UK public still broadly supports most net zero policies

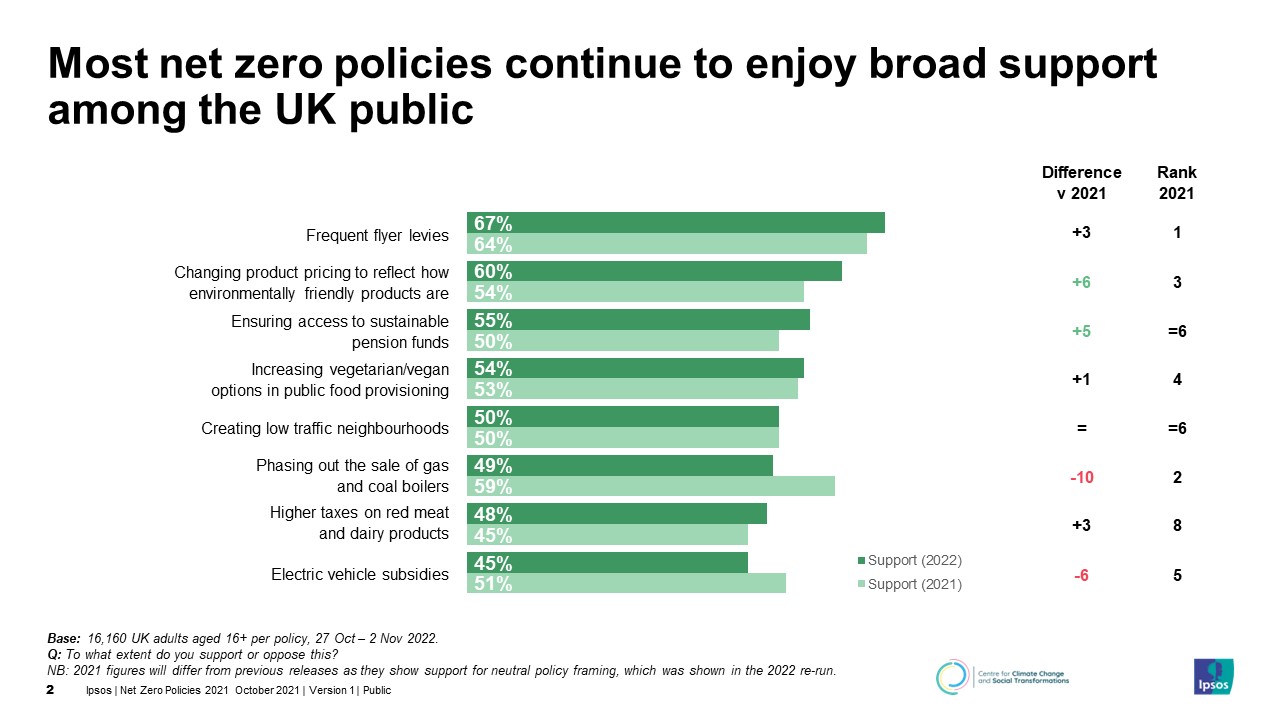

The majority of people in the UK continue to support most Net Zero policies in October 2022, with some enjoying even higher support than in August 2021. New Net Zero Living data released by Ipsos and the Centre for Climate Change and Social Transformation (CAST) shows similar policies continue to enjoy higher levels of support even as the cost of living crisis begins to bite, such as frequent flyer levies and changing product pricing to reflect how environmentally friendly they are. While both would entail a greater financial outlay for people – such as by paying more to fly or for certain types of products – perceived fairness and an ability to avoid financial impacts (for example by going abroad on holiday less) may be more important for public support.

However, two previously popular policies have significantly lower levels of support in 2022, namely phasing out the sale of gas and coal boilers and electric vehicle subsidies. This might reflect top-of-mind concerns among the public around the increasing price of energy and fuel, as well as seeking to avoid large purchases as the cost of living rises. Seasonality may also be a factor at play in the falling support for phasing out coal and gas boilers, with people being much more aware of home heating costs now than in summer 2021.

