The Digital Difference: Ensuring Your Digital Experiences Meet Heightened Expectations

KEY TAKEAWAYS:

- When evaluating opportunities to improve the customer experience, it’s imperative to estimate the impact with specific consideration for the reach of those enhancements.

- Brands must always monitor their customer journeys and touchpoints for “hot spots” and have a system for quick identification and remediation.

- Closing the loop with customers who have expressed a negative experience—or those we can assume are dissatisfied through contextual and behavioral data—is a must. When a negative experience is remediated, it can become one of the most memorable experiences a customer has with the brand.

As human interactions resumed in 2022 post-COVID-19 vaccinations, we sought to understand how consumer reliance on digital channels was shifting and how expectations changed for physical channels (i.e., stores) and human interactions (i.e., phone customer service). Our 2022 research¹ surfaced high expectations for omni-channel consistency, as well as higher standards for in-person interactions than digital interactions. This year, we’ve repeated the study² to explore what changes are here to stay and how expectations vary for those who work remotely versus those who have returned to a workplace commute.

Digital Experience (DX) Consistency

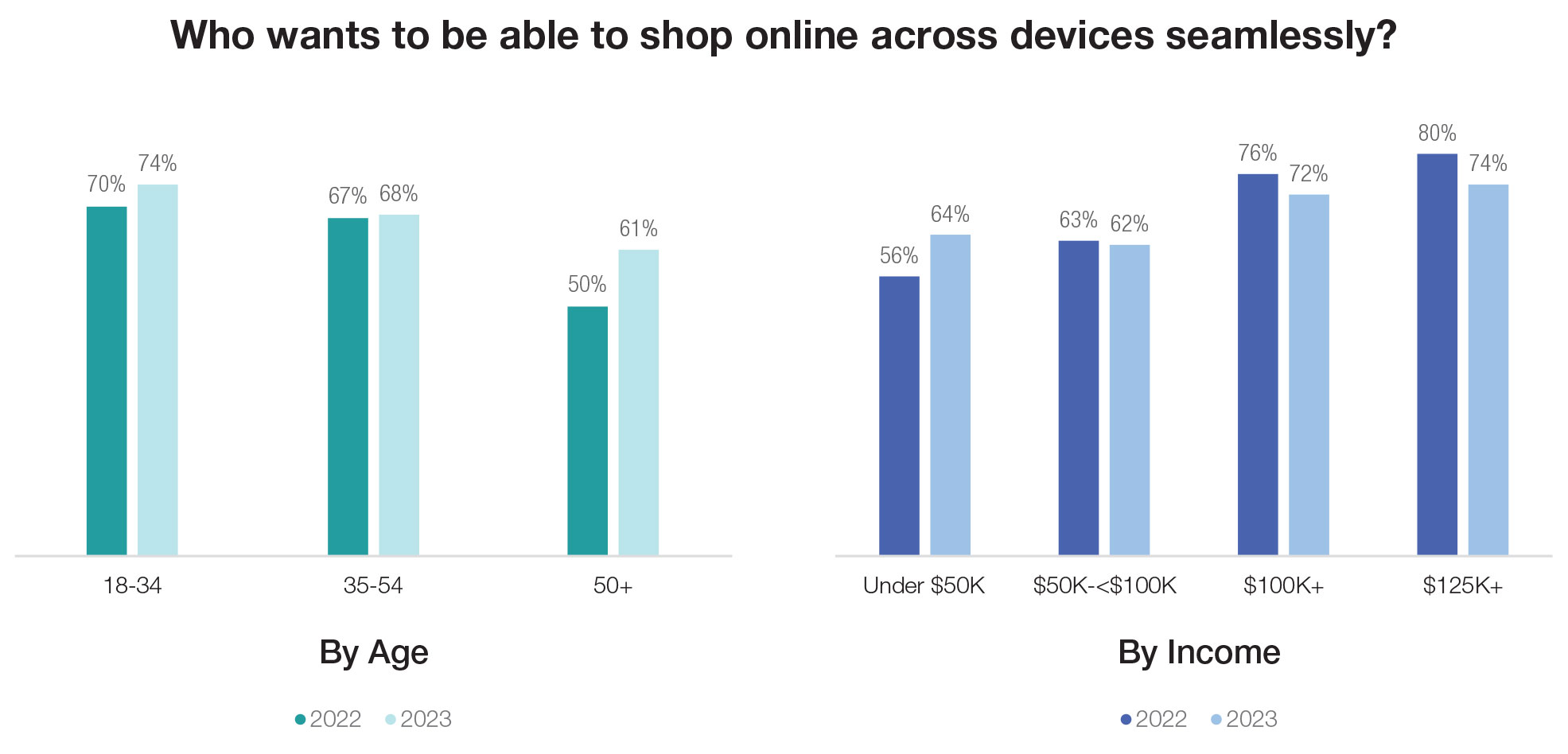

Last year, we uncovered that over half of individuals regardless of age or income level expect to be able to interact seamlessly with brands regardless of device (smartphone, tablet, computer) whether on a website, mobile web or mobile app. Such consistency in expectations across digital channels is an outcome of the COVID-era: Brands can no longer sustain inconsistent functionality across web browsers, Android and iOS or their web/app experiences.

In 2023, we observed a 20% increase in this expectation for the 50+ cohort, which signals that there is less difference in expectations for the “digital native” vs older generations than previously observed. Higher income earners may have had inflated expectations in 2022 that have since tempered.

In 2022, busy parents exhibited the least patience for poor usability, with 73% of households with children expecting a seamless experience vs. 58% of those without. In 2023, the rates have increased to 76% and 63%, respectively.

