The Future of Fintech: Five Key Themes

The new fintech landscape, coupled with continued innovation and evolving consumer expectations, presents a number of significant opportunities as well as particular challenges for product developers and marketers at firms of all sizes. In this paper, we provide a deep dive into five key themes that we expect to impact the world of FinTech in 2021, and potentially beyond, based on our analysis of consumer insights data and recent market trends:

- Digitization gets sticky

- Money in a pinch

- Rebundling the fintech offer

- Educate, don’t gamify

- From Esg to ESG

Want more insights? Revisit our recorded webinar on this topic.

WHAT TO EXPECT IN 2021 IN FINTECH: FIVE THEMES

- Digitization gets sticky

- Money in a pinch

- Rebundling the fintech offer

- Educate, don’t gamify

- From Esg to ESG

The acceleration in adoption of digital financial services and e-commerce during the COVID-19 pandemic has been well-documented. But what is less clear is whether—and how—that will stick as vaccinations increase, the economy re-opens and we head into the new normal. The new fintech landscape, coupled with continued innovation and evolving consumer expectations, presents a number of significant opportunities as well as particular challenges for product developers and marketers at firms of all sizes. In this paper, we will highlight five key themes that we expect to impact the world of FinTech in 2021, and potentially beyond, based on our analysis of consumer insights data and recent market trends. But before we jump in, it is important to ground us in two notable devel-opments after a year of COVID-19.

2020 was another strong year for fintech in the U.S., despite the pandemic

There was heavy fintech funding in the U.S. coming on the heels of an exceptional 2019. Thirteen fintech unicorns, with valuations of more than a billion dollars, were created. And there were several high profile fintechs that went public, including Lemonade, Root Insurance and Affirm. On the consumer side, we saw a dramatic acceleration of digital adoption as we went into pandemic and this was across the board in fintech, with mobile payments, mobile banking, investments as well as lending and financing. In the investing world, we saw dramatic market movement and a change in the mentality of retail investors with the performance of GME, AMC, and Dogecoin. In March 2020 we were just going into lockdown with the COVID pandemic and facing an uncertain future. We ended the year with the first COVID vaccines being authorized and with everybody looking hopefully towards recovery and return to a new normal.

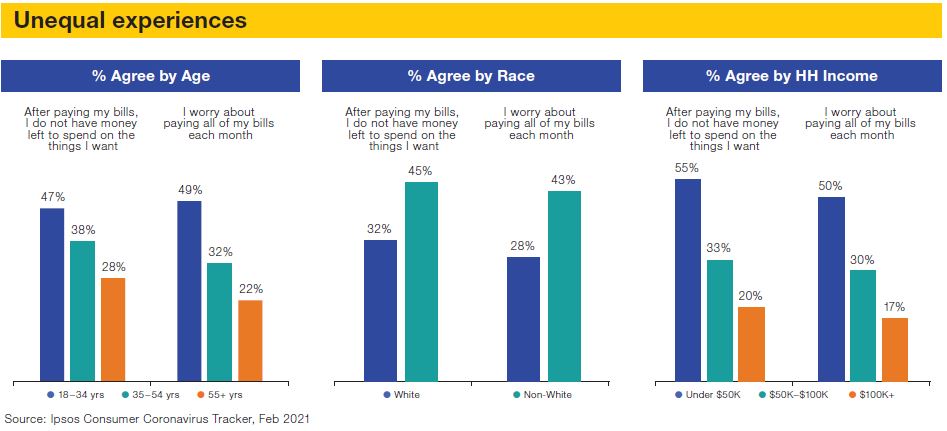

Unequal experience of the COVID-19 pandemic and the K-shaped recovery

One other point to set the stage. There are two very distinct and unequal experiences of the COVID pandemic and its aftermath. Some segments of the population, notably the affluent, did well and saw an increase in wealth and savings, while others faced increased unemployment, reduced savings and heightened financial hardship.

Looking at Ipsos data from February 2021 we see younger folks, lower income segments and people of color disproportionately struggling financially during the pandemic and after.

THE THEMES

1. Digitization Gets Sticky

The pandemic’s lockdowns and restrictions accel-erated—almost forced—adoption of digital financial services, whether that was how we paid for purchases or how we banked.

