Here’s what it takes to attract early adopters in 2022

Early Adopters represent an important market segment for most brands. In our latest paper, we offer a deep dive into the hearts and minds of Early Adopters: who are they; what do they expect from brands; where do they shop; what makes them tick? Read more about how to connect with these consumers, while keeping in mind that:

- Early Adopters in the U.S. are just as worried about inflation as the rest of the country— so businesses should focus on new products that innovate to meet their needs

- Early Adopters are most firm in wanting brands to match their values, whether that means supporting their community, producing with more sustainable practices, or aligning to their view on equality

- Beyond having the latest and greatest, Early Adopters want to be in the know and not buy blindly

KEY FINDINGS:

- Early adopters in the U.S. are just as worried about inflation as the rest of the country—so businesses should focus on new products that innovate to meet their needs

- Early adopters are most firm in wanting brands to match their values, whether that means supporting their community, producing with more sustainable practices, or aligning to their view on equality

- Beyond having the latest and greatest, early adopters want to be in the know and not buy blindly

It’s hard to get a new product to stick, but for businesses trying to create something new or ensure their brand stays relevant, it’s incredibly important to reach a group of consumers who are more willing than average to try new things—a group known as early adopters.

The theory of early adopters (and the adoption curve) is relatively straightforward—a certain group of consumers (the aforementioned early adopters) will be the first to try new products or enter emerging categories, followed by the early majority and late majority, with laggards finally deciding to buy or subscribe only after others have taken the leap. These early adopters represent the cutting edge: They’re willing to take a risk and try new things, and they’re engaged in a way others are not.

