What’s Next – Financial Services Post Pandemic Implications

Given vaccination rates and increasing consumer confidence, financial services brands must prepare now to address economic recovery and a transformed market once the pandemic is over.

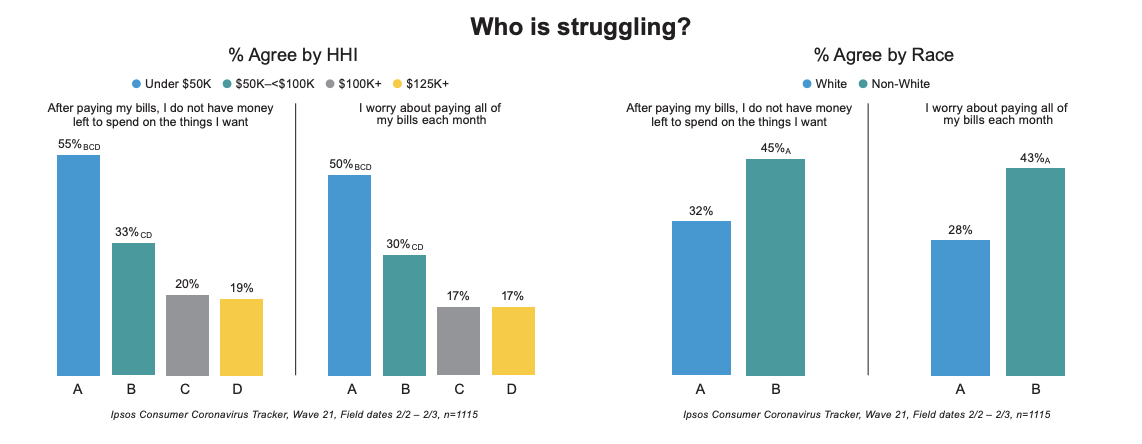

COVID has highlighted and exacerbated the many economic inequalities that exist in our society. While some segments of the population faced job losses, depleted savings and overall extreme financial hardship, others prospered through increased savings, capital gains and debt reduction during the past year.

This unequal experience of the pandemic has shaped these two divergent groups’ perceptions on what “post-pandemic” means. Financial services providers will need to balance serving these two very different groups during what many economists are calling a “K-shaped recovery” when developing communications, creating new products and serving customers.

Behavioral Science principles, however, reveal that we may be able to peer into the future through one’s current vaccination status. From a psychological standpoint, getting vaccinated (or being scheduled to get vaccinated) is a “temporal milestone” much like a birthday or New Year’s Day, marking a fresh start. In this case, getting vaccinated indicates that the pandemic is effectively over.

With a national rollout, a subset of the population is currently vaccinated. For this group, they are already in a “post pandemic” mindset. Conversely with the remaining population still waiting for their opportunity to receive the vaccine, this group is still currently living as we have been since March 2020—in a “during pandemic” mindset.

We are therefore, in a unique moment in time where research can reveal significant differences between the two groups and provide strategic business guidance on where to focus on post pandemic strategic efforts.

Download our recent paper for more insights and tips.

Key Themes:

- Confidence is rising for most. For affluent consumers, there is pent-up demand to spend

- COVID-19 increased inequality; consumers expect financial services to address it

- New products, messaging and customer experiences will be required during the K-shaped recovery

As vaccinations in the U.S. and around the world pick up steam, many companies are looking ahead to the economic recovery from COVID-19 —and this recovery will involve the financial services sector in an especially crucial role.

COVID-19 has highlighted and exacerbated the many economic inequalities that exist in our society. While some segments of the population faced job losses, depleted savings and overall extreme financial hardship, others prospered through increased savings, capital gains and debt reduction during the past year.

This unequal experience of the pandemic has shaped these two divergent groups’ perceptions on what “post-pandemic” means. Financial services providers will need to balance serving these two very different groups during what many economists are calling a “K-shaped recovery” when developing communications, creating new products and serving customers.

