Affluent Consumers During Covid: Part 1

Download our detailed Appendix featuring more data, charts, and insight featured in this article.

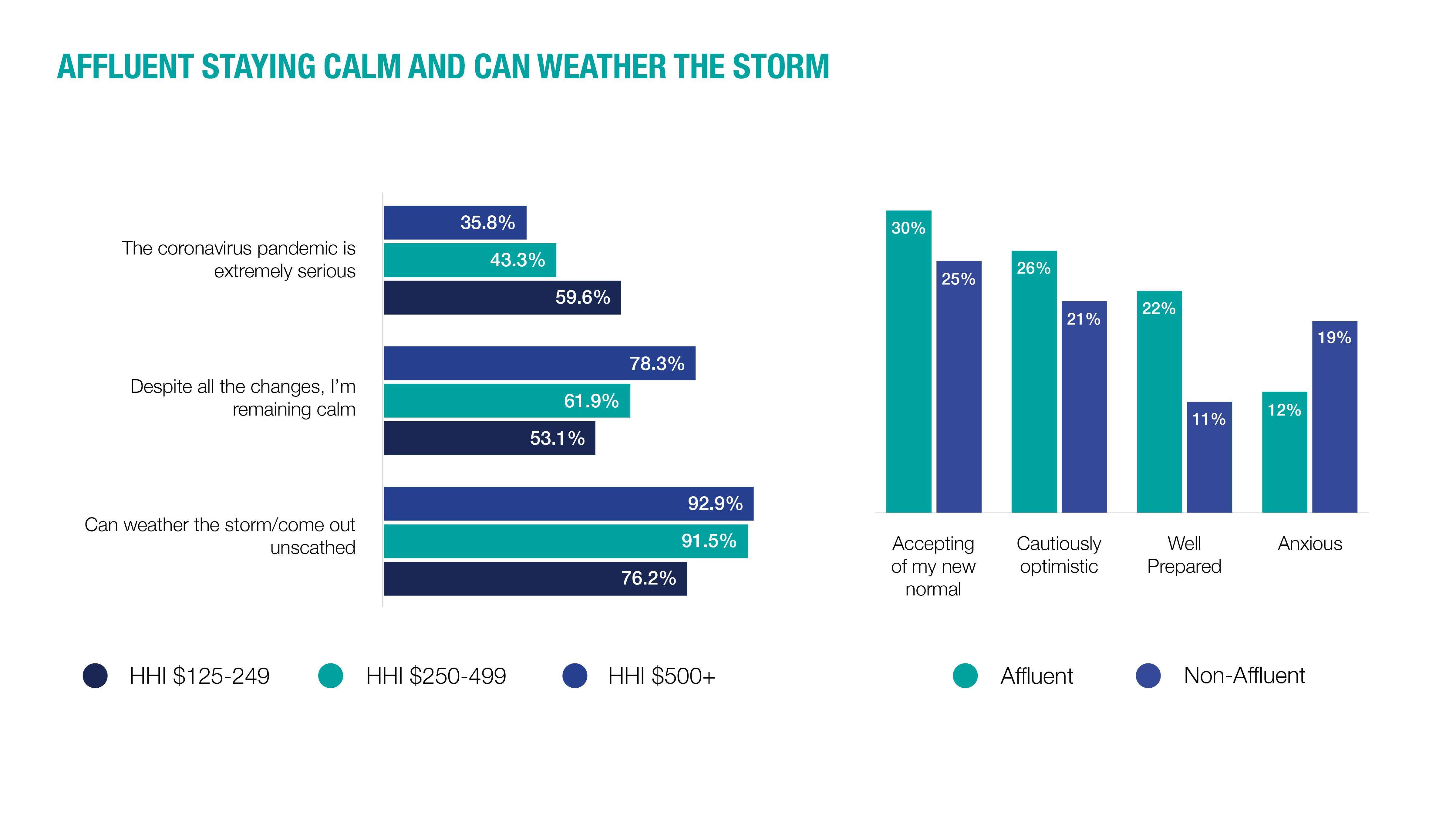

While affluent consumers have sometimes been called “crisis-proof”, they have exhibited anxiety and concern during past crises and again during the current one. In fact, anxiety and worry amongst affluent consumers continued for years after the Great Recession and declined very slowly over the first years, post-crisis.