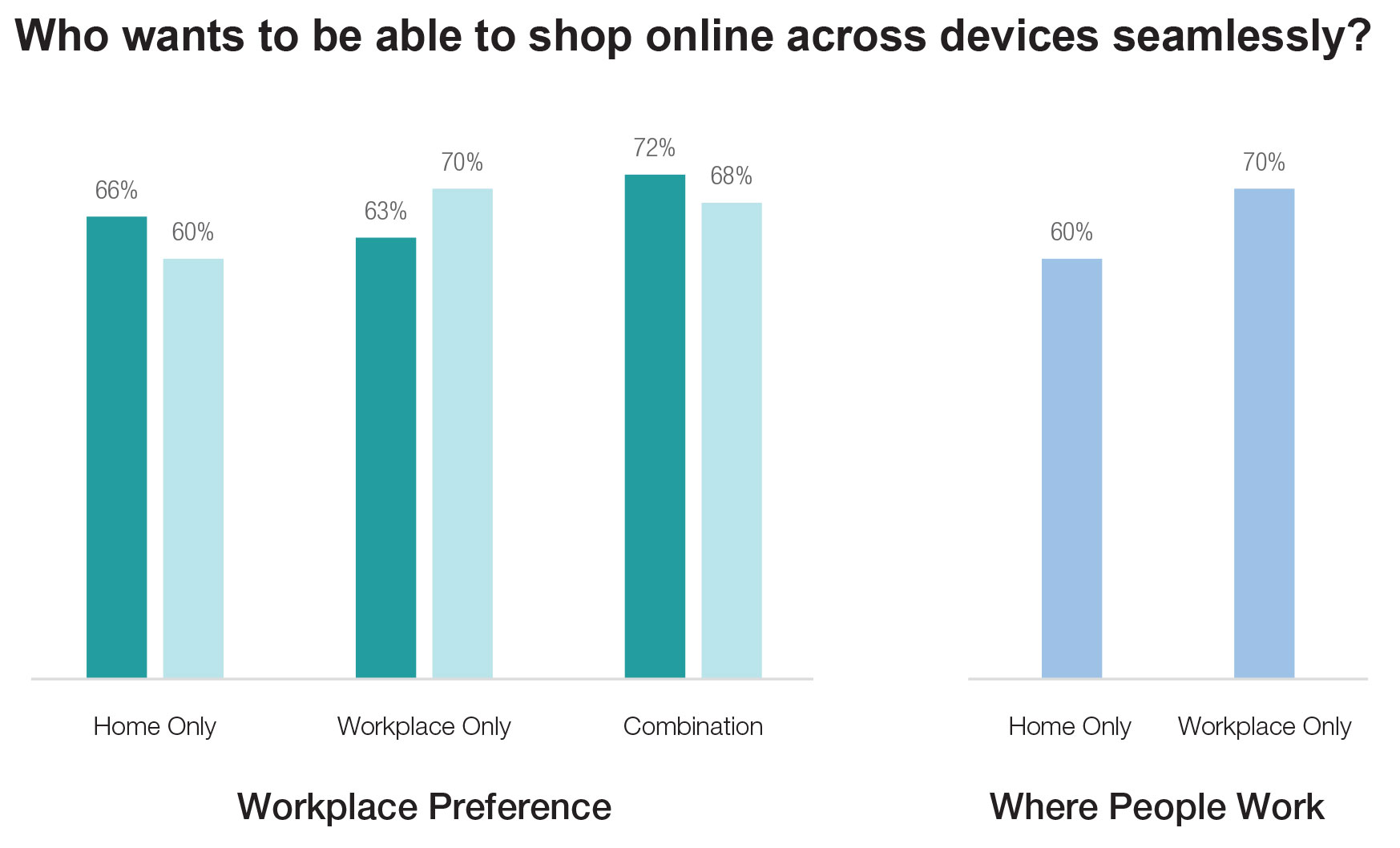

Last year, many organizations were defining their Future of Work policies, so we explored the data by work location preference. In 2022, those who preferred the workplace had the lowest expectations for consistent, seamless digital experiences (63%). In 2023, those with the workplace preference have the highest expectations (70%). We explored the data by actual workplace policy and found that those who are workplace only laborers have a 10-point higher expectation for seamless digital experiences than those who work from home. We hypothesize this is due to reliance on multi-tasking during commutes and the overall time loss from a daily commute.

Ipsos CX Guidance:

- Expectations across demographics are converging around consistency; ensure your digital experiences are consistent across channels.

- Measure the effectiveness of each channel independently to identify relative strengths and weaknesses.

- Institute a continuous cycle of DX measurement and optimization to ensure experiences are meeting ever-increasing expectations.

