Why payment card surcharges don’t add up for merchants

KEY FINDINGS:

- Surcharging debit and credit transactions costs the average merchant more in lost sales

than they offset in customer surcharge fees. - Surcharging reduces the debit and credit card spend as well as the revenue at merchants who surcharge.

- Merchants who surcharge see approximately a 10% reduction in same store debit and credit sales as customers change their purchase behavior to offset the fees.

In recent years, independent merchants have begun implementing a payment card surcharge. Surcharges are additional fees that merchants add to a customer’s bill when using a card for payment. Surcharging is allowed on credit purchases in most states in the United States, but merchants must disclose the surcharge dollar amount on every receipt and post that the merchant assesses a surcharge at the point-of-entry and point-of-sale. Surcharging is never permitted on debit purchases.

Merchant surcharging grew significantly through 2021 and 2022 in response to inflationary pressures. As COVID-19 drove customers away from using cash and toward plastic, and inflation rates in the United States reached 8% in 2022, merchants sought a method of mitigating increased credit and debit fees by passing those costs along to the customer.

In 2022, Ipsos saw the incidence of surcharging reach 31% at independent and small merchants in specific categories (restaurants, hairdressers, liquor stores, convenience stores, gas stations, bakeries, etc.). Surcharge fees have also increased along with their incidence, from 1–2% in 2019 to as high as 3–4% in 2022.

Ipsos wanted to understand the financial impact on merchants of surcharging customers on debit and credit transactions. We conducted an independent analysis of changes in customer behavior at merchants where surcharges are applied compared to those where surcharges are not applied.