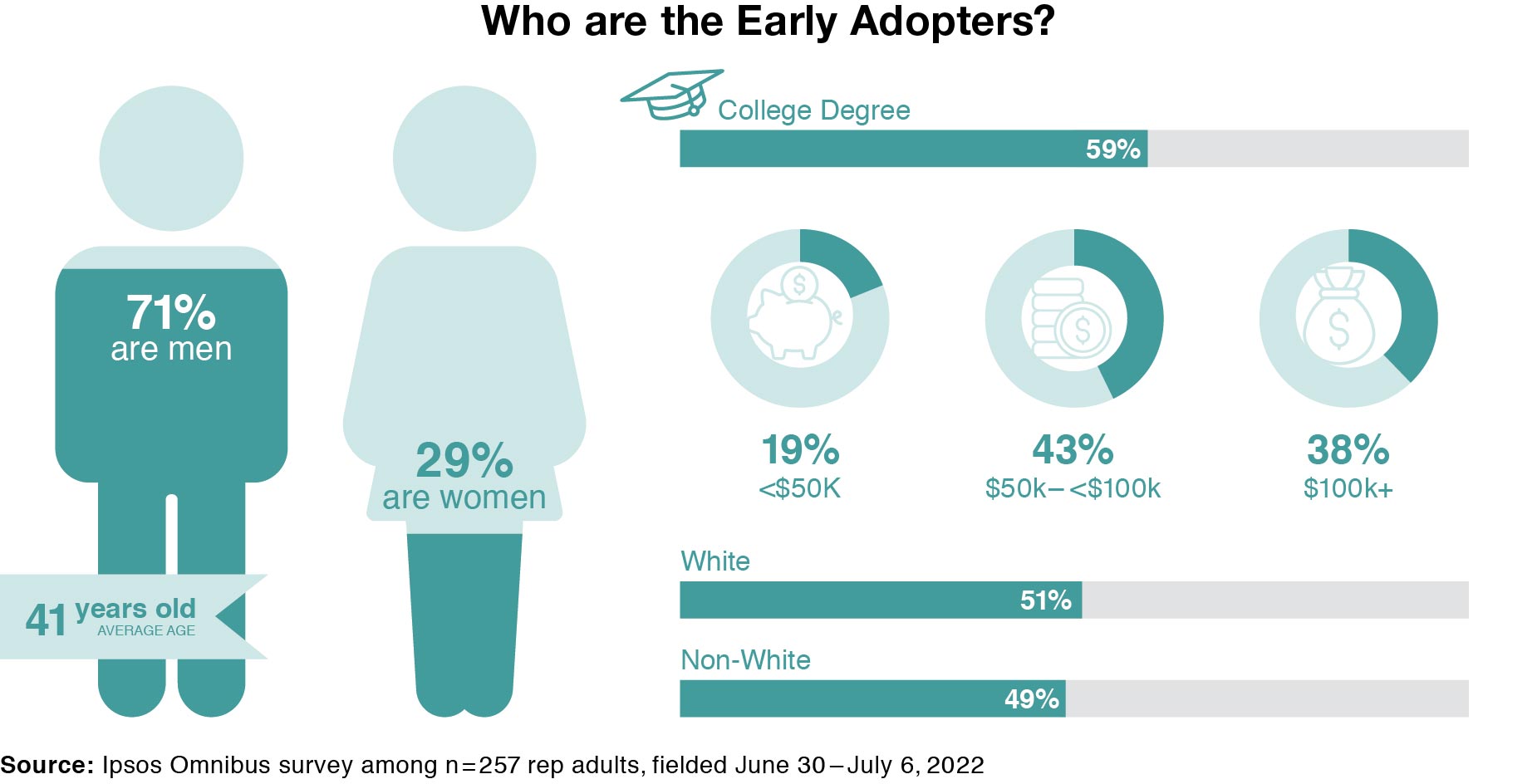

Businesses typically target early adopters when developing innovative solutions with the understanding that appealing to this audience can gain traction among more sizeable early and late majority consumer groups that represent the majority of the market. And the profiles of these early adopters typically lean toward the more affluent and more risk-tolerant consumer who has the means and willingness to give new things a try.

So how do we identify early adopters in a reliable, accurate way at a broader scale—and what do they think about the topics driving consumer conversations today?

In this piece we propose a new framework for how to identify early adopters that goes beyond consumers telling us where they think they sit on the adoption curve. With this framework in mind, we examine who these early adopters are, how they learn and shop, and what they own and use today. We also take a look at their brand expectations and attitudes as well as their views on inflation—important dynamics at play in today’s market that will shape how brands approach new product development and marketing initiatives.

What makes an early adopter?

When taking a broader view of the market, it’s impossible to identify early adopters based on purchase behavior alone, as important of a characteristic it may be.

One method is relying on self-identification—does the consumer believe they tend to be among the first to try new products?—but leaning on people accurately comparing themselves to others can be perilous. Another method is measuring attitudes, such as interest in switching brands versus staying with the tried-and-true, or if they enjoy taking chances when buying new products; but again, this alone can be problematic, as it may not reflect actual purchase behavior that traditionally defines the adoption curve.

To combat these effects, we’ve taken the approach of overlaying both self-identification along with attitudes, giving us a more nuanced understanding of who is early to buy, and the result of this approach approximates the distribution of the theoretical adoption bell curve.