Pressure on the Front-Line is Tempered

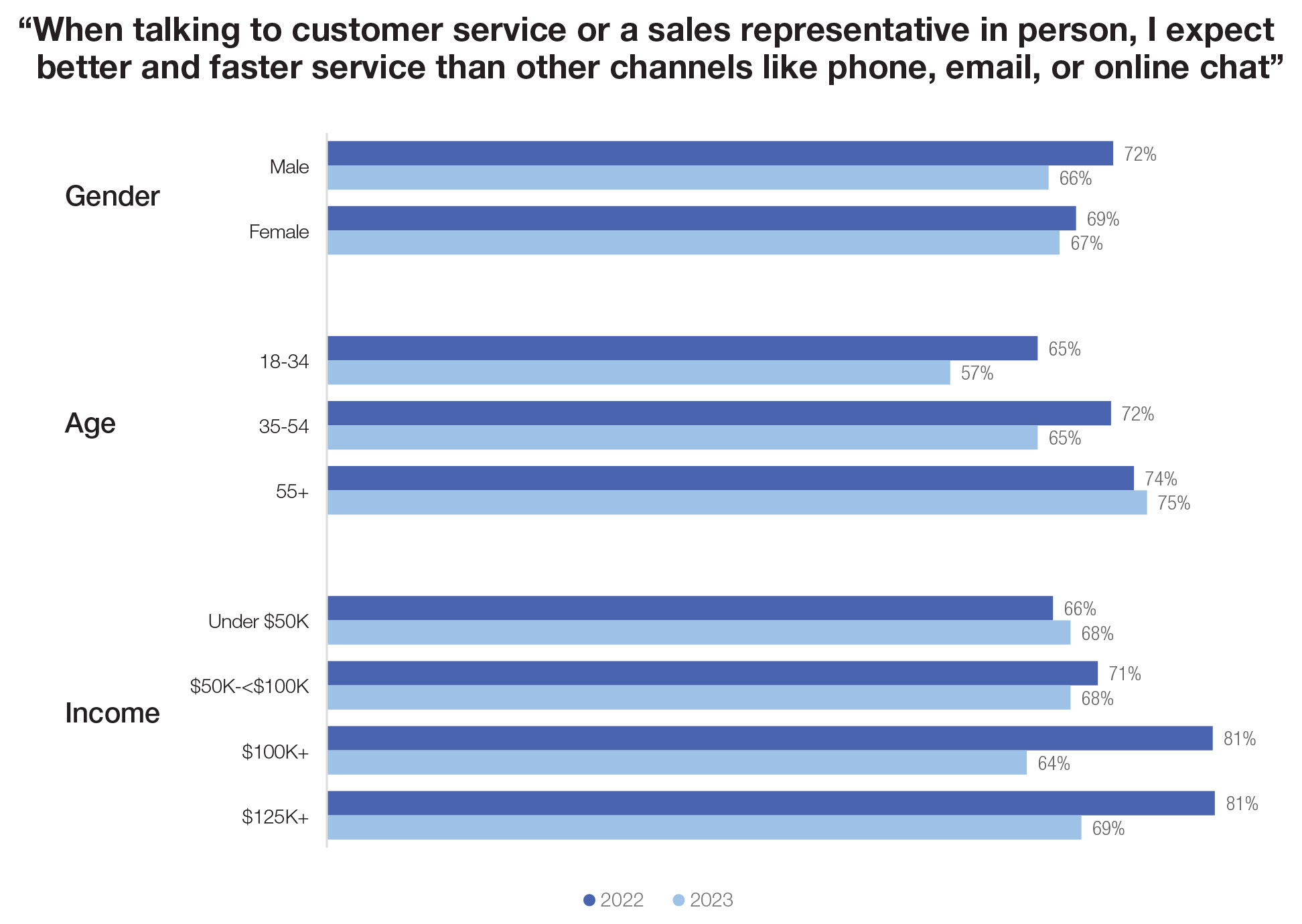

Throughout the pandemic, we saw expectations loosen as consumers empathized with staffing shortages and frontline workers. In 2022, however, we saw extremely high expectations for face-to-face human interactions. While the expectation remains for over 50% of respondents, it’s more tempered in 2023 than in 2022.

Notably, this expectation has dropped 8-points for those age 18-34. This may be due to the recognition and adoption of significant self-service digital capabilities across industries. As age increases, so does expectations of the front-line, which signals where digital natives vs. hybrid or analog consumers differ. While expectations for digital experience consistency are converging, we are still seeing distinction by age for human interactions.

The greatest change year over year is the 17-point drop for $100K+ income earners, such that expectations are now similar across income levels. This may reflect improvements in digital offerings and experiences resulting from investments organizations made in their digital channels from 2020-2022.

