Painless payments aren’t without downsides

When people pay for something, the same sections of their brain responsible for registering emotional and physical pain are more active, a 2017 study at the University of Toronto found using functional MRI. However, some payments hurt more than others. One of the biggest contributors to what scientists observed in a Journal of Consumer Research paper as “payment pain” is how much “friction” the payment type produces. This is due not only to the form of the payment—where people may have to physically count the money or calculate the number to put on a check versus swiping a credit card—but also to the delay in receiving the good and actually paying for the item.

Decreasing friction makes the process quicker and easier for the shopper. It also focuses their thoughts on the benefits (vs. costs) of their purchases, per a separate study published in the Journal of Consumer Research. Counterintuitively, even though they obtain their purchases more quickly, doing so actually causes them to feel like they own the item “less.” This potentially shrinks the value shoppers feel they get from their purchases.

Other work provides clues about issues unique to lending, some relating to our lay beliefs about service quality and the length of service encounters. One study found that when shoppers perceive that a service takes longer due to the effort involved, they rate the service as more valuable to their lives.

Therefore, lenders offering frictionless applications and availability may suffer from perceptions that they are not high-quality lenders or that the terms and conditions of their offers may be substandard to competitors who have more steps to lending or who just take longer to approve applications.

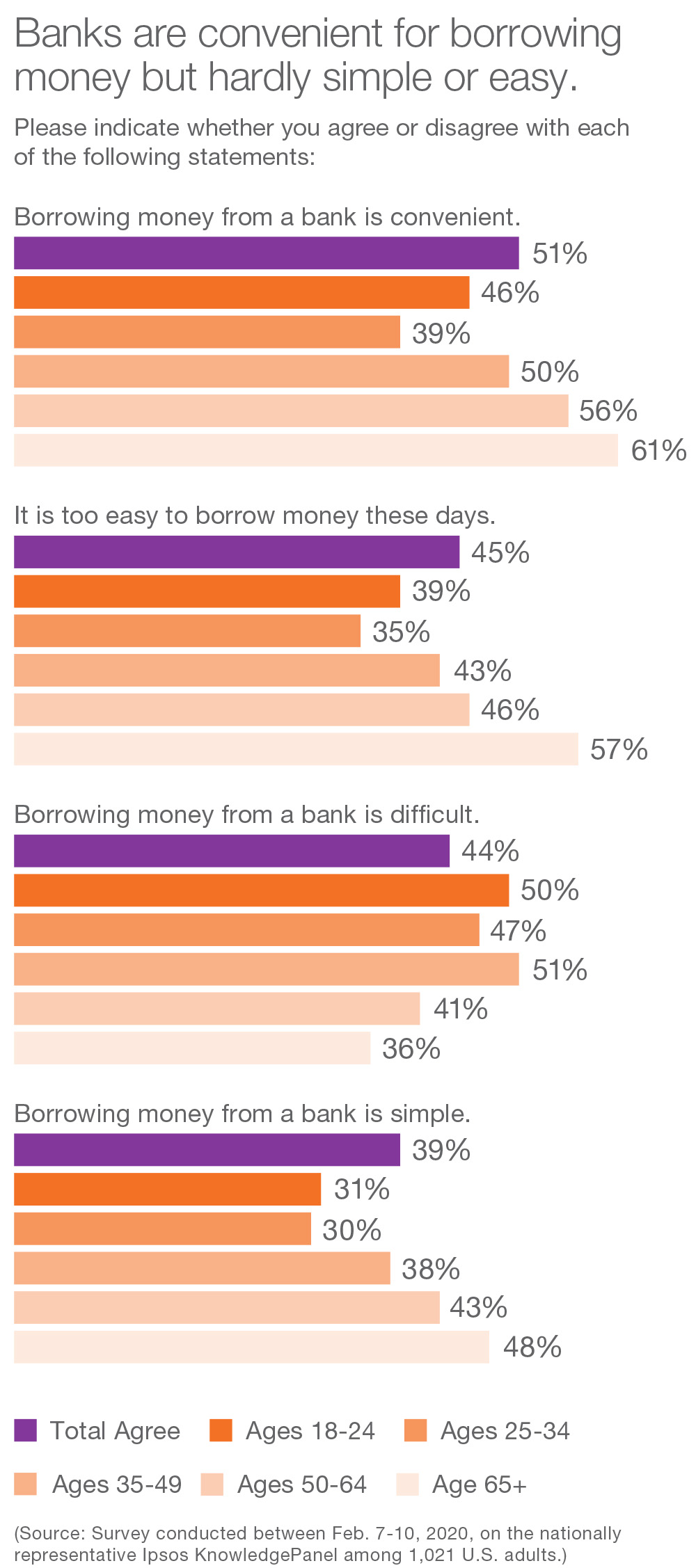

This may explain why while half of Americans find it convenient to borrow money from banks, fewer find it simple (39%) or quick (3%), per a February Ipsos KnowledgePanel survey. Despite new offerings to ease borrowing, Americans are split on whether it’s too easy to borrow money today.

While anything in our fast-paced society that decreases friction and pain provides relevant and important benefits to shoppers, it’s critical to be aware of the impact on their perceived and actual financial well-being and the potentially negative influence on their perceptions of brands.

To subscribe to our What the Future series, please click here.

![[WEBINAR] Here’s how Influential audiences differ across segments](/sites/default/files/styles/list_item_image/public/ct/event/2026-04/thumbnail-templates_1.png?itok=8UDJ-jMz)