Even early adopters are worried about inflation

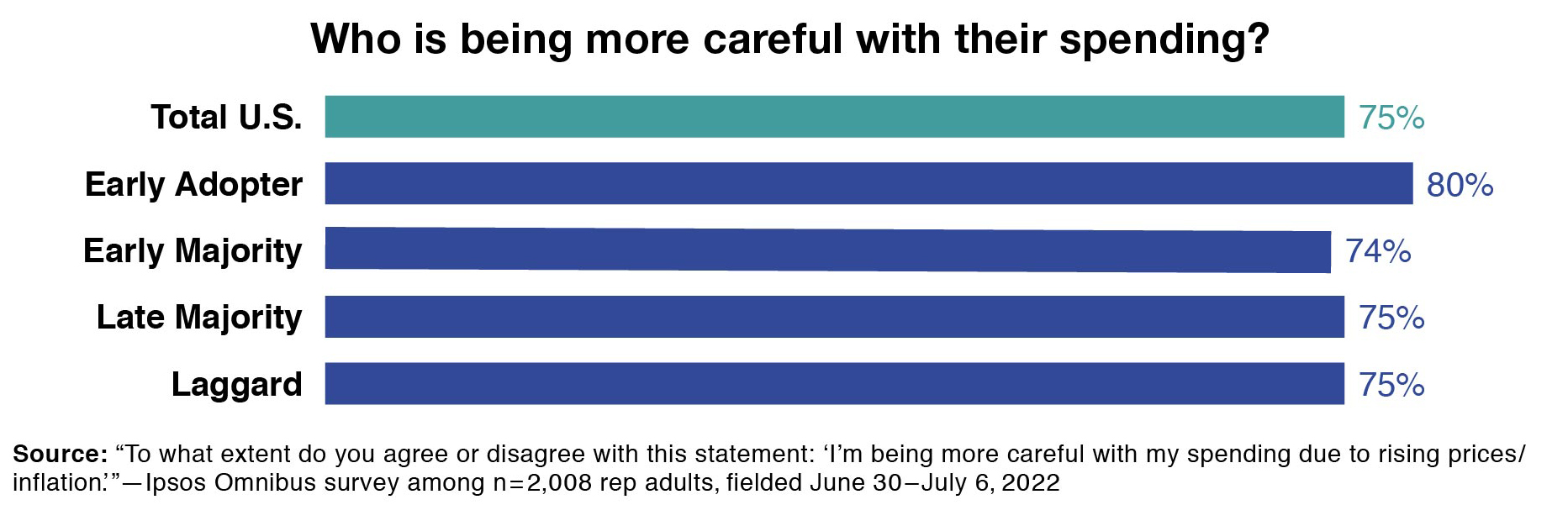

Grappling with the reality of inflation is inescapable: Price increases are being felt by consumers across America, even if they would prefer to live under a rock and avoid the seemingly constant media attention. Despite being willing to take chances, and sporting higher incomes, early adopters are just as worried as the rest of the country about the impact inflation has on their bank account—80% agree they are being more careful with their spending due to rising prices/inflation, compared to 75% of the country as a whole.

But this doesn’t mean they will withhold spending altogether, or that brands should be playing defense; early adopters are naturally more open to trying new things, and brands should focus on proactively innovating to meet their needs and focus on providing (and communicating) new sources of value.