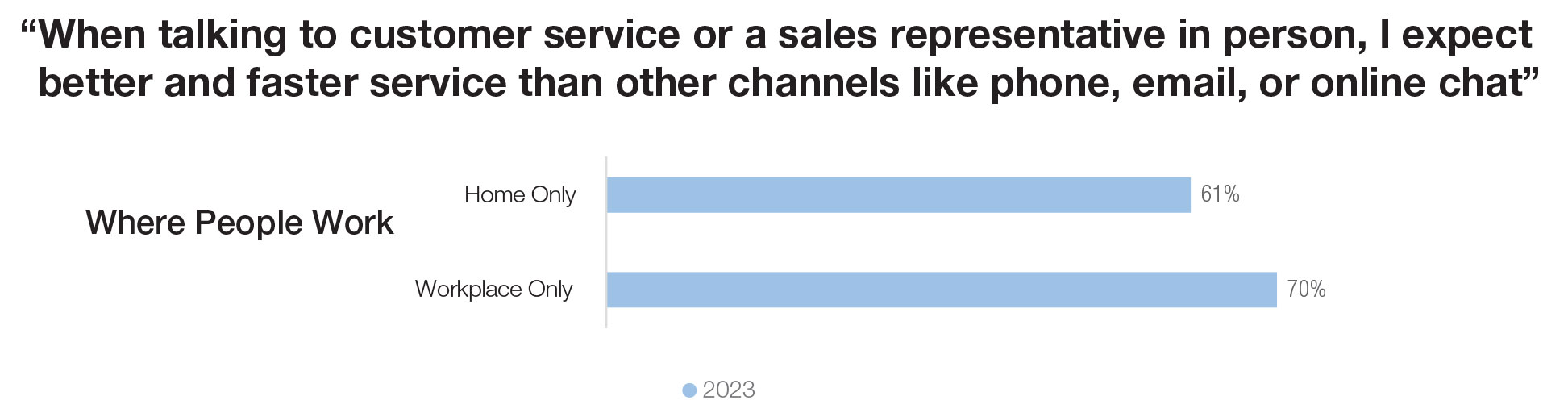

As for work-from-home vs. workplace arrangements, once again expectations are higher for those commuting to their workplace. Convenience might be at play, or this heightened expectation could be a projection of the expectations they face as in-workplace employees.

Ipsos CX Guidance:

- Deeply understand the role each channel plays in the customer journey, including your frontline touchpoints, as only measuring digital will miss a key part of the customer journey.

- Recognize that while expectations on the front-line are more tempered in 2023, they are still tasked to deliver better, faster service — a Voice of Employee program can uncover opportunities to better enable and empower the front-line to deliver great Customer Experience.