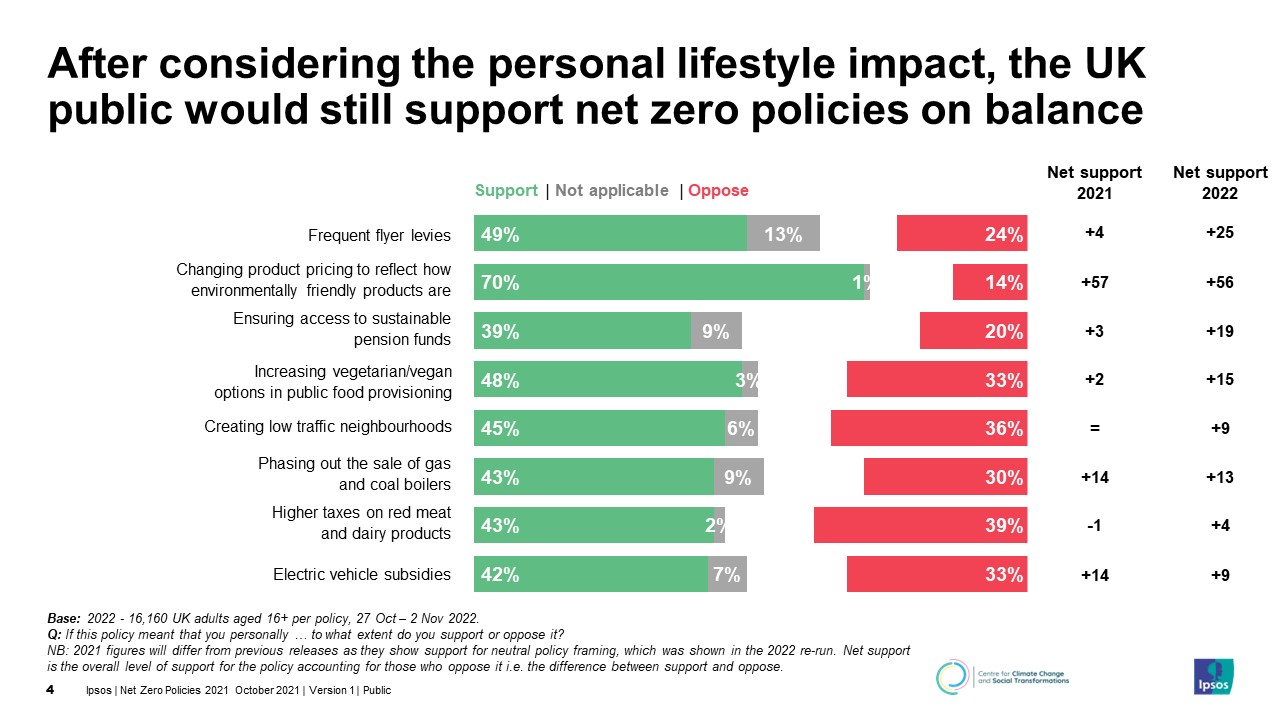

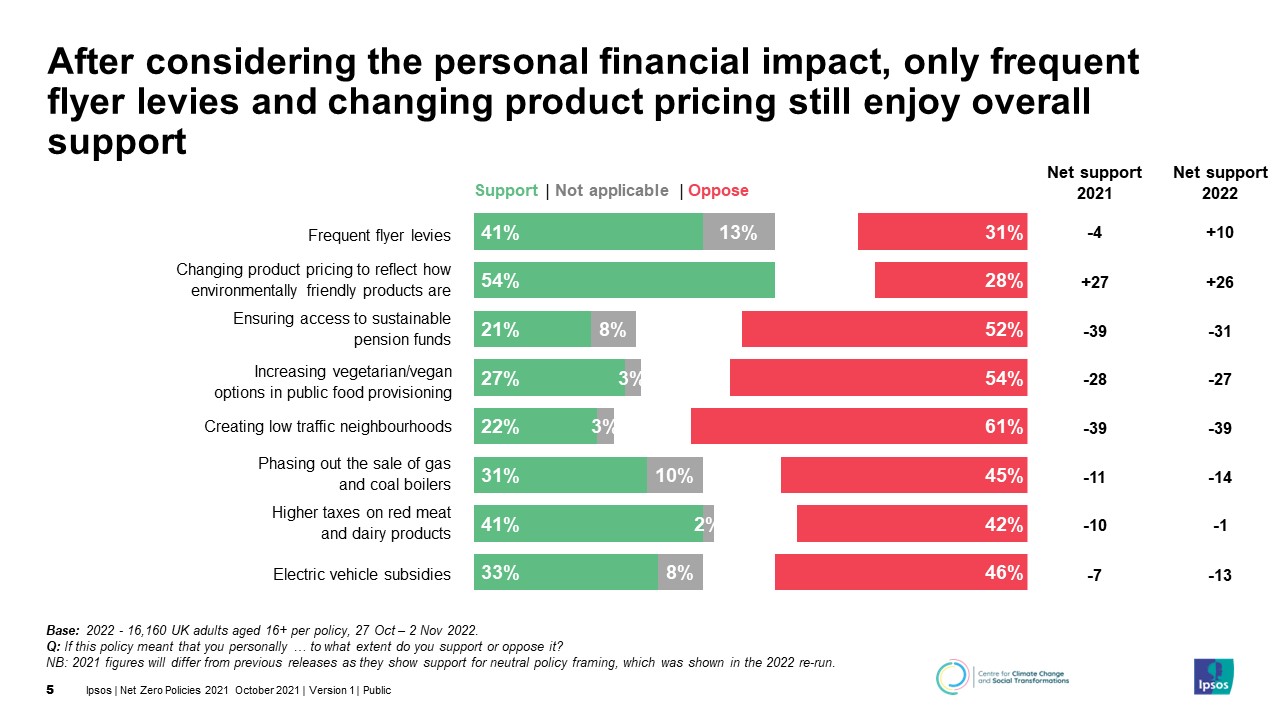

As in 2021, we tested whether support for net zero policies falls when people consider the personal lifestyle and financial trade-offs. While support for net zero policies still falls when these trade-offs are introduced, this generally has a smaller impact on policy support overall in 2022. This may be because the cost of living is at the forefront of people’s minds, so they are already factoring in financial costs when initially considering the policies. However, the personal financial cost of net zero policies does have a greater additional negative impact on policy support after the public have already considered a policy’s lifestyle impacts, making up a greater proportion of the overall drop in support than it did in 2021. Again, this likely reflects increasing concerns about the cost of living.

Who in the UK supports net zero policies?