Speaking with spend

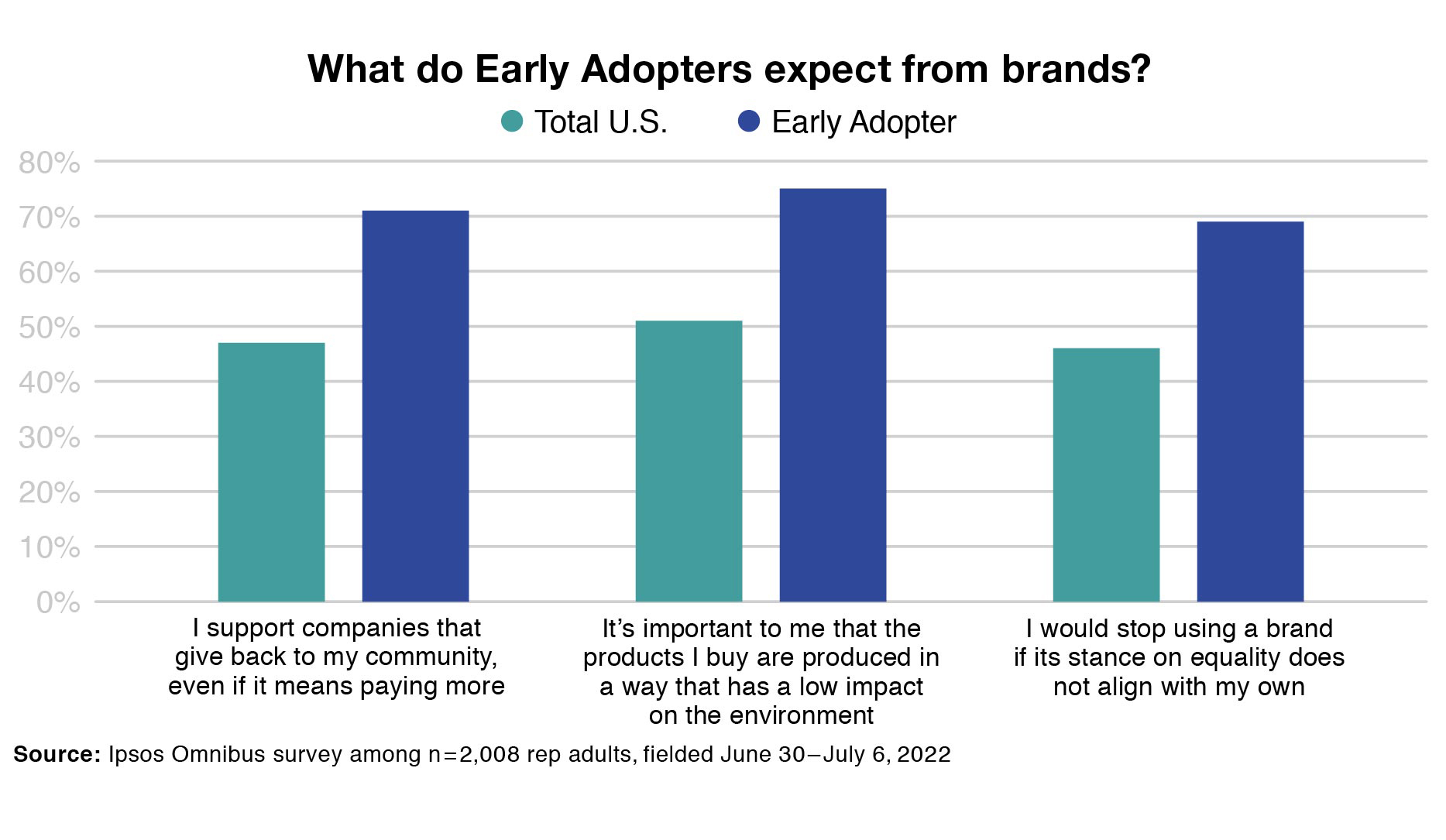

Early adopters are most firm in wanting brands to match their values; be it supporting their community, producing with more sustainable practices, or aligning to their view on equality, early adopters are far more interested than most in speaking with their wallets, and have the luxury of doing so. Less engaged consumers are less focused on brand values and sustainability as of now, potentially more focused on budgets and just getting the most functionality they can as prices rise—but the early majority also leans towards wanting brands to take a stand, and this larger and relatively affluent group still can help drive sales and cannot be discounted.