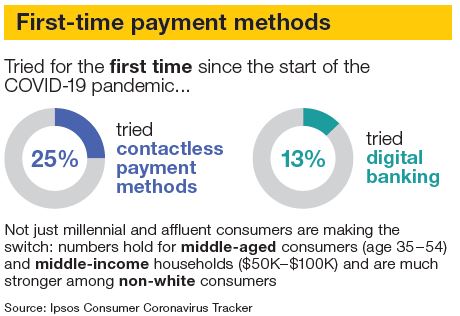

Ipsos data shows that 25% of consumers, since the start of the pandemic, have tried for the first-time contactless payment methods, which include mobile payments/paying with a smartphone, contactless card payments or P2P payments. And 13% have tried digital banking for the first time, whether using their bank’s mobile app or a fintech banking app.

Importantly, it’s not just millennials and affluent consumers who are making the switch to digital. These numbers hold for those 35–54 and those with middle incomes $50K–$100K in HHI and much stronger with people of color. These numbers have steadily ticked up: They were about half as strong last summer and have increased steadily since then. These are dramatic increases in adoption and first-time usage numbers. What banks and payment providers and fintechs have been trying to do for several years with digital adoption has been effectively pushed through in 12 months. The question of course is: will consumers stick with it? Our data says yes. The majority of first-time users of contactless payments and digital banking say they will continue to use these digital financial services post-pandemic. And the numbers on continued usage at least hold steady with segments beyond affluents and millennials and even increase with some segments. As these data on digital adoption show, COVID has actually facilitated financial inclusion in some segments and areas. However, given the K-shaped nature of the recovery, some risks of leaving vulnerable segments behind remain. As the push to digital continues, are we doing enough to not alienate the most vulnerable segments, including the lower income households, older consumers—those who are less tech savvy or have less access to tech? The implication for providers—banks, payments companies, fintechs—is clear. The increased digital adoption is here to stay and providers must be prepared to create superior digital functionality and seamless experiences. The challenge—and the opportunity—for banks and financial services firms is how to ensure that you’re considering the needs of all segments beyond just millennials and afflu-ents. How can financial firms ensure that this shift online draws in those who are currently unbanked, under-banked or less tech-savvy, rather than further alienating them?

2. Money in a Pinch

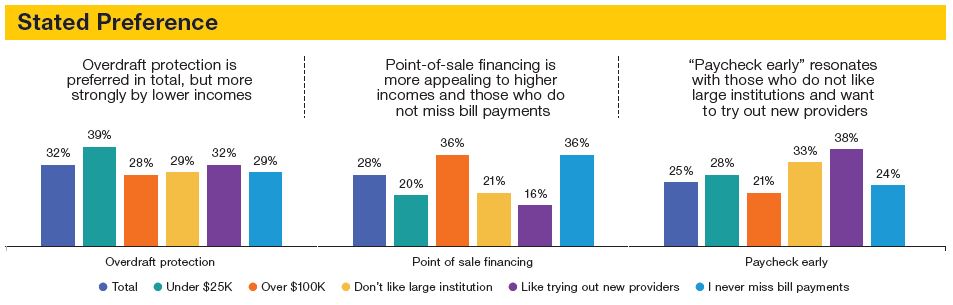

Providers are trying different ways of spotting clients cash when they need some assistance. There are three alternatives to credit cards and small loans we have been tracking. These include Buy Now, Pay Later (or point-of-sale financing), Overdraft Protection (above and beyond low- or no-fee overdraft, e.g. Chime allowing overdraft up to $200), and Paycheck Early (get your paycheck up to 2 days early).

But what do people actually want? And why? Ipsos asked consumers their preference; the results are shown here. What is interesting is the difference in preference based on demographic and attitudinal segments. The overall population prefers overdraft protection. Lower incomes also have a stronger preference for overdraft protection, while higher incomes prefer point-of-sale financing (or buy now, pay later). “Paycheck early” appeals more to those who want to break from the norm—they don’t like financial institutions or to try out new solutions. With that in mind, it’s critical you know your customers and include products designed specifically for them.