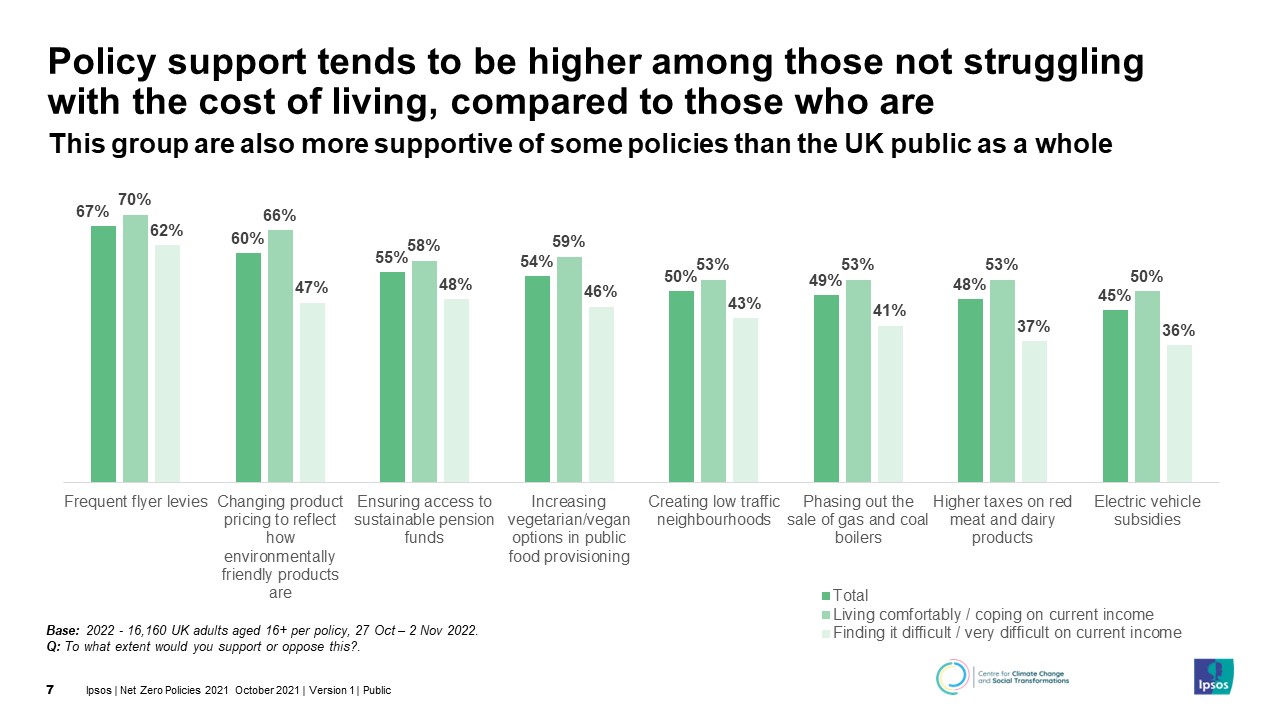

Initial policy support is higher among similar groups as when we initially ran the Net Zero Living research in 2021. This includes people educated to degree level or higher, those from more affluent households or parts of the country such as London and the South East, those on the left of the political spectrum, and those who are more concerned about climate change. Support is also higher among those who are not significantly impacted by the rising cost of living (those who say they are living comfortably or coping on their current income) compared to those who are.

While there are no consistent differences in support between age groups, some policies are favoured by younger or older members of the public. As in 2021, older people tend to be supportive of creating low traffic neighbourhoods, frequent flyer levies and changing product pricing. On the other hand, younger people remain more supportive of EV subsidies, phasing out the sale of coal and gas boilers, as well as ensuring access to sustainable pensions.

