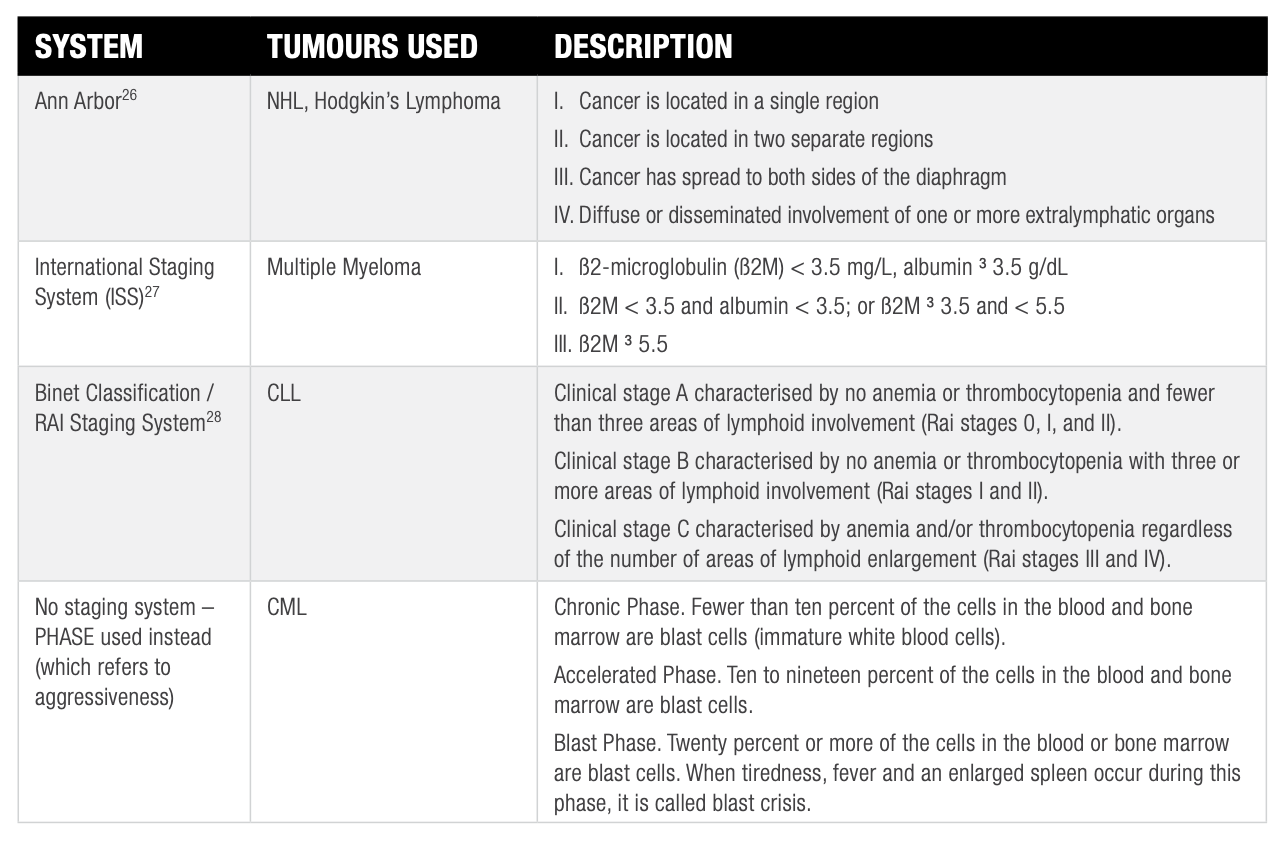

Due to the more diffuse and ‘dimensionless’ nature of these cancers, staging of haematological malignancies is generally very different to staging of solid tumours, and is also specific to each malignancy.

Figure 9: Staging Systems for Haematological Malignancies

Figure 9: Staging Systems for Haematological Malignancies

Some haematological malignancies, such as AML and ALL, are not commonly staged.

Cancer Treatment – Art or Science?

Solid tumours, like breast and lung cancer, begin as small groups of localized malignant cells in the primary organ in which they arose, but ultimately become much more dangerous to the host body by spreading to distant organs. Their relentless drive to replicate means that tumour cells often gain the ability to spread through the human body, in many cases (especially if not treated early enough) resulting in distant metastases. Cancer metastasizes by shedding cells from the primary tumour, which enter the lymphatic system and/or the bloodstream and travel to distant sites where they eventually take hold and replicate.