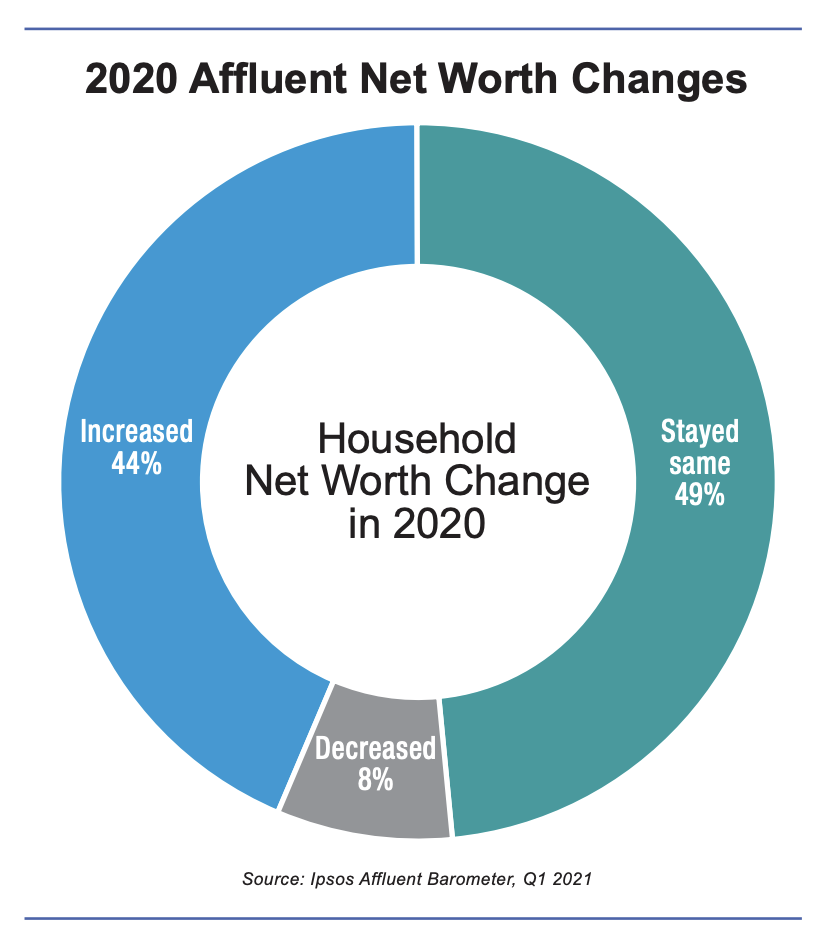

Among the affluent population, four in 10 share that their net worth increased in 2020. With fewer options for discretionary spending (e.g. travel, entertainment and dining) for a year, this group was able to increase savings substantially and pay down or refinance high-interest debt. Restrictions will likely be lifted this summer and there will be a surge of consumer spending due to this pent-up purchasing power and current rates of vaccination. There are several opportunities for financial services providers to consider.

Credit Card Rewards

With travel and entertainment shut down for a year, many rewards earning and redemption opportunities on the most popular credit cards became irrelevant. Many issuers shifted categories on both sides of the equation to continue capturing spend during the pandemic. Consumers were able to earn (and in some cases, redeem) rewards on categories that were most pandemic-relevant, such as groceries, takeout/delivery services and streaming platforms.

However, once travel and entertainment comes back to life, issuers will have to consider:

- Which of these pandemic-era rewards categories should continue?

- What is the impact on the original card value proposition of these earning categories, outside of a pandemic context?

Additionally, travel points balances have swelled in the past year due to the lack of redemption opportunities. Once restrictions are lifted, demand may overwhelm supply. Issuers may need to nudge cardholder redemption activity by introducing additional rewards flexibility to ensure a healthy balance sheet and customer satisfaction. Ultimately, issuers will have to determine what optimal combinations of earn and redeem categories cardholders will accept.

Wealth Management

Increased savings is an opportunity for both financial services providers and customers. For the first time in their lives, some consumers are in the serendipitous position to have a good chunk of money to put away. For those that were already financially disciplined, the newfound additional savings allow for new wealth building opportunities. Areas for wealth management providers to focus on include:

- How to convince first-time investors to take the first step to financial health and ensure continued financial discipline

- What new services and investment vehicles can be offered to new and existing investors to preserve and grow the sudden increase in investable assets