Seeking out, not sitting around

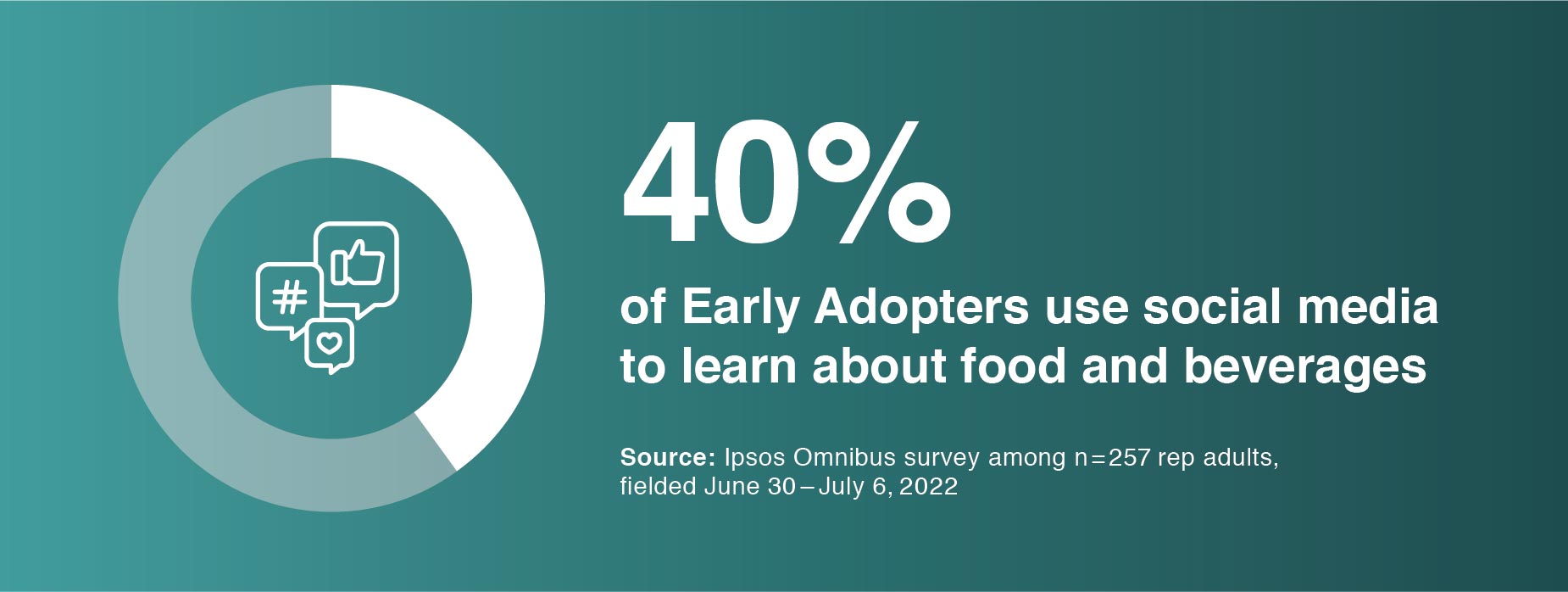

Early adopters are fully engaged and actively seeking out information about new products, using sources like social media and YouTube, but also going straight to a brand’s homepage or product reviews for product details. This information-seeking behavior is not isolated to just one category either, early adopters are doing online research for everything from smartphones to food/beverage and household cleaning products. Beyond having the latest and greatest, early adopters want to be in the know, and they play an important role in vetting new products for early majority and late majority segments who rely on their opinions to navigate their way into the market.