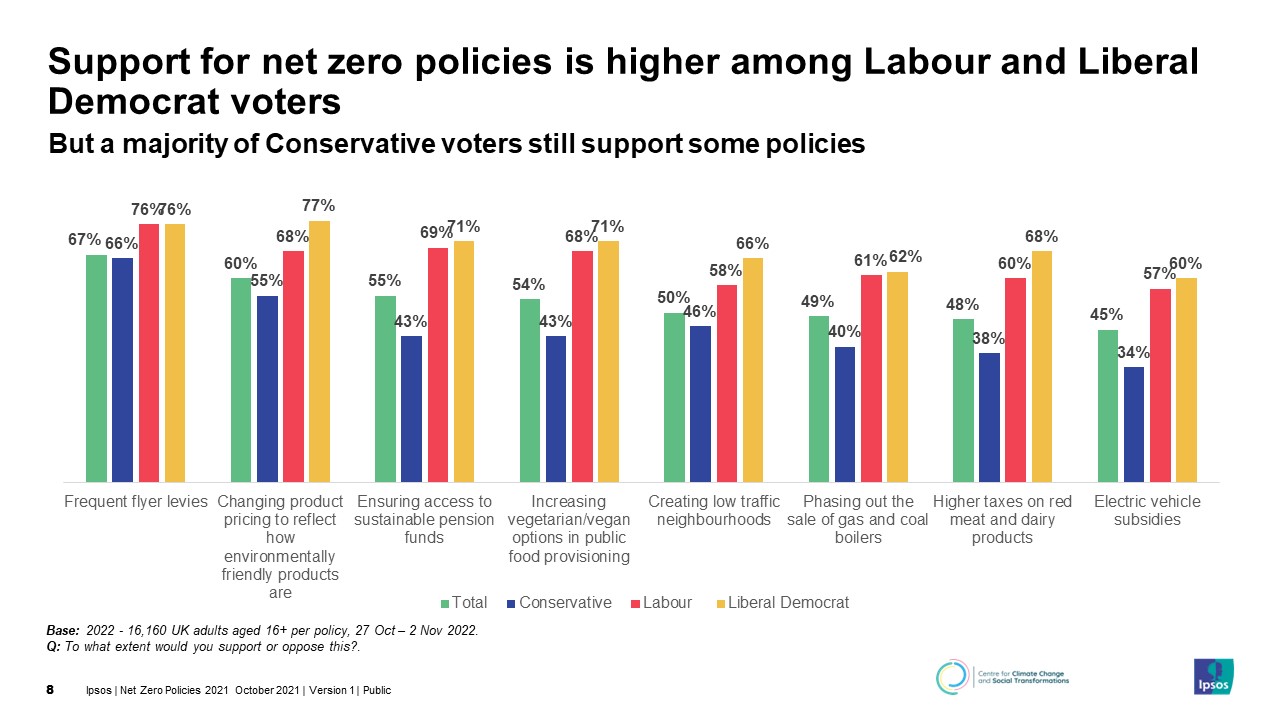

Political affiliation continues to shape policy support too. Those who voted for Labour or the Liberal Democrats at the last general election are consistently more supportive of net zero policies than those who voted for the Conservatives, including after seeing the lifestyle and financial trade-offs. However, there is majority support for frequent flyer levies and changing product pricing across voters, and most Conservative, Labour and Liberal Democrat voters remain supportive of changing product pricing even after seeing the personal trade-offs.

Public support for net zero policies has remained buoyant in the UK, despite the rising cost of living which we might expect to have a greater negative impact on policy support, particularly where these have cost impacts. Yet policymakers must not lose sight the importance of personal cost – particularly financial impacts – as we head into this difficult winter. They still need to engage with public concerns around the cost of net zero policies when communicating about them and associated sustainable behaviour change. Broader Ipsos research shows people are increasingly worried about the cost of living, as well as looking for ways and guidance on how to reduce bills. For example, one in five (21%) Britons are searching for advice on saving energy at home, and for four in five (80%) saving energy is most commonly about saving money. Communication about net zero policies and their co-benefits – particularly on the potential for future savings on essentials like food and energy – can support and inform people to help bring them along the path of sustainable behaviour change.

Higher levels of support among those feeling less of an impact from the cost of living crisis also indicate that we need to consider who in the UK is vulnerable to being left behind on this journey. Policy support is lower among people from less affluent households, yet they are often the people most affected by the impacts of climate change and the cost of the transition to net zero. Policymakers also need to recognise their concerns around net zero policies and reassure them of the benefits, while also acting to minimise the cost of such policies to them.

Technical note

Survey data has been collected by Ipsos’s UK KnowledgePanel, an online random probability panel which provides gold standard insights into the UK population, by providing bigger sample sizes via the most rigorous research methods. Ipsos interviewed a representative sample of 16,160 adults aged 16+ in the UK between 27th October and 2nd November 2022.

Data are weighted by age, gender, region, Index of Multiple Deprivation quintile, education, ethnicity and number of adults in the household in order to reflect the profile of the population of the UK. All polls are subject to a wide range of potential sources of error.

Where percentages do not sum to 100 this may be due to computer rounding, the exclusion of “don’t know” categories, or multiple answers.

Questions are asked of the total sample of n=16,160 unless otherwise stated.