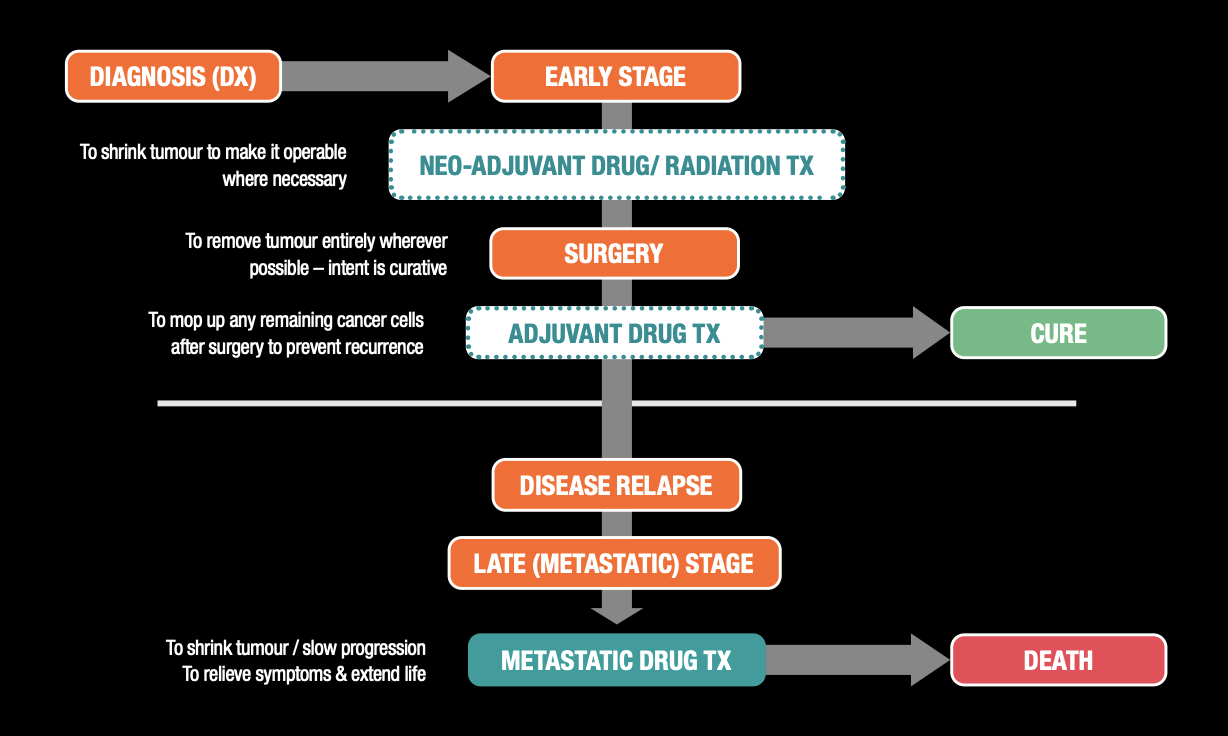

A significant challenge associated with cancer is that treatment is as much an art as it is a science. Even after the cell type, stage and grade (i.e. how aggressive the tumour is) have been determined, other variables such as the patient’s general health, treatment history, preferences and support system, as well as the doctor’s training, come into play to decide the appropriate treatment approach. Initial treatment modality may include surgery, radiation, drug therapy, or some combination of these approaches, with variability seen by tumour type.

Figure 10 shows two different patient diagnoses; one in which the cancer is detected early and another in which the cancer was detected late and had already metastasized (spread).

Figure 10: Solid Tumour Treatment – General Overview

Figure 10: Solid Tumour Treatment – General Overview

When cancer is detected early and the tumour is localized, surgery is generally the standard treatment modality of choice. By resecting the tumour and a margin of tissue surrounding it, a cure is possible. Surgery may also be combined with systemic drug or radiation therapy.

- Neo-adjuvant means that anti-cancer drugs are given before surgery. This aims to decrease the tumour size to make the tumour eligible for resection, improve the outcome, and/or make the resection easier to perform.

- Adjuvant means that anti-cancer drugs are given after surgery. This aims to kill any cancer cells that remain after surgery and prevent a recurrence/return of the cancer.

In some cases, surgery cannot be performed due to the location of the tumour or the patient’s surgical ineligibility due to their general health and/or refusal. In this case, drug and/or radiation therapy may be used instead of surgery.

When cancer is diagnosed late, the treatment objective is to slow its progression in order to extend the patient’s life. Cancer itself does not cause death; death occurs because the cancer cells crowd out the normal functioning cells and damage the organs of the body.

Cancer Treatment – A Plethora of Options

Adding to the complexity of cancer treatment is the fact that more drugs are approved for cancer than any other single disease. With the advent of targeted therapies, some drugs have contributed to changing certain cancer types to more of a chronic condition with significantly longer survival.

Systemic drug therapy for cancer began with cytotoxic drugs and has since expanded to a number of different classes of drugs, as shown in Figure 11.

Figure 11: Systemic Therapy – Cancer Drug Treatment Class Overview

Figure 11: Systemic Therapy – Cancer Drug Treatment Class Overview

The oldest group of anti-cancer drugs is called cytotoxics; these drugs indiscriminately kill cells. Cytotoxic chemotherapy drugs interfere with DNA replication and/or cell division. They do not specifically target cancer cells, but instead rely on the fact that tumours are amongst the most rapidly dividing tissues in the body, hence affecting cancer cells to a larger degree than healthy cells. Because of this indiscriminate mode of action, they often have significant side-effects.

Then there are anti-hormonal therapies which are predominantly used in hormonesensitive breast and prostate cancer. Some breast and prostate cancer cells have receptors on their surfaces that, when stimulated by hormones, result in the cells growing and dividing. Anti-hormonal therapies, sometimes referred to as hormonal agents, act by blocking the surface hormone receptors and preventing the cells from receiving a signal to grow and divide.

Biological/targeted therapies utilize the mechanisms of cancer and the pathways through which the cell signals. They can be divided into two sub-groups:

- mAbs (monoclonal antibodies): mAbs work at the level of the cell surface by blocking receptors that are involved in signalling cancer cells to keep dividing, keep growing and stop dying. They are large molecules and are typically administered by IV infusion.