Addressing Inequality

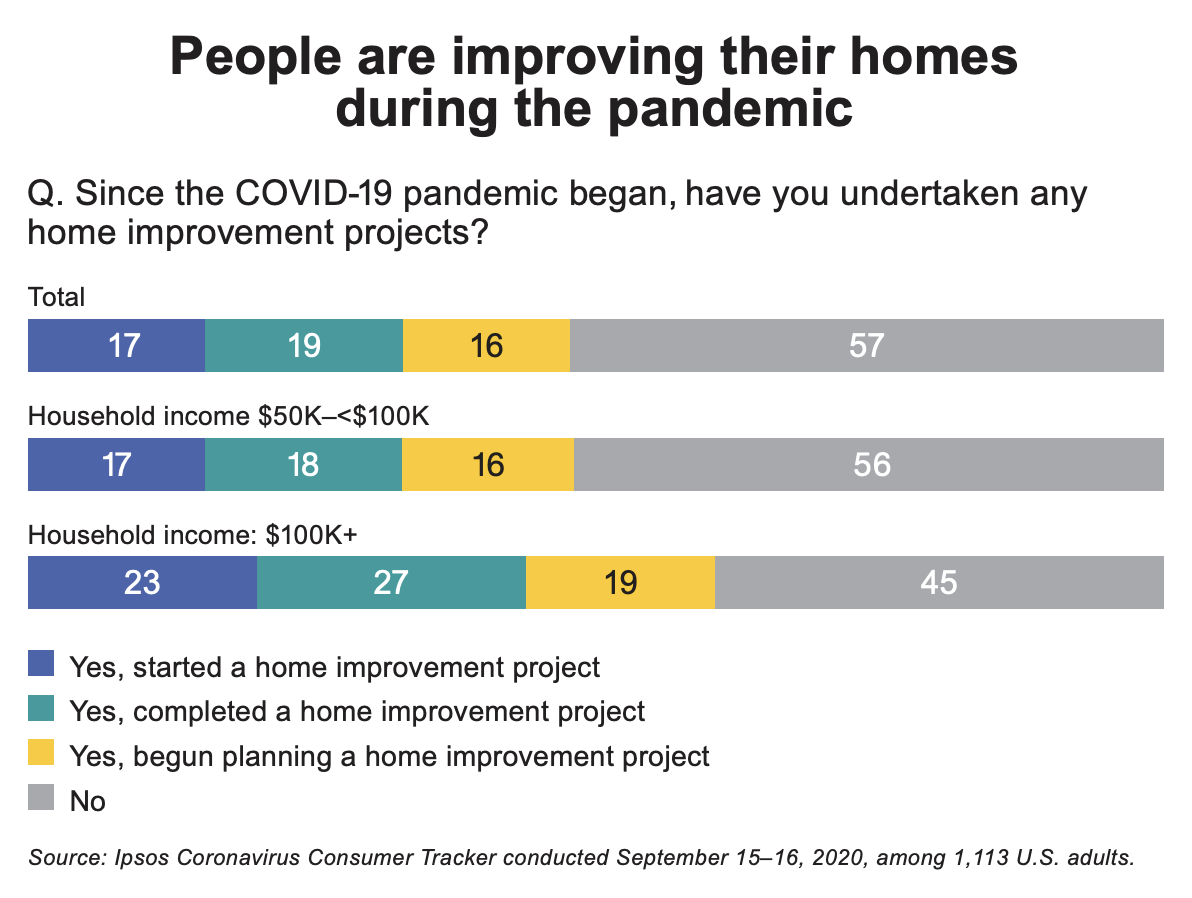

The pandemic also triggered a confluence of events that greatly impacted home lending. First, with everybody locked down, many yearned to upgrade their home environments. Secondly, home sales skyrocketed and increased home values as buyers sought bigger homes with outdoor space. Finally, mortgage rates dropped and remained at new lows. As a result, new mortgages and refinances—specifically cash-out refinances—reached volumes not seen since the period before the 2008 financial crisis, according to the Wall Street Journal. Industry analysts foresee a slowdown in home lending coming unless rates drop even lower and trigger a new wave of customers.

