How can financial providers assist in the big wealth transfer?

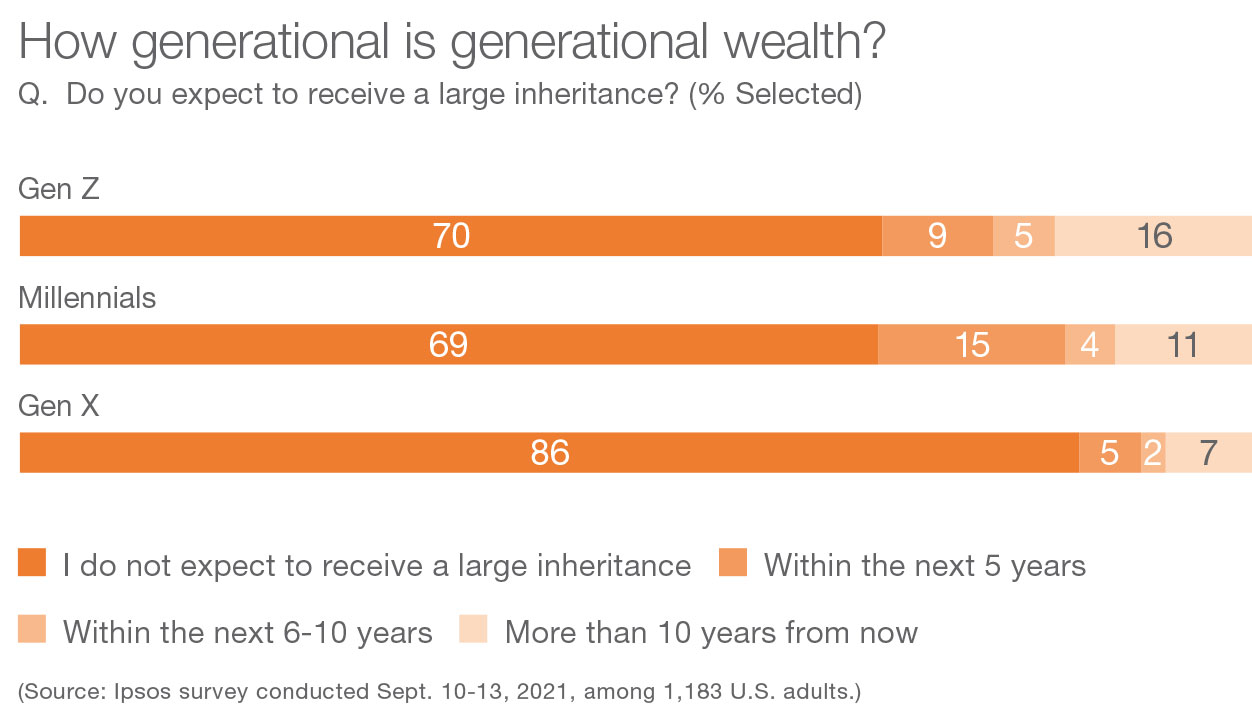

Americans age 70 and older have stockpiled more than $35 trillion, more than a quarter of all U.S. wealth, according to the Federal Reserve. This will lead—and, sadly, COVID-19 accelerated this—to an unprecedented transfer of wealth over the coming years.

The competition to help consumers across generations to manage and grow wealth is as heated as ever due to digital innovation. However, wealth transfer relies on a service orientation that’s decidedly analog even as the offerings are increasingly digitally enabled.

Wealth transfer is a highly emotional topic, and decisions made under the duress of a death can be costly. There’s a growing need for financial services to help customers from multiple generations navigate the situation. Providers do a good job educating on such universal topics as will creation, updating beneficiaries and life insurance. Yet today’s families must work through additional digitally oriented challenges like gaining access or passwords to a deceased family member’s accounts and smartphone.

This creates an opportunity for financial providers to be a trusted, neutral resource where uncomfortable conversations and vital information-sharing can occur asynchronously over years, and then only become accessible when a person suddenly passes away.

The pandemic has created an urgency and an opportunity to broach this kind of planning with loved ones. Financial services providers could market these services in tandem with investing and savings advice.

On one hand, the existing and often long-standing relationships with the older generation position traditional financial services well to innovate and build out concierge services. Their teams can handle wealth management to legal and accounting services to tech support for surviving family members.

On the other hand, younger generations might look to newer financial technology startups. Some new investors will seek fintech-driven value propositions like no-commission trading, no account minimums and even opportunities to buy fractional shares. For investors who want more guidance, other companies offer low-effort automated investment options as well as robo-advising. Established providers are quickly catching up to offer services to cover the entire spectrum of investors from self-directed, to robo-advising, to traditional financial advisor client services.

Regardless of the service, financial brands can position their services as the much-needed neutral provider who can take the emotion out of financial decisions that will shape their clients’ futures.

This article was originally published in What the Future Wealth, a research magazine by Ipsos highlighting Americans’ unique view of wealth and the influence that digital, diversity and the Great Wealth Transfer will have on how we pass, share, spend and invest it. Download the magazine here.

![[WEBINAR] What the Future: Success](/sites/default/files/styles/list_item_image/public/ct/event/2026-07/thumbnail-wtf-success-.png?itok=3mnYDE70)

![[WEBINAR] 2026 KEYS: The Frontiers of Brand Trust](/sites/default/files/styles/list_item_image/public/ct/event/2026-06/thumbnail-keys-0709_.png?itok=Z3yGpXTY)

![[WEBINAR] Ipsos Global Influentials: In Their Own Words](/sites/default/files/styles/list_item_image/public/ct/event/2026-06/thumbnail-templates_0.png?itok=cHr4zS5w)