- Small molecules that target the cell signalling process within the cell: ThBiomarker testing traditionally required a viable tissue sample from the tumour (or metastases), which often necessitated re-biopsies for patients whose cancer had progressed, or for whom insufficient tissue was present in the initial biopsy sample. In the past few years, however, liquid biopsies have arrived on the scene, allowing physicians to send blood (or in some cases, urine) samples from their patients straight to the lab to be analyzed for biomarkers, avoiding the use of a (sometimes invasive) tissue biopsy. In fact, several commercial panels now exist that combine both of these two innovations, allowing for large numbers of genes to be sequenced based on a blood sample only.ese work within the cell by blocking the complex pathways involved in the cell cycle and apoptosis (programmed cell death). These are orally administered, which can also provide a patient convenience benefit.

There are also some mAbs that work not only by blocking the cell surface receptors, but also by delivering cytotoxic or radiological payloads directly to the cancer cells (sparing health cells). These so-called “smart bombs” are a new generation of targeted therapy called “antibody-drug conjugates” (ADC), and a number have now been approved across different tumour types.

Targeted therapies have created much excitement in the field of oncology and have transformed the way in which some cancers are treated.

Biomarkers – Continuing to Transform Treatment Paradigms

Whereas treatment decisions used to rely on a combination of clinical observations, various imaging techniques and general histopathological findings, Oncologists now have a range of biomarker tests at their disposal to make a more informed drug choice in a growing number of tumour types. Notwithstanding the increasing complexity of such testing, this approach ultimately benefits physicians and patients alike: treatments which are likely to lead to better response rates and more prolonged responses can be selected based on molecular characteristics exhibited by the patient’s tumour.

The biomarker testing landscape has undergone multiple major and incremental changes in the past few years, providing Oncologists and other specialties with an increasing toolkit to ensure the right treatments are selected for their patients. Apart from the ever-growing list of biomarkers and their associated companion diagnostics, recent key innovations include the advent of tumour-agnostic biomarkers and liquid biopsies.

Tumour-agnostic biomarkers are part of a key change in philosophy when it comes to how to approach cancer treatment: whereas cancers used to be treated primarily based on the affected organ/cell type (see earlier section in this paper), there is a growing realization that the molecular signature of tumours (the presence or absence of certain genetic changes) is what should be driving treatment choice. For example, a lung cancer with an NTRK fusion can be treated with an TRK inhibitor, much like a breast cancer with the same NTRK fusion can be. On the other hand, lung cancers without NTRK fusions would require a completely different treatment approach. The increased use of these tumour-agnostic biomarkers has been made possible by the continued rise of Next Generation Sequencing – allowing physicians to determine the mutation status of many genes at once - driven in turn by ongoing declines in sequencing costs. A large number of commercial tumour-agnostic panels now exist, and this area continues to change at a rapid pace.

Biosimilars – Making their Mark on the Treatment Landscape

Such is the context at a time when the first ‘generics’ of biologic targeted therapies have now received FDA/EMA approval to treat certain types of cancer, and a growing number of brands are continuing to become available.

As mentioned, targeted therapies such as mAbs are designed to recognize features specific to cancer cells and then target the specific areas of the cell that allow it to grow faster and/or abnormally. Copies of these targeted therapies are known not as generics but as ‘biosimilars’ – because it is impossible to replicate a biologic drug exactly. Manufacturing alone can modify its molecular structure. However, a biosimilar drug will have no clinically meaningful differences from the originator biological medicine in terms of quality, safety and efficacy.