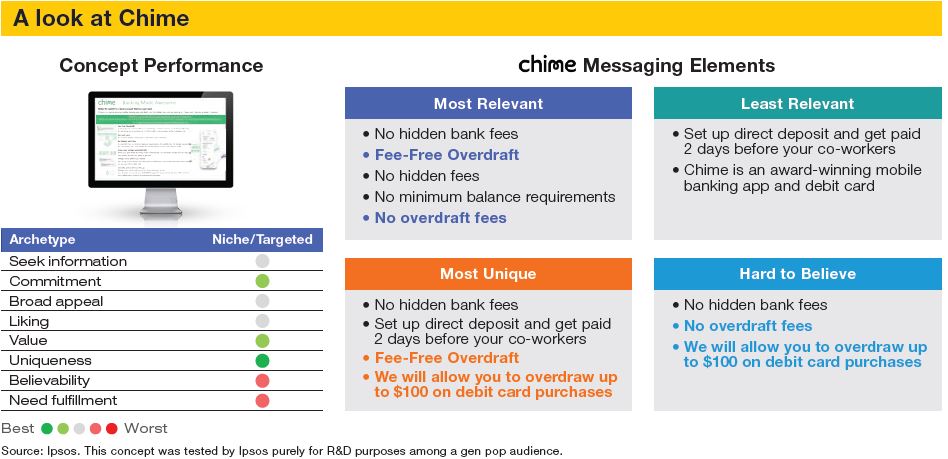

We tested Chime with the Overdraft feature with consumers and they easily picked up on this added benefit. Chime is one of the best at targeting vulnerable consumer segments: they offer both overdraft and “paycheck early.” We’ve tested Chime twice using our validated concept testing approach. We get consumer feedback on key success metrics and compare the scores to our database, indicated by the colored circles below. Based on the pattern of the scores, we can also identify an innovation’s profile; in this case, we see Chime is a niche product, which makes sense as their CEO has specifically said they are only focused on the most vulnerable segments.

What is interesting from our messaging analysis is that the overdraft feature drives interest in the concept.

Like Chime, it’s important to keep vulnerable segments in mind. The vulnerable are likely to be more exposed through the K-shaped recovery, so it’s critical providers understand what features interest which segments and build inclusive products. Some of the innovations may require some risk, but taking that risk can lead to a long term relationship with a client you might have ignored in the past. While we anticipate that services that offer money in a pinch will grow, it will be important for providers to know their consumers’ specific needs, as a one-size-fits all approach will not work here.

3. Rebundling the Fintech Offer

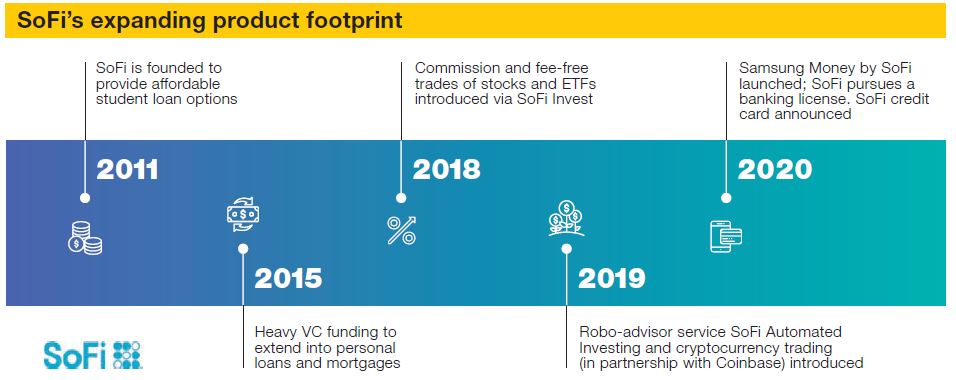

Banks are known for offering a breadth of services. Fintechs, however, typically begin by focusing on a single product or a single underserved segment. Increasingly though, fintechs have started to expand their breadth of services in an effort to deepen customer relationships, challenging banks in the process. A few recent product introductions from fintechs exemplify this trend: Acorns (IRA, checking), Betterment (checking/savings), Square (checking, savings, investing), Chime and Affirm (credit card), and no better example than SoFi.