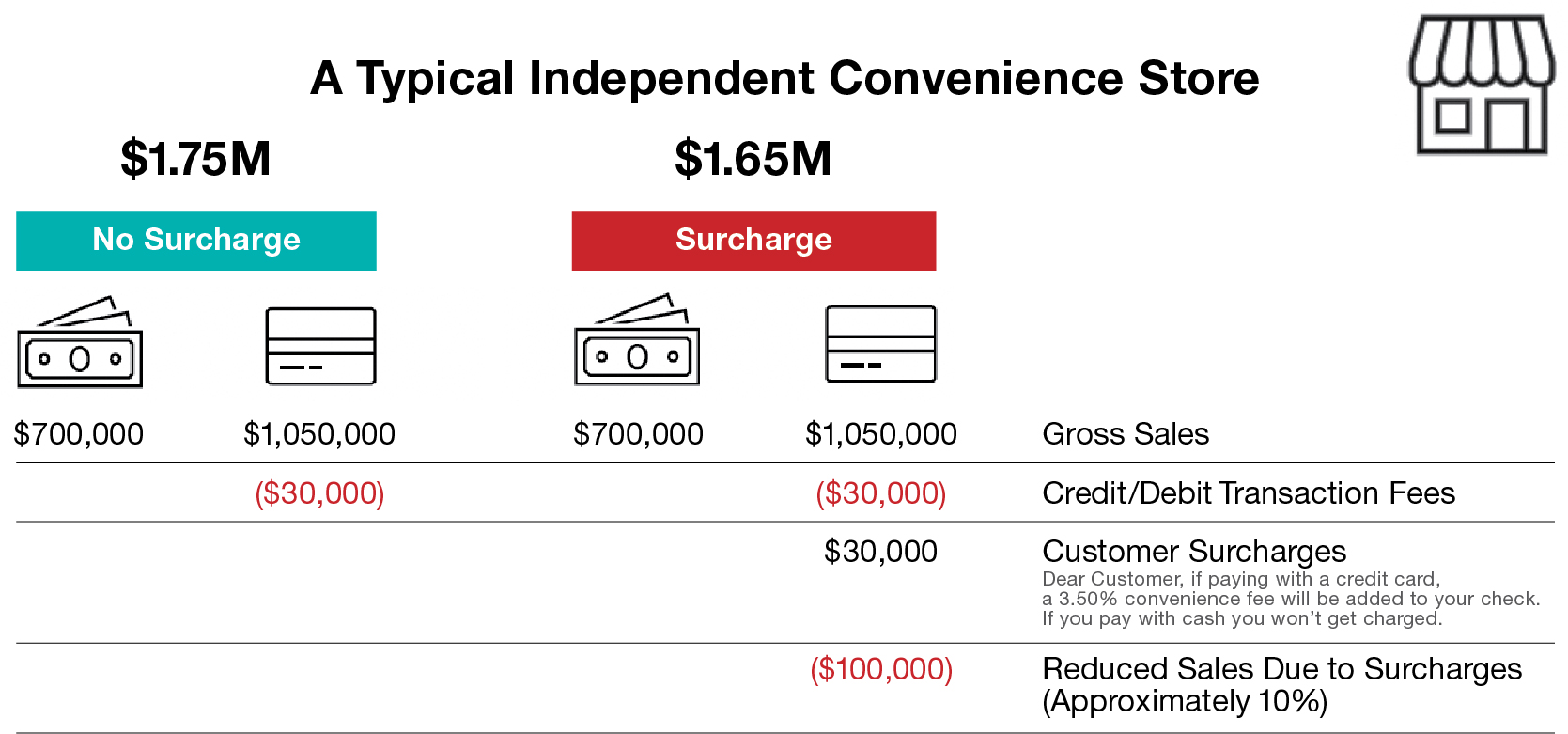

In short, surcharging debit and credit transactions costs the average merchant more in lost sales than they offset in customer surcharge fees. Merchants who surcharge see approximately a 10% reduction in same store debit and credit sales as customers change their purchase behavior to offset the fees.1 In the example of a typical independent convenience store below, annual revenue of $1.75M drops to only $1.65M with surcharging; a decline of $100K caused by customers reducing their spend to compensate for merchants passing surcharges along to customers.

1 Ipsos Geo-Intercept Survey of Shoppers, November 2022. n=1000 completed interviews

But that’s only the immediately measurable financial impact that results from merchants passing transaction fees onto customers in the form of surcharging. We also learned from this research that customers change their long-term behavior because of merchant surcharging. Specifically:

Furthermore, we know that customers spend up to twice as much per transaction when using a debit or credit card than they spend using cash, meaning that not only does surcharging reduce the debit and credit card spend, it also reduces the revenue at merchants who surcharge as the debit and credit transactions are replaced with lower value cash transactions.

In conclusion, we know that merchants feel the pain of paying fees on debit and credit card payments, but our assessment of the situation suggests that merchants who attempt to pass those fees on to customers in the form of surcharging are financially worse off in the short term. In addition, the longer-term impact on the merchant in the form of lost customers and reduced transaction value, while more difficult to calculate, should not be ignored.

Independent merchants should carefully evaluate the financial implications of surcharging before they attempt to pass these fees on to customers. While customers are willing to accept the increased cost of goods sold due to inflation, they are unwilling to accept having credit and debit surcharge fees passed onto them. In the example above, lost revenue because of recouping transaction fees results in a net revenue loss to the merchant of −$100K annually!

Want to take action? Reach out to Ipsos Channel Performance to audit and educate your merchants on the negative impact of customer surcharging.

Authors

Carlos Aragon

SVP, Ipsos Channel Performance

[email protected]

Kaili Hunsaker

Director, Ipsos Channel Performance

[email protected]

About Ipsos

At Ipsos we are passionately curious about people, markets, brands, and society. We deliver information and analysis that makes our complex world easier and faster to navigate and inspires our clients to make smarter decisions. With a strong presence in 90 countries, Ipsos employs more than 18,000 people and conducts research programs in more than 100 countries. Founded in France in 1975, Ipsos is controlled and managed by research professionals.

![[WEBINAR] Global Voices of Experience 2026](/sites/default/files/styles/list_item_image/public/ct/event/2026-02/thumbnail-global-voices-experience.jpg?itok=NN6W-9Ft)

![[WEBINAR] Increasing Efficiencies in Service Delivery in the Public Sector](/sites/default/files/styles/list_item_image/public/ct/event/2025-01/feature_4.png?itok=0fa4kfCx)