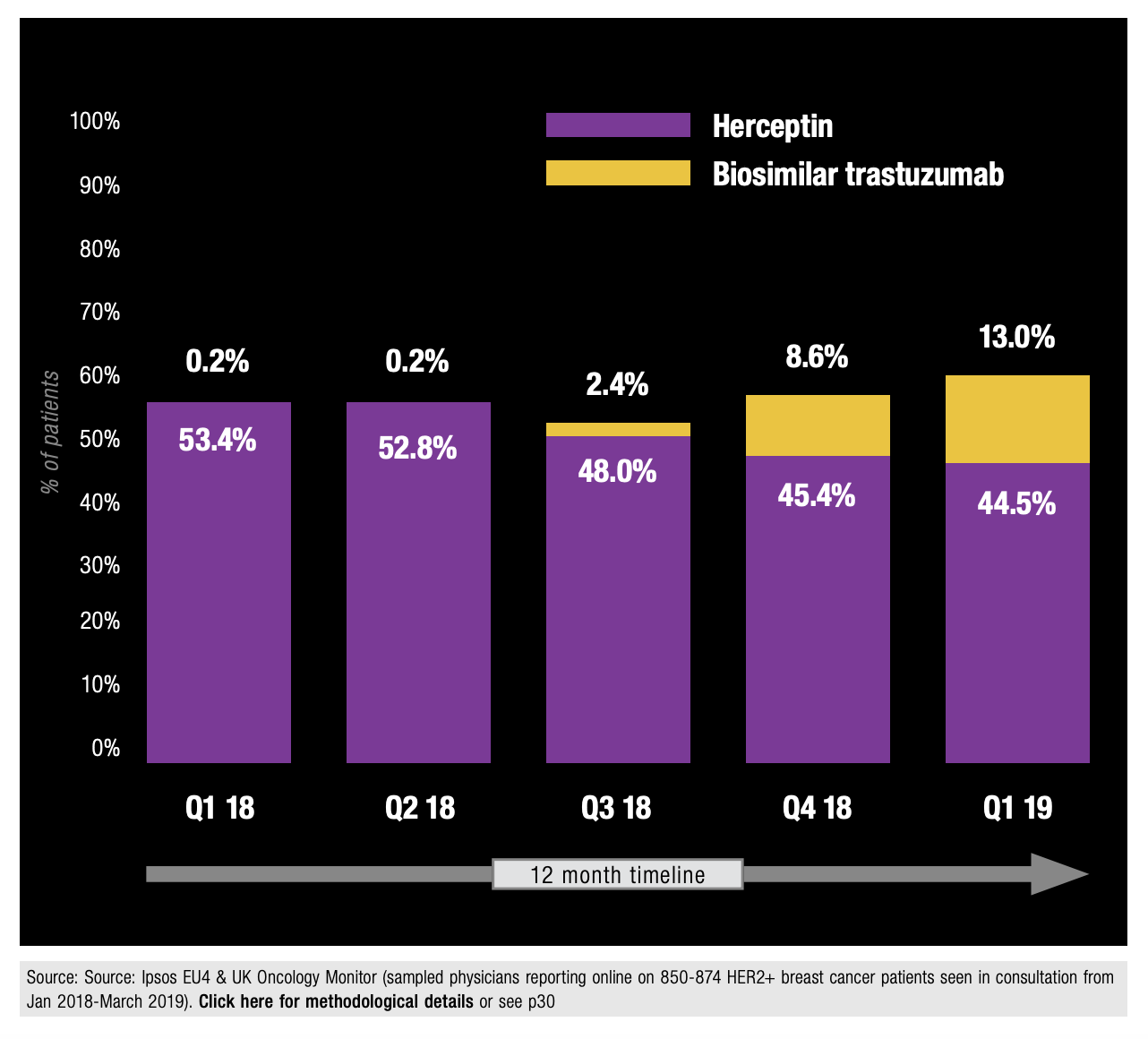

Biosimilars themselves have been around for some time. Despite a slow initial uptake and ongoing debate over the concept of bio-similarity, the last few years have seen widespread use and growing comfort with biosimilars across several gastroenterology, rheumatology and dermatology autoimmune indications, such as rheumatoid arthritis (RA) and ulcerative colitis (UC). Moving back to oncology, 2017 saw the approval of two mAb biosimilars to treat cancer, Truxima® and Rixathon®, both biosimilars of rituximab. In line with all biosimilar drugs, Truxima® was launched at a significantly cheaper cost than the branded version of rituximab, MabThera®. As of early 2021 there were over 15 biosimilar brands available across the rituximab, bevacizumab and trastuzumab molecules to use in oncology, as specified by the European Medicines Agency (EMA)31, with more still in the developmental stage.

Uptake of biosimilars in oncology

Whilst potential barriers may remain to the use of biosimilars, such as lack of evidence, patients’ preference for brands and impossibility of direct replication of originators, Ipsos’ data have depicted a receptive and adaptive marketplace for these more cost-effective options; European HER2+ breast cancer patient data from the Ipsos Oncology Monitor suggested a notable and steady growth of biosimilar trastuzumab usage approximately one year on from availability of the first biosimilar brand:

Figure 12: Patient Share of Biosimilar Trastuzumab vs Originator Usage in HER2+ Breast Cancer in Europe

Figure 12: Patient Share of Biosimilar Trastuzumab vs Originator Usage in HER2+ Breast Cancer in Europe

The Ongoing Rise of Immunotherapy

Immunotherapy – which includes checkpoint inhibitors, therapeutic cancer vaccines, oncolytic viruses, cell-based therapies (e.g. CAR-Ts and TCR-Ts), and cytokines – deserves a section of its own. This treatment approach uses the body’s own immune system to fight diseases; certain Immuno-Oncology (I-O) treatments, such as antiCTLA-4s, anti PD-1s (programmed-death 1), anti PD-L1s (programmed-death ligand 1), and CAR-Ts (chimeric antigen receptor T-cell) have revolutionized cancer therapy in recent years.