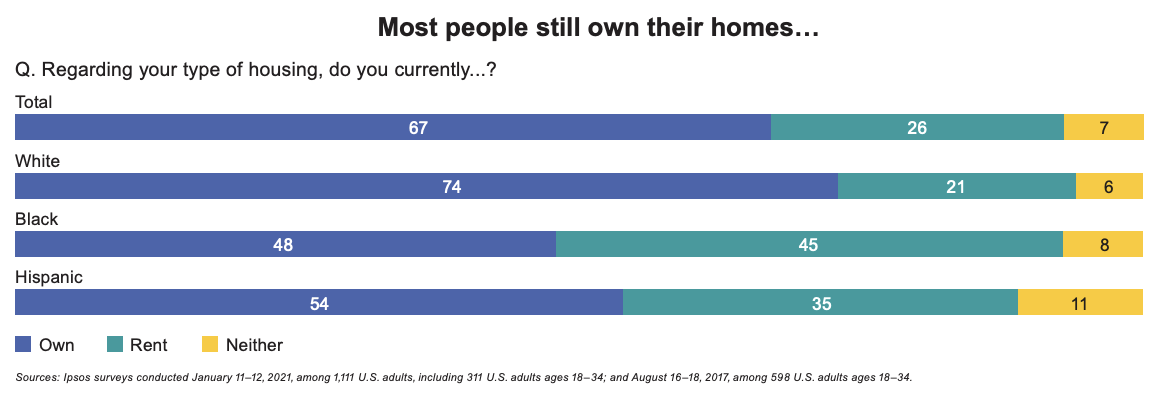

However, the financial services sector may be able to use home lending to achieve the renewed commitments made towards financial inclusion after the racial justice protests in 2020. Home ownership is one of the most effective pathways to build wealth. Banks and lenders are in a particularly influential position during the recovery to help underserved communities achieve this goal.

Financial services providers can make home loans more accessible beyond current assistance programs by dedicating resources to understand the unique experiences and financial dynamics of each community. This will then enable the sector to create specific financial products to address unique unmet needs. Specifically, lenders can:

- Invest in new models and alternative ways to assess risk.

- Innovate around new loan structures that may better match non-traditional income dynamics of different communities.

Beyond this, the financial service sector must also plan on how to simultaneously serve the population which suffered the effects of the pandemic the most. COVID-19 cut across racial, socioeconomic and gender lines, disproportionately affecting communities of color, lower-income workers and women. Banks have a unique opportunity to help these segments of the population get back on their feet once the pandemic is officially declared over. This focus not only supports the sector’s commitment to diversity, equity and inclusion, but also fulfills customers’ expectations of companies in the post-pandemic era.

Prioritizing easier access to credit and reimagining traditional risk profiles can jump start innovations in recovery-specific products for impacted populations.

Immediately during the recovery, these populations will need purchasing power, cash flow and a path towards building back up their savings again beyond anything that they receive from the latest relief bill. Banks can accommodate this and create new products, perhaps specifically for this time period. Later, as this new population builds up credit and demonstrates its finan - cial responsibility, banks can convert the products into more traditional ones for these newly acquired customers. Additionally, similar re-thinks of access to credit and risk profiles should also concurrently be applied to small businesses that serve these impacted communities. Innovations that quickly generate working capital to finance training and planning activities during the transition period will help SMBs fully prepare for a post pandemic reopening.

Given vaccination rates and increasing consumer confidence, brands must prepare now to address a transformed market once the pandemic is over. Currently, a potential concern may be that it is difficult for consumers to share what anticipated needs and attitudes will be later, when we are all still in the middle of quasi-lockdowns and community spread.

Behavioral Science principles, however, reveal that we may be able to peer into the future through one’s current vaccination status. From a psychological standpoint, getting vaccinated (or being scheduled to get vaccinated) is a “temporal milestone” much like a birthday or New Year’s Day, marking a fresh start. In this case, getting vaccinated indicates that the pandemic is effectively over.

With a national rollout, a subset of the population is currently vaccinated. For this group, they are already in a “post pandemic” mindset. Conversely with the remaining population still waiting for their opportunity to receive the vaccine, this group is still currently living as we have been since March 2020—in a “during pandemic” mindset.

We are therefore, in a unique moment in time where research can reveal significant differences between the two groups and provide strategic business guidance on where to focus on post pandemic strategic efforts.

![[WEBINAR] The Modern Twenty-Something: How Gen Z Thinks About Money, Milestones, and More](/sites/default/files/styles/list_item_image/public/ct/event/2026-07/thumbnail-templates_0.png?itok=GNEHIkP1)