Yet, data also shows that the Affluent are more insulated from economic crises and are the first to rebound post-crisis than non-affluent ones.

So how do you fulfill the needs of this resilient group?

After the Great recession, the affluent took an economic hit, just as the rest of the US population did. However, US Census data over the ensuing years show that this top 20% of consumers were the first to have their income rebound, and they’ve showed the highest growth since. In addition, the most affluent – the top 5% -- show the highest growth of all. This is likely what leads affluent consumers to be taking a generally more optimistic (or at least less anxious) view than the non-affluent.

That is not to say that the Affluent are a monolithic, singular identity group. In fact, we see a distinct duality in their attitudes and anxieties. On the one hand, measures of “now is a bad time to invest” and “a great time to invest” are both up appreciably. Similarly, plans to take on a more conservative AND a more aggressive approach with investments are also both up.

Implications: The Affluent audience represents a material opportunity audience for marketers during and immediately after the Coronavirus crisis. However, it’s important they truly understand the nuances of the audience and their varied mindsets. Brands need to have solutions and engagement opportunities that fit both the anxious and the calm sides of the affluent audience – and ensure they are targeted as best as possible.

Purchase behaviors changing

Another enormous difference between the current crisis and past economic crises is with regards to purchase behavior. Buying across many categories was severely affected during the Great Recession. The current crisis is significantly different in that it is external circumstances that have initially disrupted the purchase dynamic – in many categories, consumers are literally prevented from buying and many products and services are unavailable.

This is driving up both interest and demand among affluent consumers in many categories. First, data shows what we are calling the “Unattainable Effect” on psychographics. That is, many attitudes that are associated with categories that are literally off-limits right now are showing noteworthy increases vs. the pre-lockdown period. For example, we see sizable increases in the number of Affluents who agree that they like to go to sporting events, see movies on opening weekends, travel for work, or shop for clothes – all things unavailable to them at the moment.

In addition, we also see meaningful increases in demand across categories. Intent to purchase a new car or truck, home goods and services, apparel and more are showing significant rises vs. before the crisis. This is literally the definition of “pent-up demand” – intent to purchase increasing due to a current inability to buy.

Affluents’ Intentions for purchasing increasing

This leads us to a hypothesis that, unlike past crises, purchasing in many of these categories might take off as soon as restrictions are lifted. For example, while auto buying took some time to rebound in 2009-11, there’s a good chance it could return more quickly this time. Same with shopping in malls, going to movies, renovating homes, buying appliances, etc.

This also suggests that purchase journeys for these categories may be condensed or truncated following the lockdown. What will this do to purchase behaviors and how may they change? For one thing, we could expect even more digital/virtual research and shopping than before in all considered purchase categories. In fact, we are already seeing rises on desires to “…keep up with” many categories, like auto, fashion, and travel.

Implications: Brands and marketers need to understand the new dynamics in the paths to purchase for their categories. It is clear that the digital channel’s role in discovery, inspiration and research has only been accelerated during a time where brick-and-mortar channels are closed to consumers – thus brands need to provide more digital shopping tools and experiences that parallel that growth and feed consumers suffering from the “Unattainable Effect.” Data also shows the rising importance of social media for all consumers, especially affluent ones. Brands should find ways to leverage it for engagement, recommendations, and influence.

Also remember that many affluent consumers are aching to go back out and shop/visit the mall, as soon as the restrictions are lifted – nearly half of them say they are feeling claustrophobic and cooped up. It’s important to leverage an omni-channel approach to transition/link brand relationships from digital to physical channels. In addition, the initial in-store experiences will be critical, as bad ones may accelerate a move away from brick-and-mortar stores.

Finally, brands will need to ensure consumers feel safe visiting their stores upon re-opening them. Sanitization, appropriate distancing and other actions will likely remain important for some time.

Read Part 2 of “Affluent Consumers During COVID”.

![[WEBINAR] How American brands can win carts and minds](/sites/default/files/styles/list_item_image/public/ct/publication/2026-06/thumbnail-brand250.png?itok=Qqw2-BEK)

![[WEBINAR] How Visible is Your Brand on ChatGPT, Gemini, and Claude?](/sites/default/files/styles/list_item_image/public/ct/event/2026-07/thumbnail-AI-Visibility-Webinar_0.png?itok=YNe59BFB)