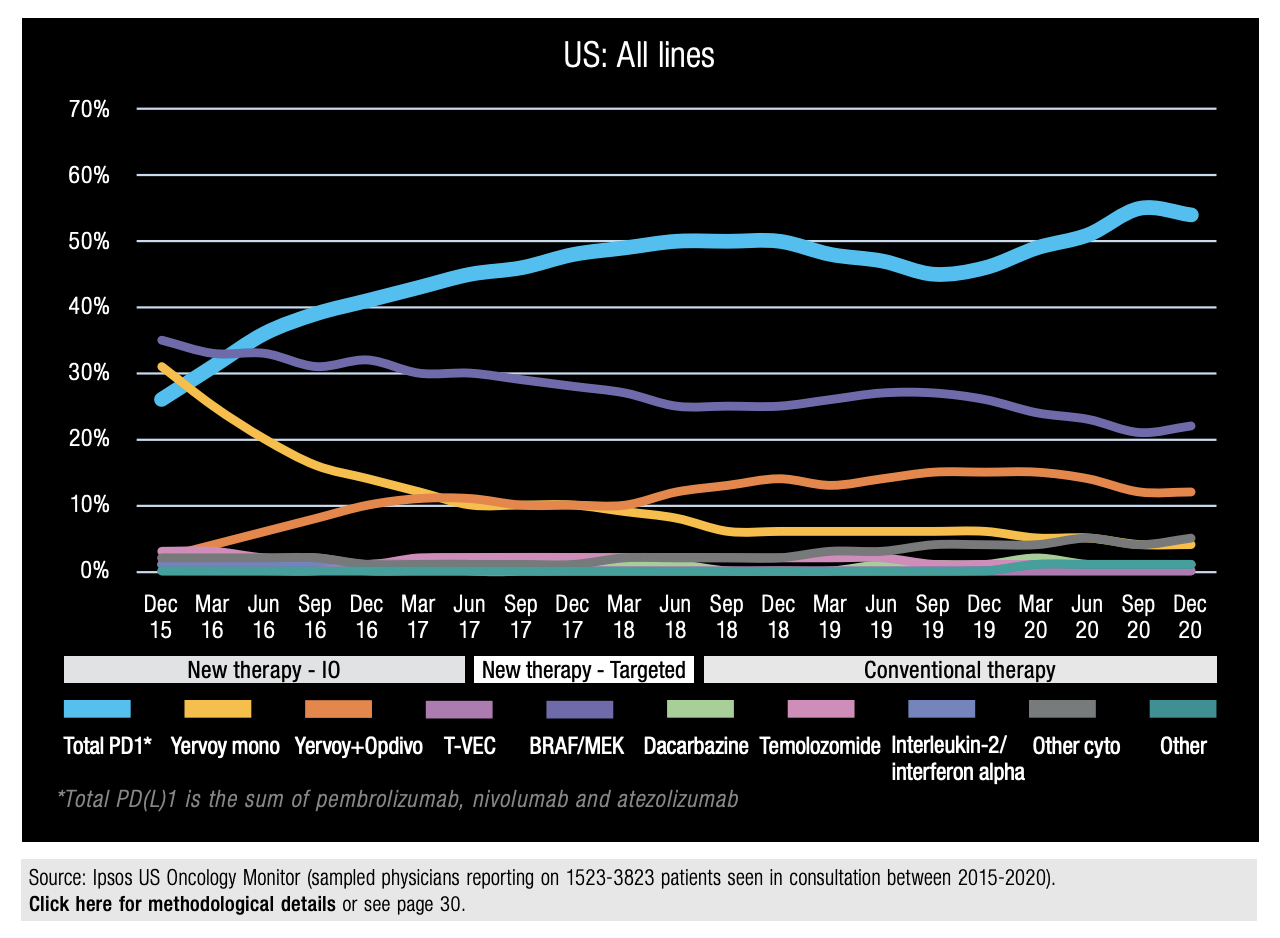

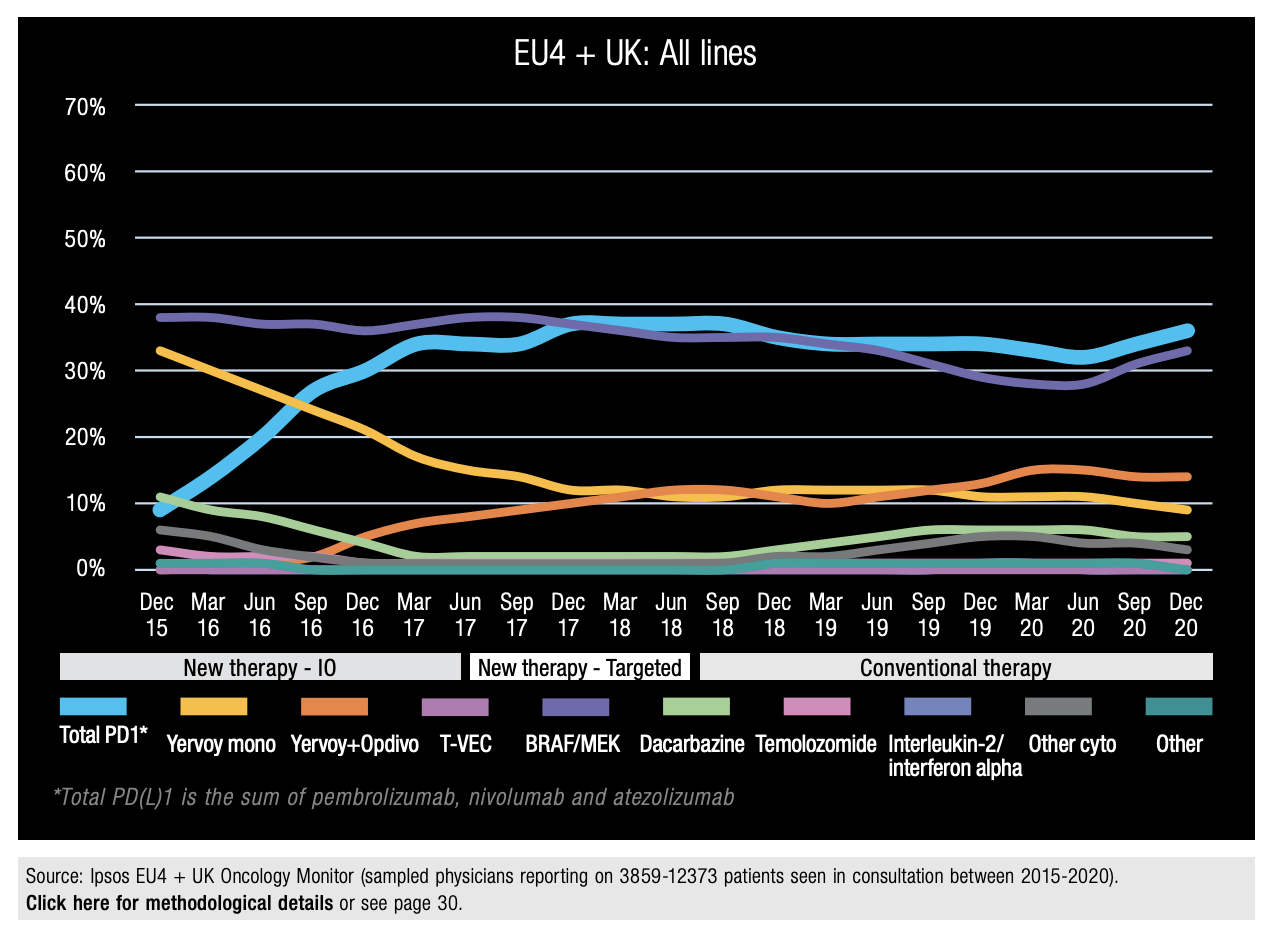

In some indications, there are trends showing that PD-1 inhibitors and PD-L1 inhibitors are now the new standard of care in areas that used to be dominated by treatments such as chemotherapies or other targeted therapies. Figure 13, based on recent data from the Ipsos Global Oncology Monitor, shows the dominance of new therapies versus traditional therapies in the treatment of melanoma by our participating physicians. Chemotherapy using dacarbazine-based regimens used to be the standard of care in the EU5 prior to the arrival of targeted therapies such as the BRAF/MEK inhibitors and I-Os. Now, however, chemotherapies are rarely used for the treatment of advanced melanoma; anti PD-1s/PD-L1s, such as Opdivo®, Keytruda® and Tecentriq®, are now the key treatment in both the US and EU5, alongside BRAF/ MEK targeted therapies.

Figure 13a: Conventional vs. New Therapies in Melanoma (US) (2015 - 2020)

Figure 13a: Conventional vs. New Therapies in Melanoma (US) (2015 - 2020)

Figure 13b: Conventional vs. New Therapies in Melanoma (EU4 + UK) (2015 - 2020)

Figure 13b: Conventional vs. New Therapies in Melanoma (EU4 + UK) (2015 - 2020)