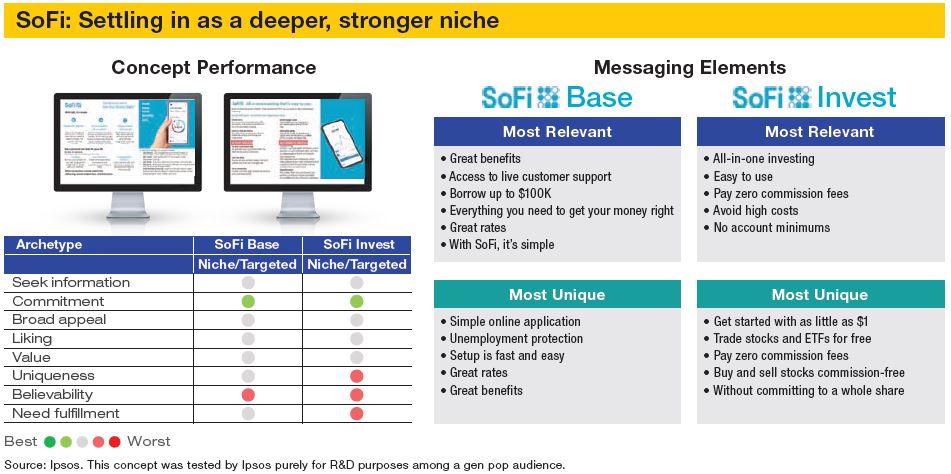

SoFi started in 2011 as a student loan refinancer, expanded into mortgages and personal loans, then offered investing services with SoFi Invest and SoFi Automated Investing. Most recently, SoFi launched the Apple Pay-equivalent Samsung Money by SoFi. In addition, SoFi continues to pursue a banking license and has also just announced a credit card. We tested the base SoFi offer, with heavy emphasis on loans, as well as the SoFi Invest offer.

Looking at the scores on consumer demand KPIs, we see strong commitment for both SoFi and SoFi Invest with moderate broad appeal, indicating a niche/targeted innovation profile. By introducing SoFi Invest, you might think that SoFi is going after a broader audience, but the focus is on deepening existing customer relationships. SoFi Invest is also a niche product, so SoFi is going after the same audience. The benefits of SoFi Invest that resonate include commission-free trading, low costs and ease of use. These are aligned with the base SoFi offer and seek to reinforce and strengthen the brand as SoFi seeks to become a one-stop shop for financial services for specific population segments. Continue to expect the unexpected in fintech competition. As fintechs broaden their services and deepen customer relationships, they pose a bigger threat to banks as they advance further into their territory. When SoFi focused on student loan refinancing, it may not have mattered as much, but with the expansion of their product footprint, they are a greater threat. We expect fintechs to continue to successfully expand their footprint of services, meaning banks and payment providers should continue to expect the unexpected from their fintech competition and be willing to pursue segments and/or defend niches before fintech advances.

4. Educate, Don’t Gamify

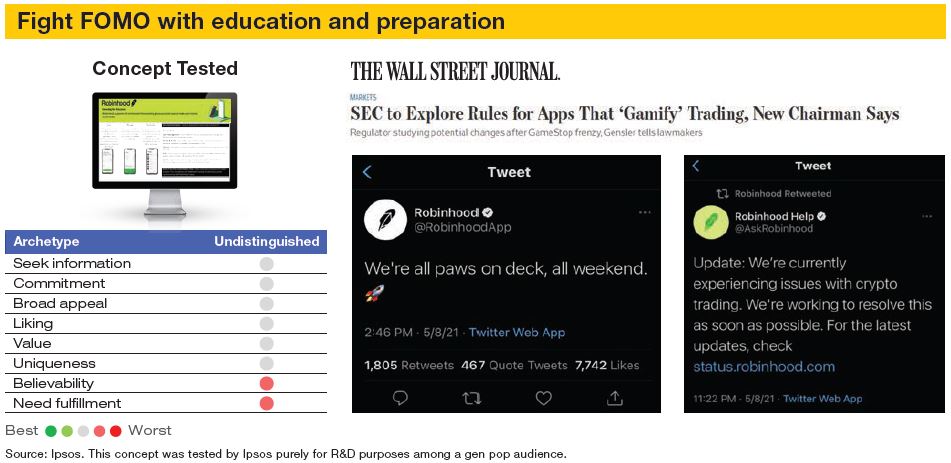

It’s hard to think about 2020 and the environment going forward without touching on investing. It was truly a roller coaster year. There was a quick recovery after a sharp market drop, but much of this was due to an unpreceden-ted circumstance. For one, the federal reserve held rates low and bought back bonds to support the market and everyday investors were more active due to no commission trading, added stimulus, and general boredom. While the market recovery is good, it has changed many investors thoughts on general investing. Much of the activity was fueled by low-cost solutions such as Robinhood. Robinhood and similar solutions typically offer little if any advice/education materials and may even gamify the platform to push clients to be active through gamification. Consumers’ thoughts of Robinhood have changed along with perceptions of the general market. We tested Robinhood with consumers and we see it’s undistinguished and no longer seen as unique. We’ve seen additional push back from regulators and from consumers on trust after some suspicious trading pauses while the likes of AMC and Doge corrected. These market conditions and push back against fintechs creates an opening for traditional providers.

Traditional firms can capitalize on the conditions by using education as a differentiator. Anyone who was investing could have made money in 2020, but that is unlikely to be the case going forward, especially given the focus on individual stock/securities that has dominated headlines recently. The less financially literate are especially exposed and could be left behind. Providers must keep them in mind when designing solutions. We anticipate that providers that prepare their clients and set them up to thrive if a correction or individual equity sinks in value will establish a platform for continued work and ultimately benefit over players pushing a more gamified approach to investment.

