Will our current circumstances increase financial citizenship?

In the early part of the 2010s, Brazil made a concerted effort to increase participation in the financial system. It did this initially by expanding locations. Ultimately, the percentage of financial inclusion increased from 56% in 2011 to 70% in 2017, according to the World Bank’s Global Findex Database. While Brazil’s efforts were successful early on, the impact of more physical locations on inclusion waned in recent years. Kenya, by contrast, has taken a highly technology-driven approach, facilitating peer-to-peer transactions via mobile devices. Financial inclusion has increased from 42% in 2011 to 80% in 2017, according to the World Bank.

While Kenya’s and Brazil’s markets and technology penetration are very different from the U.S.’s, their greater progress suggests that the U.S. needs to facilitate financial technology adoption in order to increase inclusion, which is already at about 93% according to an Ipsos KnowledgePanel survey conducted in February 2020. This is roughly consistent with 2017 figures from the FDIC, suggesting little or no recent change.

During the pandemic, Ipsos has seen greater fintech banking app usage. But affluent consumers are five times more likely to be using these apps than households making under $50,000 a year. So, fintech efforts are largely underrepresenting the most in need.

This need for digital banking is underlined by the fact that the current crisis will almost certainly put more pressure on U.S. banks’ real estate footprints. Banks do have a role in converting cash to digital accounts. Perhaps the increasing focus on inclusion will compel banks to open in communities where they are most needed.

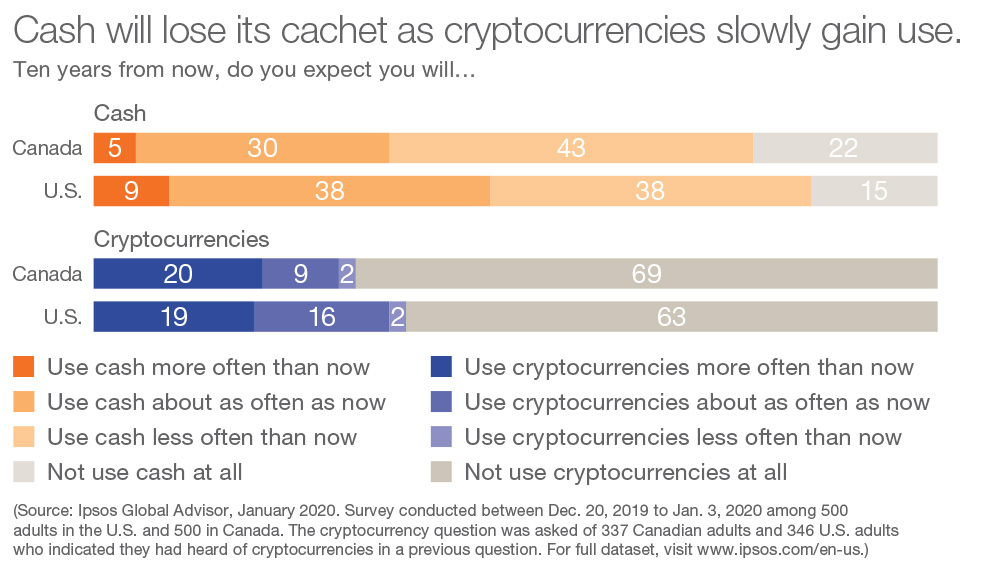

Even with an increase in technology solutions and physical proximity, there is still an issue in getting to 100% inclusion. Consumers are roughly split down the middle in terms of their outlook on using cash in the future. For the 47% who think they will use cash at least as much in the future, reluctance to move to digital is generally chalked up to a lack of trust on the consumer’s part. Understanding these concerns with, and barriers to, digital adoption more granularly will be important in maximizing financial citizenship in the U.S.

The old goal of 100% inclusion in traditional banking might be the wrong marker with the acceleration of digital services. But fintech can likely bridge that to move us toward 100% inclusion in platforms that allow for all populations to save and grow wealth.

To subscribe to our What the Future series, please click here.

![[WEBINAR] Know America at 250: Public Opinion Update](/sites/default/files/styles/list_item_image/public/ct/event/2026-07/250_0.png?itok=LxsH2NfS)

![[WEBINAR] Trust, Values & Growth Audiences: Innovation, Inclusion & Insights](/sites/default/files/styles/list_item_image/public/ct/event/2026-06/thumbnail-templates.png?itok=XcWEzpQn)