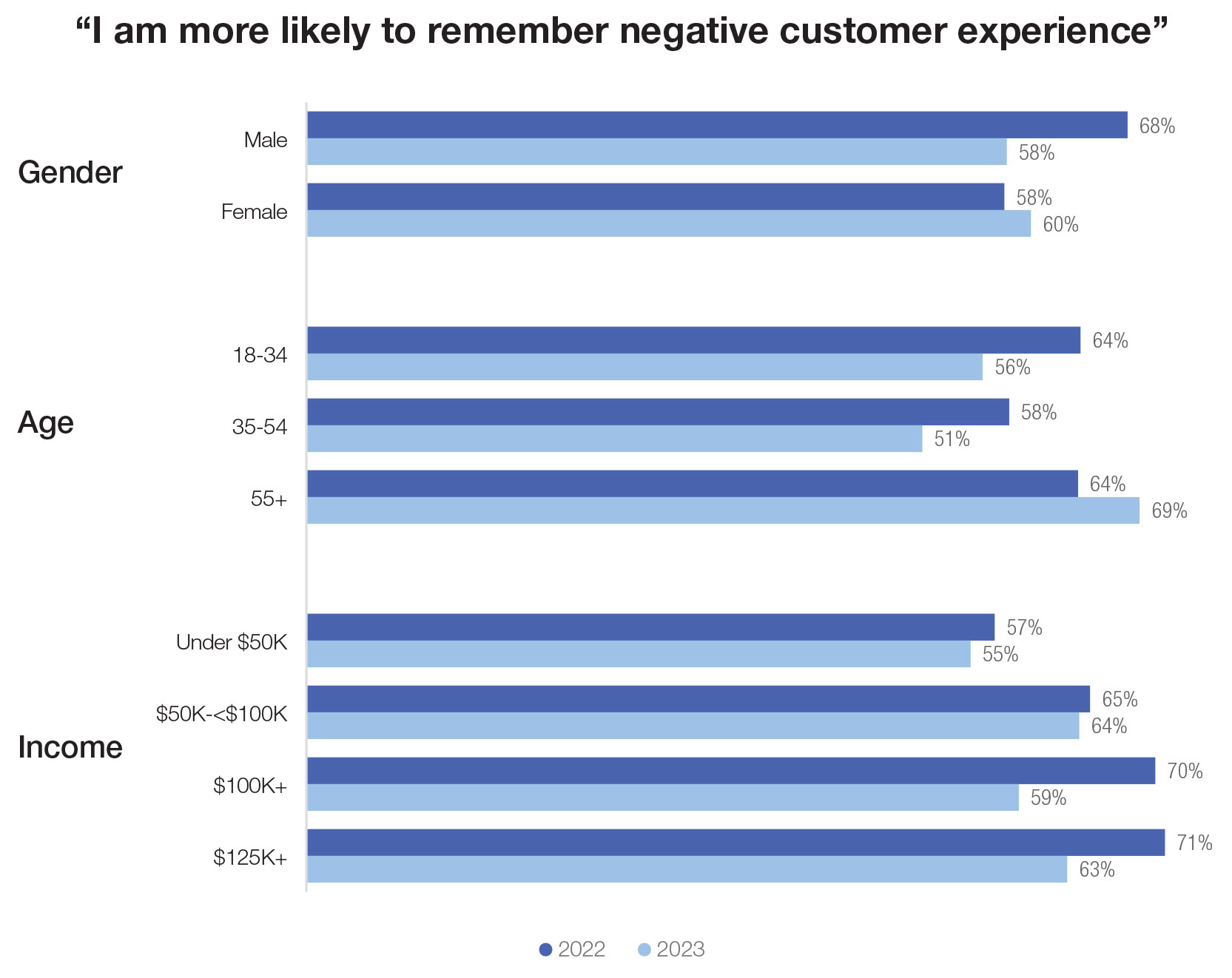

All Experiences are Memorable

In any Customer Experience measurement program, there is a desire to capture a representative sample of experience feedback. When feedback is largely negative, CX stakeholders may quickly suggest that those with a negative experience are more likely to provide feedback since negative experiences tend to have a higher emotional impact. In 2022, we sought to explore the likelihood of remembering negative experiences over neutral or positive ones. We found that affluent males were most likely to have that bias. However, in 2023 we see declines in this tendency across most demographics.

This trend is a great signal for CX program owners: It’s unlikely that you’re getting an over-representation of negative experience responses in your feedback data.

What’s Next:

- When stakeholders discredit a program’s validity, double down on the importance of representative feedback and the validity of your sample set.

- Know that there is still a slight tendency to remember missed expectations vs. those that are met or exceeded, so improving CX metrics is an important churn prevention measure.

- Take advantage of the emotion that surrounds negative experiences. When those are addressed and remediated, that positive experience now carries the emotion.

Consumer expectations are constantly evolving. Ipsos CX works with the world’s leading brands to help them keep their finger on the pulse, retain customers and secure those at risk, grow share of spend, increase advocacy and secure a Return on their Customer Experience Investment (ROXCI). To learn more about how we ensure experiences across touchpoints are driving quantifiable value for our clients and their customers, get in touch with us ([email protected]).

![[WEBINAR] Global Voices of Experience 2026](/sites/default/files/styles/list_item_image/public/ct/event/2026-02/thumbnail-global-voices-experience.jpg?itok=NN6W-9Ft)

![[WEBINAR] Increasing Efficiencies in Service Delivery in the Public Sector](/sites/default/files/styles/list_item_image/public/ct/event/2025-01/feature_4.png?itok=0fa4kfCx)