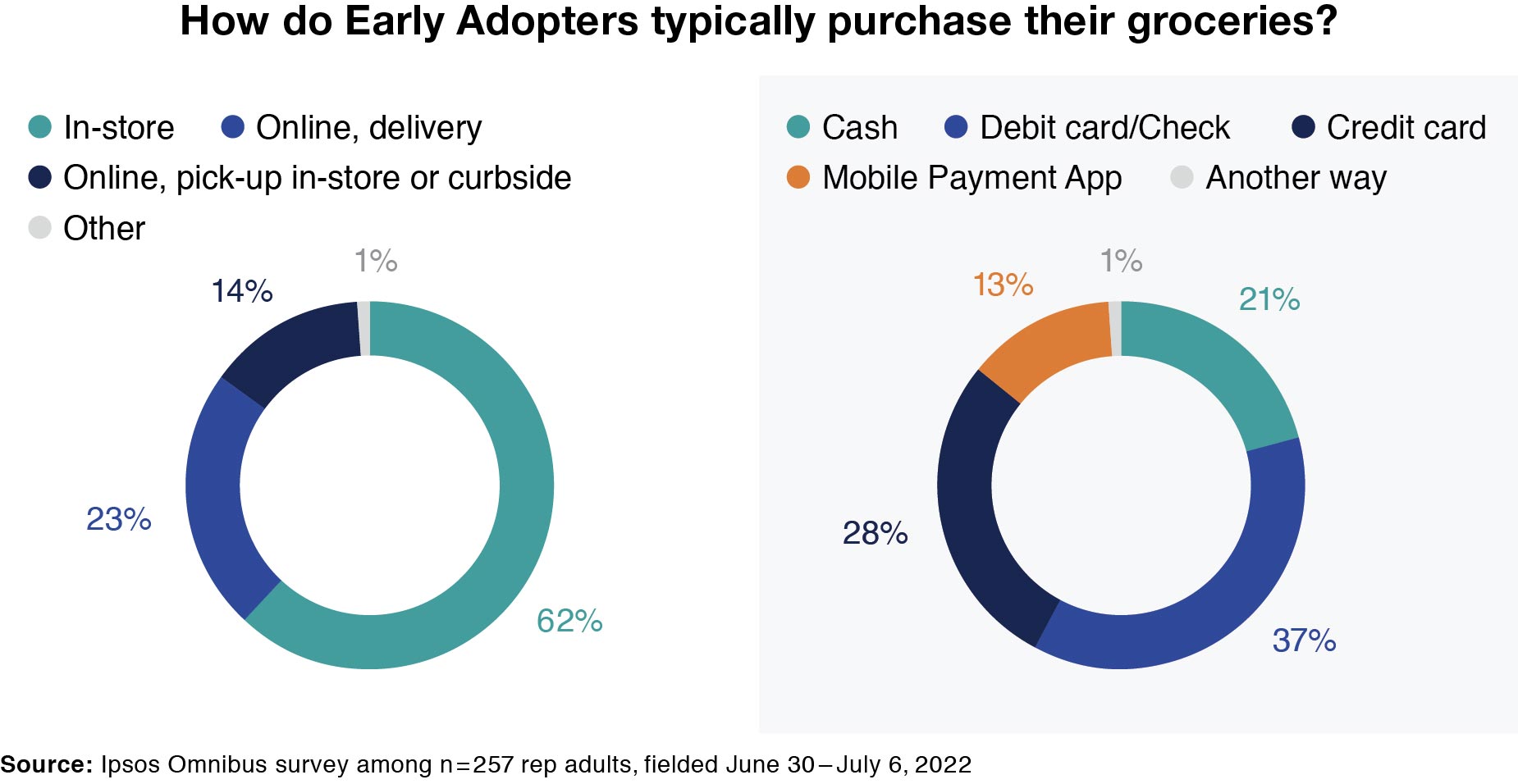

In-store still favored for everyday

While early adopters are more likely to take their shopping occasions online overall, in-store shopping still reigns supreme for everyday items like groceries and over-the-counter medications. Even a hybrid solution like buy online, pick-up in-store is still in its early days within the grocery category among early adopters, despite any shifts toward contactless shopping that might have happened over the course of the pandemic.

Speaking of contactless, despite more in-store shopping happening among early adopters regardless of category, credit and debit payments remain the preferred payment method for early adopters (and all adopter segments). Even with the accelerated move to digital banking over the course of the COVID-19 pandemic, mobile payments are not yet the preferred method for purchasing for these cutting-edge consumers.

Crypto-curious and VR-voracious

In the tech and finance worlds, two key topics drive conversation these days: the metaverse and virtual reality, and cryptocurrency. While these trends have been around for a few years, they are still in their relative infancy and are largely reliant on early adopters to drive uptake and interest. Early adopters are nearly three times more likely than the general population to own a VR headset (29% vs 10%), and two times more likely to already own cryptocurrency (29% vs 14%). And it’s not just laggards who have yet to buy into both ecosystems—the late majority still don’t make up their fair share of owners, either.

But the same cannot be said of internet connected devices like smart TVs, smart home speakers/displays, or smart doorbells. The late majority have been catching up and purchasing these connected products, waiting mostly now for laggards to catch on and drive further penetration.

These products illustrate an important dilemma for brands and marketers: While not all early adopters or early majority own today, is potential for current solutions somewhat limited if the idea has largely been accepted across groups? How do you grow beyond your current share if even the late majority or laggards catch up? What’s next in order to drive more adoption or stickiness among the early, and then driving further conversion across the curve?

Ask yourself: Who are your early adopters, and how are you creating for them?

While we have included the lens of attitudes and mindsets to help define early adopters on a broad scale, this key group can vary by category; for example, a consumer may be interested in staying up to date with the latest and greatest tech products, but is not adventurous or a risk taker when they buy groceries, preferring to stick with what they know. Early adopters, as convenient as it would be otherwise, are not a monolith—brands and marketers need to deeply understand who in their categories are on the cutting edge and who are willing to take risks (and who is more likely to switch), and why.

WHAT’S NEXT:

- While broader market knowledge is undoubtedly important, brands that deeply understand their early adopters have a built-in advantage: These brands can understand if modifications of positioning, messaging, or product are hitting the mark among an audience more accepting of change, even if their larger customer base takes some time to catch up.

- Even in inflationary times, there’s room for innovation; consumers are more attuned as prices rise, no longer able to rely on what may have been assumed to be baked-in buying habits and are now looking for solutions that match the moment.

- While this may seem like a time to play defense, it’s quite the opposite, and Early Adopters are naturally on the lookout for what’s next. Understanding what they care about in each category and meeting their needs in this inflection moment could result in new users and even new advocates long term.

![[WEBINAR] Cracking the Nutritional Supplement Market](/sites/default/files/styles/list_item_image/public/ct/event/2026-05/thumbnail-cracking-nutritional-supplement.png?itok=Cts0kD4T)