5. From Esg to ESG

When it comes to ESG (Environmental, Social, and Governance criteria), financial services firms and fintechs have focused on environmental impact for a while now, as evidenced by the examples below:

- Banking—Aspiration is a digital bank that won’t use consumer deposits to fund fossil fuel projects.

- Payments—Doconomy, a Swedish digital bank focused on reducing unsustainable consumption and carbon emissions, introduced a credit card with a CO2 cap on spending, effectively a credit card that monitors purchases by their carbon emissions—and puts a cap on spending based on a user’s impact on the climate.

- Investments—Betterment, Personal Capital and others have ESG investing options that primarily focus on environmental impacts and avoiding investments in companies directly or indirectly involved in fossil fuel projects.

However, we expect financial products that directly and indirectly support issues beyond the environ-ment will resonate in 2021.

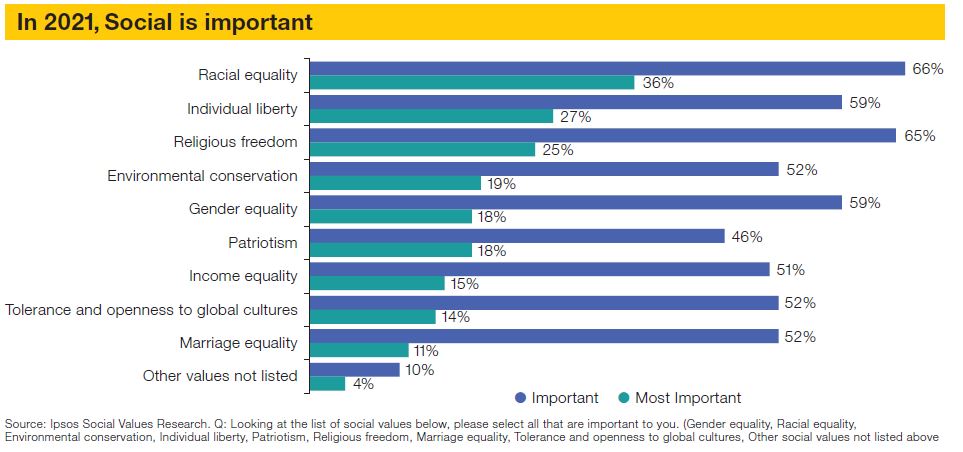

Ipsos data shows that consumers do care about the environment, but they care as much and more about many social issues—racial equality, gender equality, income equality, etc. And that cannot be ignored. In fact, brands/companies/providers are expected to take a stance on social issues, according to Ipsos research on the financial sector. As we saw earlier, people of color and lower-income consumers continue to feel pandemic effects disproportionately. Providers should emphasize financial inclusion of these most vulnerable segments and build financial products, services and functionality that support them.

In addition, when we asked consumers who they most trusted to protect their financial data—banks, fintechs, big tech or the government. A lot of consumers chose “none of the above,” mirroring the increasing lack of trust in institutions. But among the others, banks were most trusted. Fintechs and Big Tech much less so. As fintechs navigate thorny data ownership questions—especially in cases where they have banking as a service partnership—they face a data governance challenge to gain trust, while banks have an edge. Fintechs, especially private fintechs, have often skated by without much attention from regulators. But if the Wirecard debacle in the UK taught us anything, it is that fintechs are going to be increasingly scrutinized by regulators, investors and consumers. Again, banks have the edge here, having already had to comply with greater regulations and historical emphasis on governance issues. When it comes to ESG, we expect to see companies whose services move beyond the E to encompass the S and G gain an upper hand in 2021.

WHAT’S NEXT

- We expect a K-shaped recovery which will increase the distance between segments, whether that’s the non-tech savvy, lower incomes, ethnic groups or those who are less financially literate.

- It is critical that providers offer products that reduce alienation and consider the non-tech savvy.

- Consumers make product decisions on more than just feature sets and pricing—there is a heightened focus on key issues, meaning brands, companies and products that recog-nize all of ESG—Environmental, Social, and Governance—will resonate more strongly.

![[WEBINAR] The Modern Twenty-Something: How Gen Z Thinks About Money, Milestones, and More](/sites/default/files/styles/list_item_image/public/ct/event/2026-07/thumbnail-templates_0.png?itok=GNEHIkP1)