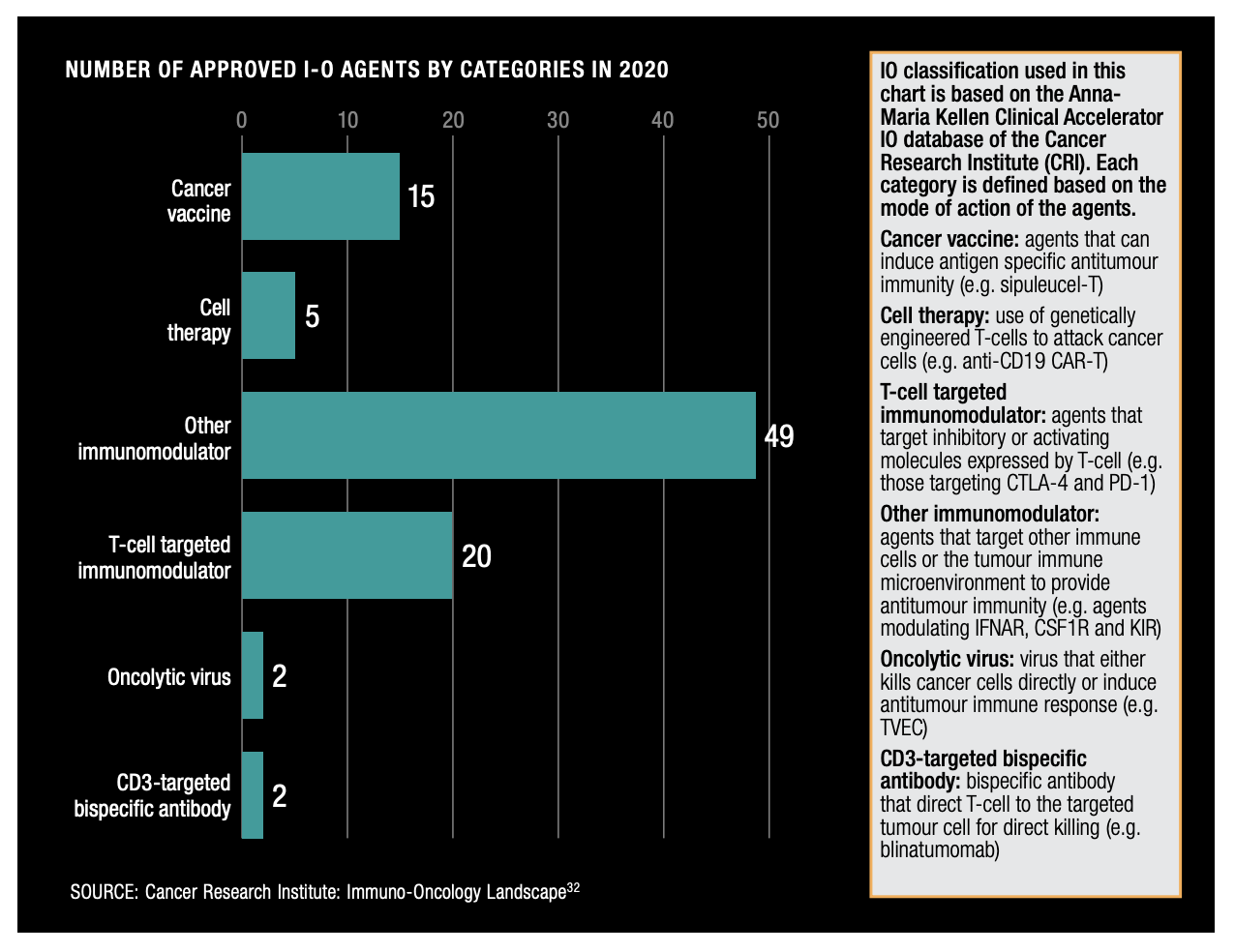

As of 2020, there were 93 active I-O agents that had been approved and development appears to be far from slowing down. A further 4,627 agents are recorded in the developmental pipeline, from preclinical stage, up to phase III trial setting. The global cancer immunotherapy market is expected to grow at a CAGR of 13.8% from 2018 to 2024 to reach USD 152.83 billion by 2024.

Figure 14: Number of Approved I-O Agents by Categories in 2020

Figure 14: Number of Approved I-O Agents by Categories in 2020

Given the advent of the COVID-19 pandemic and the subsequent vaccination programme, we feel a specific acknowledgment must be made of mRNA vaccines and their use in the fight against cancer. mRNA vaccines ‘teach’ our cells to produce and recognize certain proteins that appear on the surface of the cancer tumour, thereby triggering an immune response to the tumour itself. Taking it a step further, personalized mRNA cancer vaccines use tumour tissue from an individual patient, identifying the specific mutations that led to that individual’s cancer and combatting accordingly – the ultimate targeted therapy. As of February 2021, it was noted that over 20 mRNA-based immunotherapies were in clinical development for solid tumour treatment. Given the success of mRNA technology in the COVID-19 vaccination programme, we feel this is a noteworthy space to watch.

The Impact of the COVID-19 Pandemic

It goes without saying that the COVID-19 pandemic has had a profound and multifaceted impact on healthcare globally, and Dr Hans Henri P. Kruge, WHO Regional Director for Europe, has cited a ‘catastrophic’ impact on cancer care itself. Whilst long-term implications are yet to be fully realized, there are already some tell-tale signs and predictors of possible effects on the oncology treatment landscape.

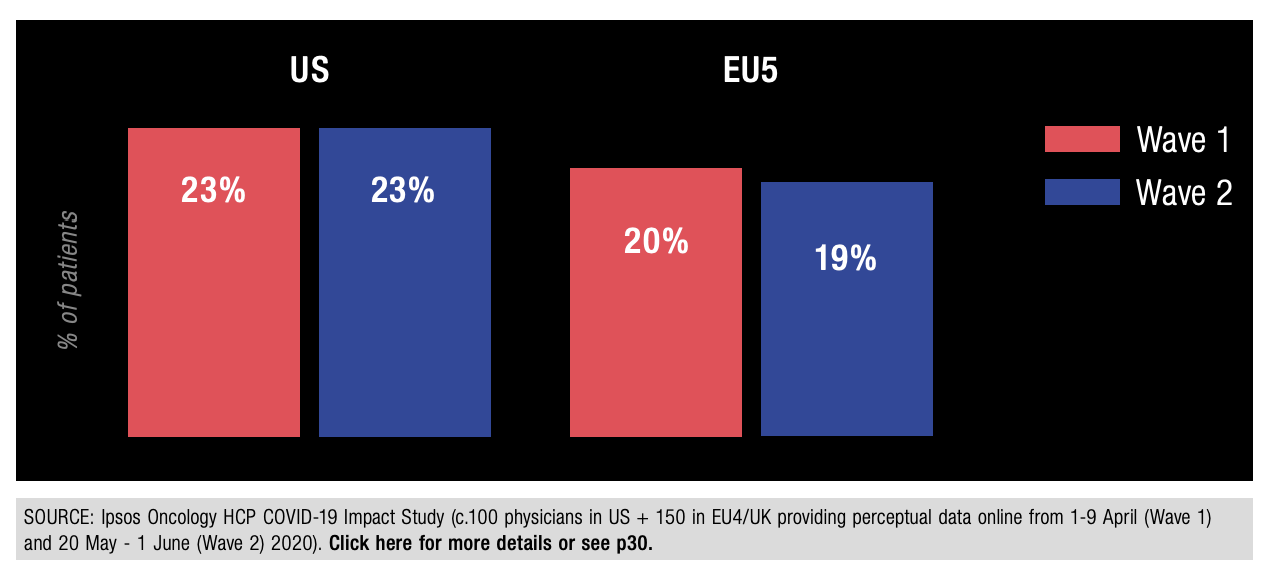

During April 2020, Ipsos conducted the first wave of our Oncology HCP COVID-19 Impact Assessment Study, an online perceptual survey amongst our US and EU5 Oncology Monitor respondents to gauge perceived initial impact of the pandemic on their patient caseload and management. Approximately 1/5 of sampled physicians across both regions cited experiencing ‘extreme delays’ in diagnosing cancer – a figure that held true during a second wave of the study conducted in May 2020:

Figure 15: Percentage of Sampled Physicians Citing ‘Extreme Delays’ to Diagnosing Cancer

Figure 15: Percentage of Sampled Physicians Citing ‘Extreme Delays’ to Diagnosing Cancer

Delays to diagnosis may mean progression of cancers that require more aggressive treatments and more holistic support services, resulting in an altered patient experience.

Following on from this is the inevitable question of mortality and what potential effects may be. Modelling outputs are already in place and one such example uses English cancer registry and hospital administrative datasets to predict mortality increases up to 5 years after diagnosis. Across breast, colorectal, lung and oesophageal cancer, increase estimations range from 5.8 – 16.6%, depending on tumour type.

Effects of the pandemic may play out for years to come and it is another factor we now have to consider when assessing the oncology space as a whole.

The Implications for Marketers

As we have tried to establish in this paper, the oncology market rarely stands still. This constant evolution affects oncology marketers and market researchers alike. Whatever specific challenges or objectives are in play – and these will be many and various – there are certain common challenges and look-outs for all of us working in oncology today:

Personalized medicine

The personalization of medicine has transformed the oncology treatment landscape. As established earlier on, we have tests today (e.g. BRCA 1/2 mutations) that can identify individuals with a higher lifetime risk of developing ovarian and/or breast cancer, enabling them to take early preventative action. Then, of course, we have biomarker tests to understand which therapy is likely to be most effective against that individual’s particular cancer, and the biomarker testing landscape is undergoing multiple revolutions, with tumour-agnostic sequencing panels based on solid or liquid biopsies helping to drive this transformation. Personalized medicine is set to evolve still further in the future, with cancer vaccines being developed and ongoing approvals of CAR-T therapies that use a patient’s own genetically modified immune cells to fight cancer. For marketers, the implication of all this is clear: a catch-all approach is unlikely to succeed. As treatments become increasingly personalized, so too must the marketing strategies around them.

Proof of value

Cancer (and other) treatments have become so expensive in recent years that the overall value of each has been placed firmly in the spotlight. The industry’s focus on value, and the dawn of value-based pricing, is another big change in the industry. Today’s oncology marketers must create the right messages for payers; they must understand the importance of real-world data and create a plan that showcases the product’s value, efficacy and patient outcomes.

The proliferation of data

Today, data are literally everywhere. We have public data, claims data, syndicated data, patient record forms, electronic medical records, social media… What to do with all this data is still unclear to many. Ultimately, these datasets must all be analyzed in order to gain a full understanding of what’s really happening in the market. For marketers, understanding how to integrate the data and use it to answer the commercial questions is critical – and a significant challenge they face.

Patient centricity

And what about patients themselves? Twenty years ago, oncology marketing and marketing research was all about the Oncologist. Today, it’s about the physician, other healthcare providers such as nurses, the payor and the patient. After all, today’s patients have a wealth of information at their fingertips and countless communities through which to share their experiences and ideas. In addition, both patients and their caregivers are becoming increasingly aware of the importance of personalized medicine and associated biomarker tests. As such, they are increasingly part of the decision-making team when it comes to their own care. Not only is this changing the dynamic between doctors and patients, it has also shifted the focus of pharma. Patient-centricity is not only well documented in corporate visions and missions, it is at the top of many pharmaceutical company agendas. This is a big change in the industry, with marketers needing to heed the shift from product to patient centricity

Achieving differentiation

One of the biggest challenges, and a lookout for marketers and market researchers, is differentiation. This is one area in which a patient-centric approach can help. Looking beyond the mechanism of action, what is the patient’s experience? What is their quality of life? What are their challenges? What are they frustrated with? Do they get enough specific information? Cancer is complicated and listening to the patient’s voice and directing the right information and support to them – and their caregivers – could be a strong point of difference.

Closing

Of course, one of the biggest challenges of working in cancer is that we’re focusing on diseases that, generally, do not yet have cures (unless they are diagnosed in early stages). However, there has been so much progress made in such a short space of time. The understanding that we now have of the pathogenesis and pathophysiology of cancer, the personalization of treatment via treatment selective biomarkers, the rise of immuno-oncology – all of this will lead to yet more advances in cancer treatment. As the industry continues to advance, we can potentially expect advanced cancers to become chronic diseases rather than terminal ones, until true cures are eventually discovered. All of us currently working in cancer are waiting for the day this happens.

![[WEBINAR] Cracking the Nutritional Supplement Market](/sites/default/files/styles/list_item_image/public/ct/event/2026-05/thumbnail-cracking-nutritional-supplement.png?itok=Cts0kD4T)

![[WEBINAR] Dealmaking 2026: What’s Changing, What’s Not, and How to Position for the Next Wave](/sites/default/files/styles/list_item_image/public/ct/event/2026-03/deal.png?itok=NtU1lGCc)